Wall Street Reels From Painful August as Winning Trades Go Sour

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThe world’s most powerful central bankers have vowed in unison to keep interest rates higher for longer if necessary to tame inflation.

On Wall Street, that hawkish Jackson Hole message has been received loud and clear all month — fueling a $5.5 trillion stock selloff, a bond rout pushing yields to the highest in more than a decade, and more.

After rallying on bets that the Federal Reserve is on the cusp of easing policy, a slew of interest rate-sensitive investing strategies are taking a beating this August. Blame benign economic data that suggests the age of elevated borrowing costs will endure — and rich valuations across risky assets after a stunning first-half rally.

“There is a very strong likelihood risk assets have registered their highs for this year,” said Michael O’Rourke, chief market strategist at JonesTrading.

From buying meme stocks and dumping the dollar to betting against swings in stock prices, a slew of popular trades have become losers. Among the winners: Hedge funds betting that bond yields will rise anew.

Here is an overview of the trading action in charts.

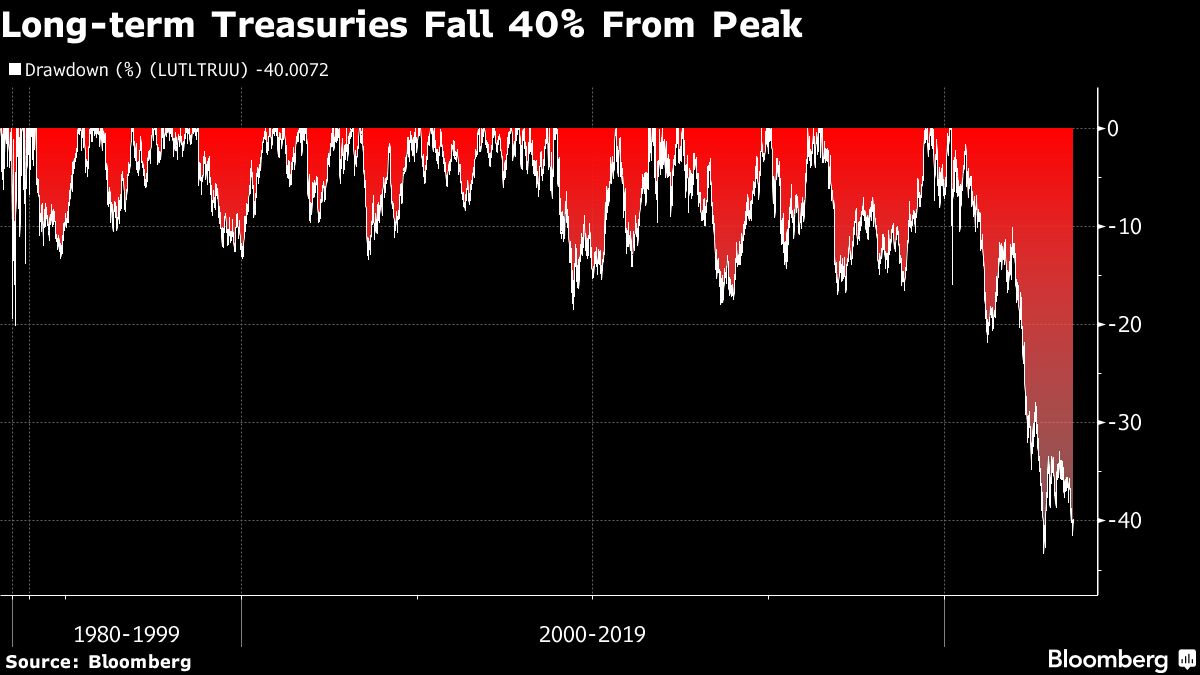

Long Bonds Are Pain Trade

The backdrop for the global market tumult is higher yields at precisely the wrong time.

According to a JPMorgan Chase & Co survey, investors recently amassed the biggest overweight bond positions in years, only to be hit with fresh losses this month. As money managers revise up their economic forecasts – the Atlantic Fed model pegs the current growth rate at an astonishing 5.9% — longer-maturity bonds have been hit particularly hard.

Those securities have lost 4% so far this month, putting them on track for a 3% plunge for the year. That’s causing fresh pain for Wall Street money managers who still reeling from a record 29% wipeout last year.

No wonder strategists at Bank of America Corp., Goldman Sachs Group Inc. and TD Securities have been abandoning their dip-buying call as market losses deepened.

“Folks that extended out the yield curve this year were thinking about the previous cycle of low inflation and slow growth coming back,” said Gregory Peters, co-chief investment officer at PGIM Fixed Income. “The muscle memory of a quick cutting Fed is still quite prevalent. That’s been swatted out and it was too premature to extend duration.”

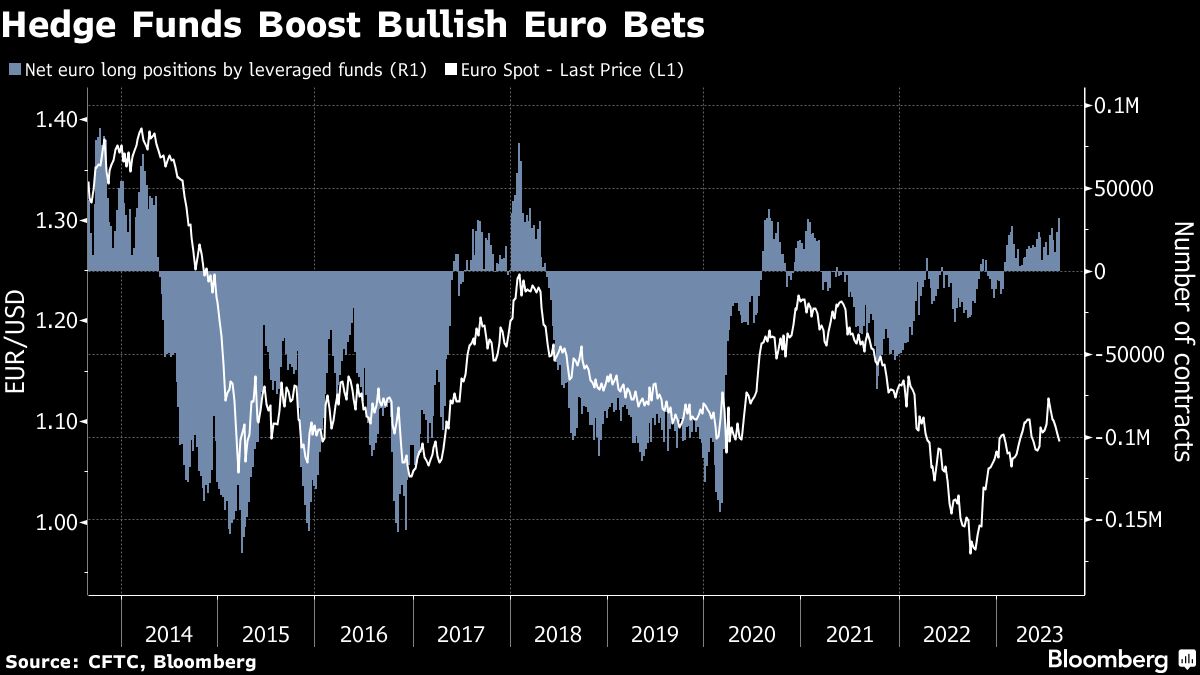

...So Are Dollar Bets

In another case of bad timing, currency bets in some of the biggest markets have gone awry.

As yields moved higher, the Bloomberg dollar index has rallied about 2% in August, bouncing back from the lowest in more than a year. That’s hurt those speculators who have assembled positions against the currency.

For example, hedge funds and other leveraged investors have recently taken the biggest bets on the euro in two years while maintaining a bullish stance on the British pound, only for the latter to weaken against the dollar to a two-month low.

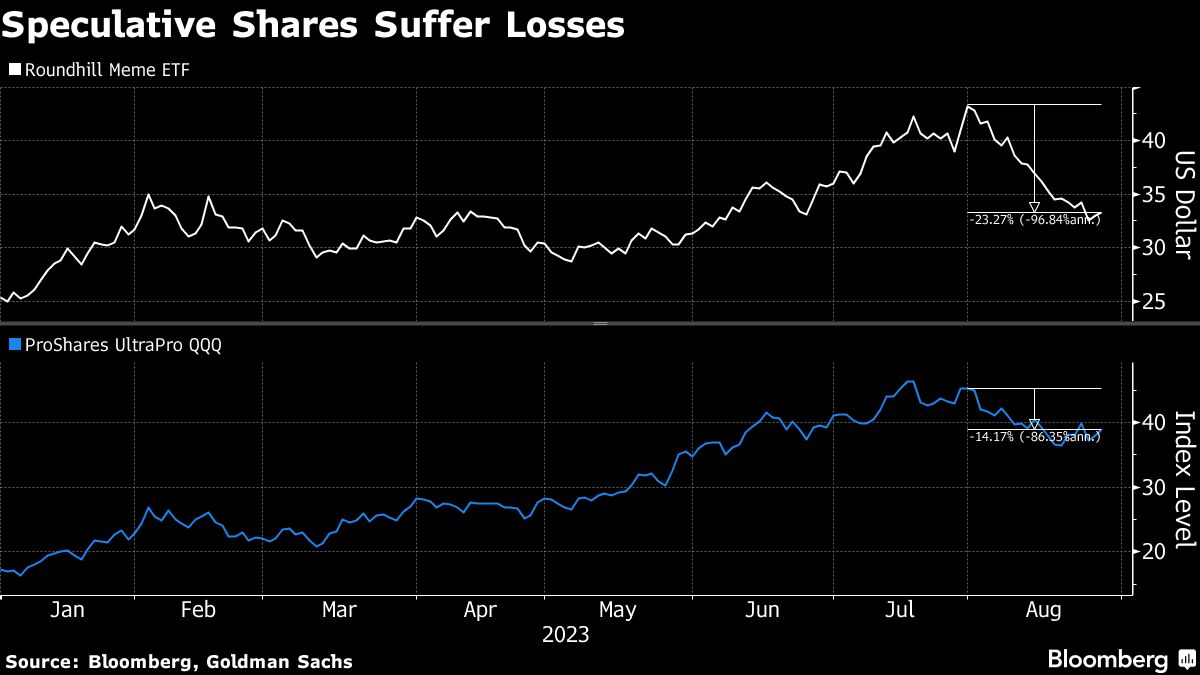

Meme Stocks Crash Back to Earth

In the world of stock investing, some of the best performers this year have quickly turned into losers as a speculative frenzy has come to an abrupt pause. The Roundhill MEME ETF (ticker MEME) advanced 70% in the first seven months of the year, only to tumble 23% in August.

More broadly, despite the AI mania in markets, betting on tech stocks is an easy trading game no longer. The Nasdaq 100 is headed for its worst month of the year, while the triple-leveraged ProShares UltraPro QQQ fund (TQQQ) has dropped 14%. The latter signals a breather after a bubbleicious rally at more than 160% that has stoked market-wide valuation concerns on Wall Street.

Bank of America Corp.’s Michael Hartnett — one of the most bearish voices out there — expects a further pullback in risky assets and trouble for technology equities “rather than era of new AI rules” in the second half. The counterpoint comes from David Kostin at Goldman Sachs, who says there’s room for investors to further increase equity exposure if the economy stays on course for a soft landing.

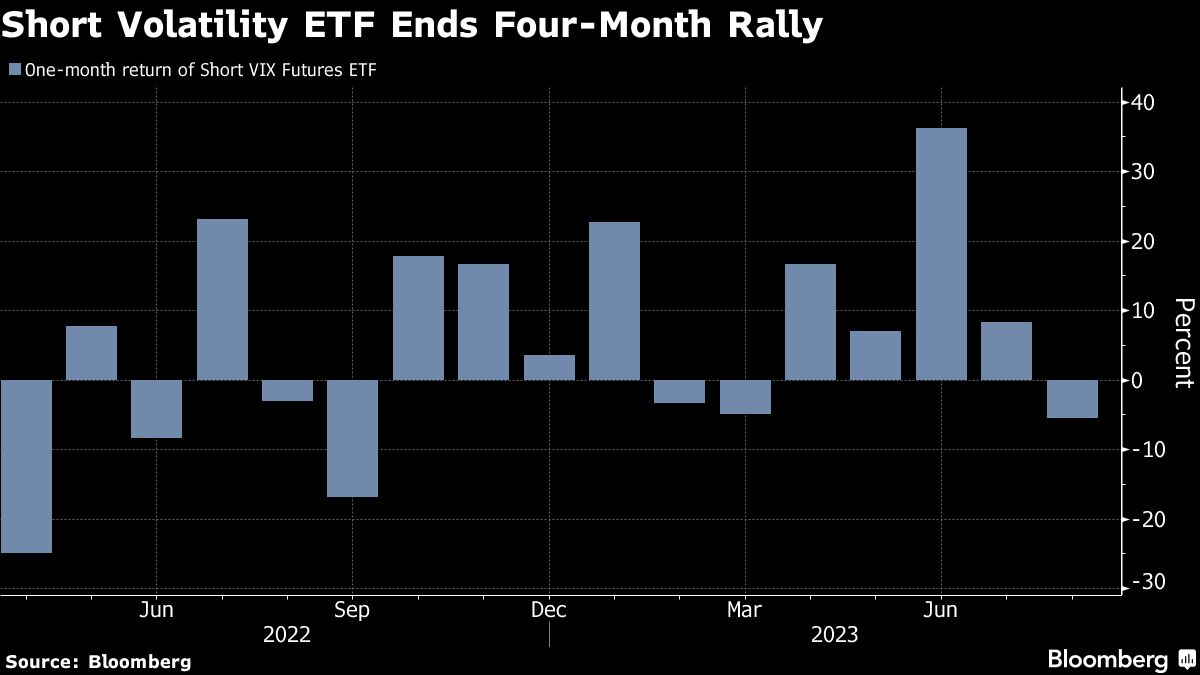

Finally, Short-Volatility Bet Backfires

Placing a bet on calm stocks markets has been a winning call for much of this year, but the peace is fraying.

Take the 1x Short VIX Futures ETF (SVIX), which thrives when stocks markets are sanguine. It has declined 5% this month as Wall Street’s favorite volatility gauge, the so-called VIX, spiked to the highest level since May at one point.

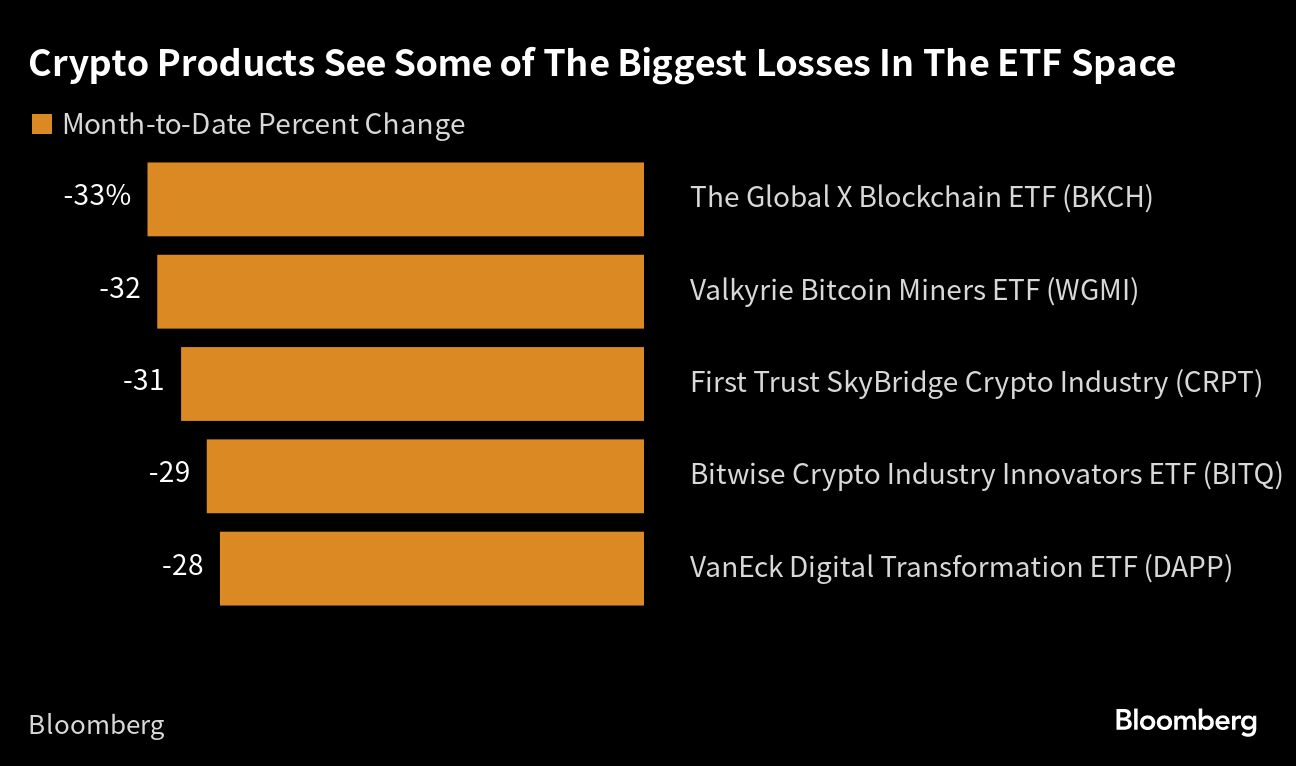

Cryptocurrencies Tumble

Digital currency traders have been gearing up for a rebound after the industry’s post-FTX crisis of confidence.

Yet with the largest token is down 11% in August, a slew of miners and digital-asset funds rank among the biggest losers in the ETF space. The Global X Blockchain ETF (BKCH) and the Valkyrie Bitcoin Miners ETF have both tumbled around 33% month-to-date.

A Few Winners...Carry Trade Is Alive

Despite the volatility, the carry trade — a strategy to buy high-yielding currencies with funds borrowed in lower-interest rate countries — has proved resilient. The Bloomberg GSAM FX Carry Index increased 0.9% in August, extending this year’s gain to 4.1%.

Hedge Funds’ Bond Shorts Pay Off

It’s also been a good stretch for bond managers who have accumulated record short positions in the futures market — which would have paid off handsomely as Treasuries sold off.

All year long as asset managers kept buying government debt, hedge funds took the other side. In the world of 10-year Treasury futures alone, bearish wagers pursued by the fast money have more than doubled since the beginning of the year.

One caveat: Their profits may be exaggerated because bearish wagers could be part of an arbitrate strategy – known as the basis trade — to exploit the minute price differences between the futures and cash bonds. That means gains on short-futures positions may have been offset by the losses in the cash market.

...And Their Equity Long-Short Strategy, Too

With richly valued speculative stocks plunging, hedge funds have netted gains by going long underpriced names while selling short their expensive peers, in a strategy known as equity long short.

For example, a Goldman Sachs index tracking the favored shares of fast-money investors outperformed a gauge of the most-shorted equities by 18 percentage points this month. That’s the most since the firm started to compile the data in 2017.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Bloomberg News provided this article. For more articles like this please visit bloomberg.com.

Read more articles by Ye Xie, Denitsa Tsekova, Michael Mackenzie

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All