All of a sudden, the short-volatility trade is back on Wall Street as billions of dollars pour into options-selling ETFs like never before.

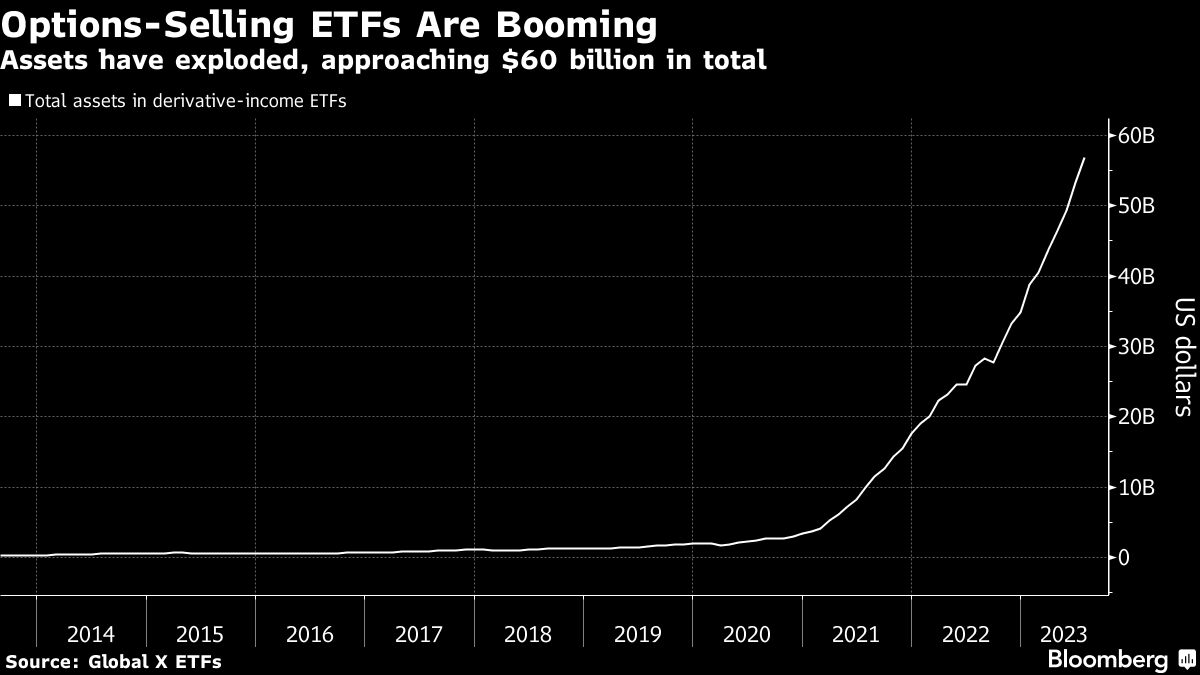

With this year’s stock rally defying recession warnings and aggressive Federal Reserve tightening, investors have been paying up for defensive strategies that offer income along the way. That’s endowed an exotic corner of the exchange-traded fund universe with a record $57 billion of assets.

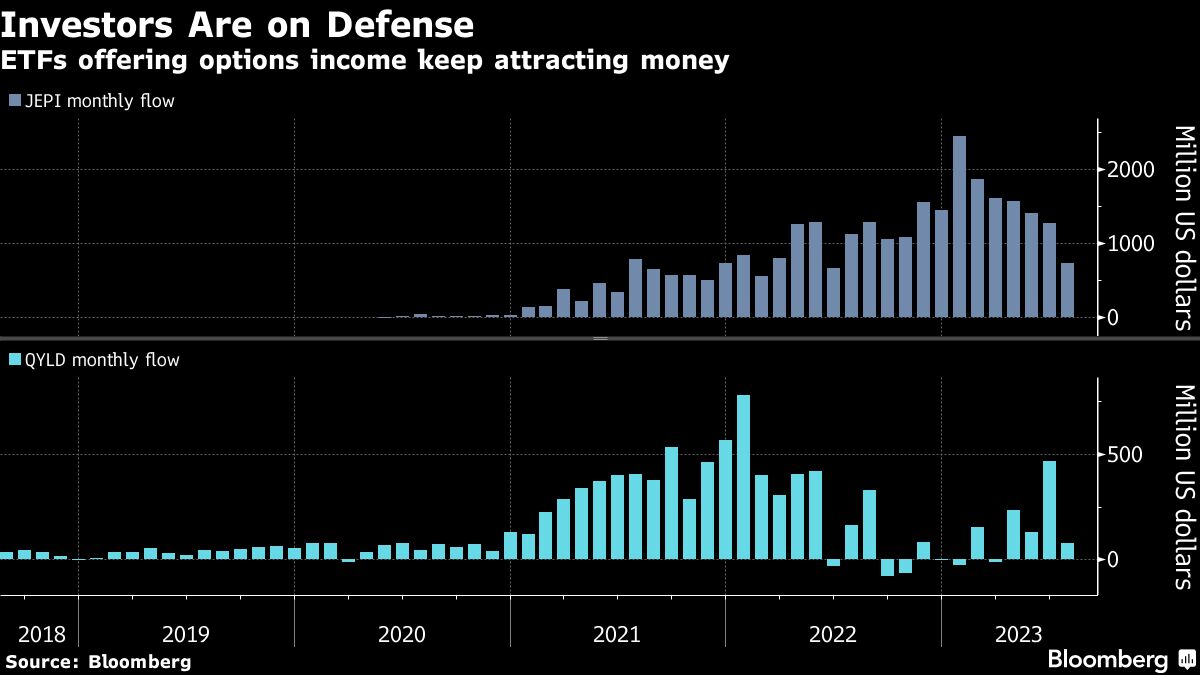

Among the most popular: Investing styles that go long equities while selling derivatives — wagers that will outperform if the S&P 500 Index trades sideways or simply fall. In so doing, investors are essentially betting against swings in share prices, with demand so hot that funds like JPMorgan Equity Premium Income ETF (ticker JEPI) and Global X Nasdaq 100 Covered Call ETF (QYLD) keep drawing in money despite subpar returns.

That crowded derivatives activity is one reason why the Cboe Volatility Index has stayed curiously low this year. Yet to equity veterans, this flurry of options selling raises flashbacks of past market incidents when wrong-footed wagers on equity calm fueled a rout, by forcing Wall Street dealers to suddenly shift their positions.

Morgan Stanley estimates that the wave of options selling, by one measure at least, broke records in April and again in June. There’s no obvious “Volmageddon” redux risk in sight, and proponents argue these funds help provide liquidity. Still to some institutional pros, the current boom spotlights the hidden dangers of the volatility ecosystem for the broader marketplace.

“If you are short volatility and it spikes rapidly, your unwinds could contribute to a short squeeze of sorts,” said David Reidy, founder of First Growth Capital LLC, a wealth management firm. “We saw this happen and its impacts on market structure in February 2018. The short-vol covering happened in March 2020 as well.”

With mundane monikers like buy write, covered calls and put write, ETFs employing the options-selling strategy have seen their assets jump more than 60% this year, according to data compiled by Global X ETFs. Buy-write funds that purchase stocks and simultaneously sell call options on these shares have seen at least 12 new launches in the past year, data compiled by Bloomberg shows.

It’s one breed of the short-volatility trade that has historically provided investors with gains but can fall prey to big drawdowns. While the VIX has climbed of late, it’s still trading below its long-term average, heading for the calmest year since 2019.

Even in today’s market where yields from three-month Treasury bills exceed 5%, the benefit from such vol selling is meaningful. QYLD, for instance, in June earned an option premium equal to 2.4% of its assets, or an annual rate well past 20%.

The income stream helped offset share losses during 2022’s bear market when long bonds or outright bearish puts failed to work as insurance against equity declines. JEPI beat the S&P 500 by almost 15 percentage points and QYLD was ahead of the Nasdaq 100 by 13 percentage points.

Their performance is less stellar this year, in part due to the relentless equity rally. And yet investor interest has shown no sign of abating. JEPI has attracted $11 billion of fresh money since January while QYLD’s inflows top $1 billion despite below-market returns.

Buoyant demand reflects investor conviction that stocks will be stuck in a range of economic uncertainty, an environment that bodes well for options selling for income, according to Rohan Reddy, head of research at Global X. In his view, any risk from these ETFs is modest, given the sheer size of the US stock market. Still, he doesn’t rule out the prospect of negative spillovers if the boom endures.

“I don’t think buy-write strategies — the growth and popularity of it — is something that we should be really concerned about today affecting market volatility in any material way,” he said. “Of course, if these strategies grow significantly and they can outrun some of the numbers that I was imagining, then maybe we might have more of an effect there.”

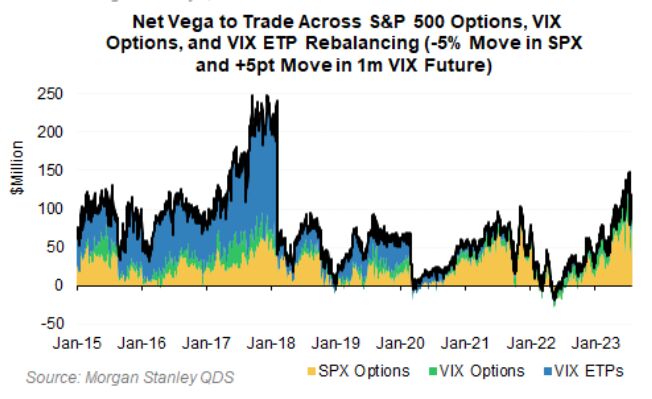

Herein lies the hidden risk: The vol selling has left options dealers — who are on the other side of the transactions — in a “long gamma” position where they need to go against the prevailing trend. That means they buy when stocks go down, and sell when they go up, in order to maintain a market-neutral stance.

The problem, per Morgan Stanley’s trading desk led by Christopher Metli, is that an equity selloff could shock options dealers out of these positions entirely — forcing them to add fuel to the turmoil given their elevated sensitivity right now to implied volatility.

When expected price swings widen, the corresponding changes in options premium increase. That typically drives dealers to hedge their exposure, known as “vega,” through index futures or stocks. Due to the complex interconnections between derivatives and the underlying equity market, all that activity can amplify volatility. By Morgan Stanley’s estimate, that vega exposure recently stood near the highest level since the 2018 Volmageddon.

“Vol-selling strategies have grown in terms of assets and in terms of breadth, with much of that new growth coming from options-selling ETFs,” the Morgan Stanley team wrote in a note this month. “If there is a shock, it’s likely the broad index exposures that come off quickest, leading to a correlated move lower.”

To Joseph Ferrara, an investment strategist at Gateway Investment Advisers, which started its first buy-write fund in the 1970s, today’s volatility landscape is different from 2018’s Volmageddon episode. Back then, a spate of exchange-traded notes designed to move inversely to the VIX collapsed when the volatility gauge spiked.

Rather than taking a direct wager that equity tranquility will prevail, the most-popular ETFs today are typically intended to cushion losses when markets tank and come with limited leverage.

“Firms that blew up or had a really tough time dealing with the volatility were firms that were leveraged,” Ferrara said. “We all live through Bear Stearns and Lehman Brothers and the rest of it. But I think there are quite a few more safety nets in place right now.”

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Lu Wang