Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Readers of this publication know the costs of an investment product reduce the net return and consider cost as an important criterion for selecting investments to make up client portfolios. But how do advisors define costs, and how important is cost reduction compared to other portfolio objectives?

In practice, few advisors truly understand the full scope of costs their clients pay and just how much they and their clients are losing to unnecessary expenses, often 100 basis points or more each year. The least expensive funds dependably outperform their costlier peers, generating more wealth for investors – and assets under management for their advisors. While these observations alone could be a sufficient reason for an advisor to focus on understanding and minimizing costs, demonstrating cost control is also a powerful tool for prospect conversations and justifying one’s own fees. As Michael Kitces put it: “Advisors are defending their own fees by squeezing out the costs of the investment products they use for client portfolios!”

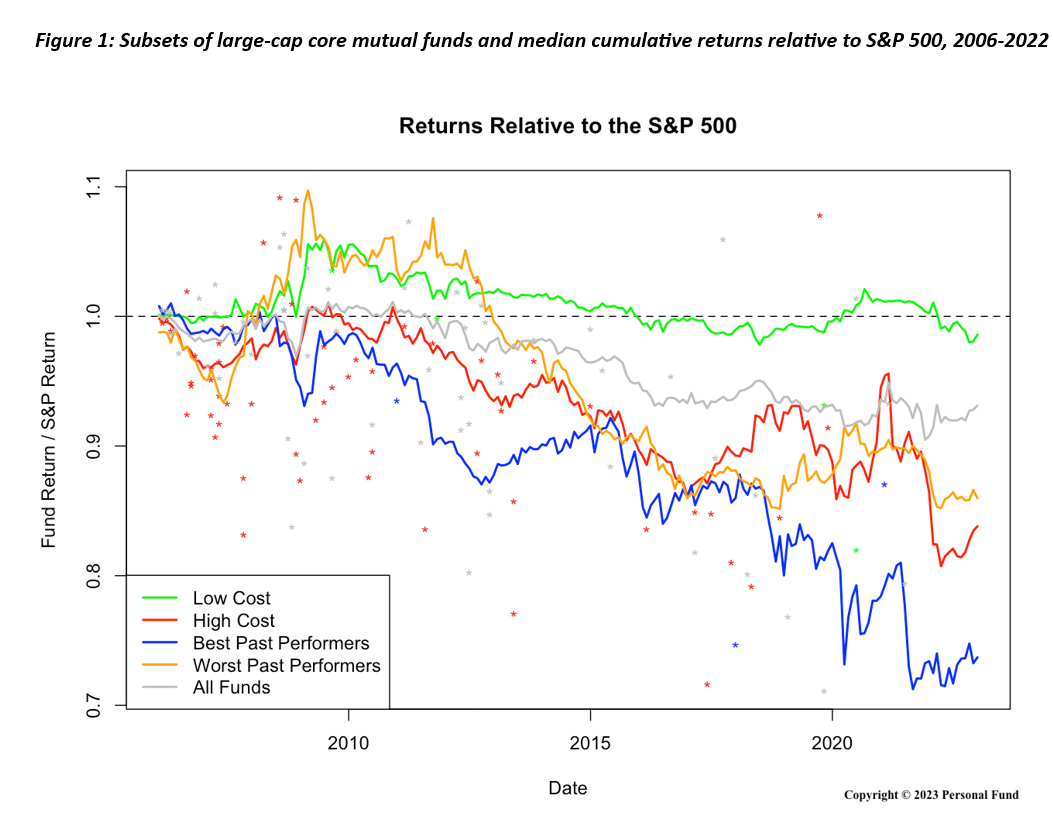

My firm’s most-recent analysis of 46,000 funds again confirmed a simple truth in portfolio construction: Controlling costs works better for managing a client’s portfolio than trying to predict performance. In fact, costs and fees are the most effective tool for predicting future performance. When comparing funds of the same asset class and investment style, past performance is uncorrelated with future performance. But current costs do predict future performance. With most products, such as cars, there is usually a direct relationship between cost and value. A $122,000 Mercedes E-class wagon is a better car by most criteria than a $17,000 Nissan Versa. But a 122-basis-point fund is not reliably better than one that charges 17 basis points. In fact, the opposite is true. With funds, to paraphrase John Bogle, you don’t get what you pay for; you get what you don’t pay for. Investment management costs are a zero-sum tradeoff.

As many researchers in academia and industry have found over the years, cost is the single most reliable predictor of future performance. Morningstar reported that expense ratio is a better performance predictor than its own star ratings.

But few investors have a full command of all the costs of owning funds and the downsides of higher costs. In addition to loads and other explicit transaction costs of buying and selling funds, there are three ongoing costs that fund investors and their advisors need to consider: explicit management fees, disclosed in the expense ratio; portfolio trading costs, which are largely opaque but can be estimated from the reported turnover ratio; and taxes on distributions in taxable accounts.

None of these costs are entirely avoidable, but all have deleterious effects on the investor’s wealth and can be controlled to some degree. All can be estimated from widely available data and should be assessed by an advisor when deciding which funds to add, retain, or sell in a client’s portfolio.

There are several empirically proven upsides to investing in less costly funds. Relative to their more expensive peers, inexpensive funds have higher average returns, lower volatility, greater chances of beating their index, lower chances of significantly underperforming their index, and a lower probability of being liquidated or merged into another fund. While superior performance has never been shown to be predictably repeatable, fund costs generally persist – a fund’s expense ratio and rank relative to other funds’ expense ratios are stable over time. The same holds true for fund turnover ratios and the resulting trading costs, and for tax efficiency relative to comparable funds.

An emphasis on cost minimization benefits an advisor beyond the obvious advantage of client asset growth. Clients care about costs. According to the E&Y 2023 Global Wealth Management Research Report, fees were a top driver of client decisions when selecting an advisor, and more than 50% of clients were concerned about hidden costs. The report concluded that “Investors are clear where they would like providers to focus: reducing costs,” and recommended that, to build client trust, advisors should “[help clients] understand the links between costs and returns.”

Many advisors are understandably cautious when approaching the subject of investment costs versus returns with clients and prospects lest they balk at the advisor’s own fees. But there is opportunity in presenting the advisor’s fee as one component in the total cost of wealth advice and management, as opposed to presenting advisory fees and fund fees as independent items. This allows the advisor to illustrate how investment-cost control is one of the valuable services that justifies the advisor’s own fee, touting cost minimization as one of their competitive advantages relative to less cost-conscious advisors. It also serves as a springboard for further discussion on differentiated value-added services and the fees that those justify. And it affords the advisor flexibility on setting those fees.

Let’s say a prospective client comes to you for a second opinion on a portfolio his current advisor constructed for him. It could be a taxable portfolio with an average value last year of $1 million, consisting of top-brand funds with strong past performance and high Morningstar ratings. In addition to asset allocation and risk analysis, you also perform a holistic cost analysis – including fees, trading costs and taxes. The total cost could easily come to 2% or more annually for a portfolio of mid-priced, actively managed funds held by a modestly affluent household in a high tax state. Many if not most clients would be shocked to learn that their funds cost them upwards of $20,000 last year. To that you add of the advisor’s fee, which happens to be 75 basis points, for a total of 2.75%, or $27,500 for the past year.

Pair that cost analysis with a model portfolio that you would recommend to the client. Using low-expense, low-turnover, tax-efficient ETFs, you could construct the same asset allocation for, say 0.7% annually, considerably less than what he paid for his current portfolio. Your report would also include your fee, say 100 basis points, for an all-in wealth management expenses of 1.7% or $17,000. In a deeper goals and values discussion, you also find the person has two children in high school who each plan to attend college, resulting in eight years of, at times overlapping, education expenses. Has the investor or their current advisor worked out a plan to navigate this cashflow crunch and reduce the cost of college?

To win this prospective client’s trust and business, you don’t have to compete by lowering your fee. In fact, through listening, analyzing, and educating, you help him see that, while you charge a higher fee, you also deliver significantly more value and total cost savings. With you, he would have come out ahead by $10,500 last year – more than 1%.

As the saying goes, fees are only relevant in the absence of value. A deep analysis of fund performance relative to cost clearly shows fund fees are relevant – they’re negatively correlated with additional value. As financial advisors deliver higher-value services to those they serve, fees naturally become less important in client relationships.

Stefan Sharkansky is the founder of Personal Fund. He holds a PhD in statistics (econometrics concentration) from the University of Washington and an MS in computer science from Stanford University. He may be reached at [email protected]

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Read more articles by Stefan Sharkansky

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.