US household finances have reached a milestone by accumulating $1 trillion in credit card debt, which comes with an average interest rate of 20.6%. When combined with shrinking personal savings and elevated consumer prices, many economists are worried that debt-laden consumers won’t have the buying power to keep powering the economy through the rest of the year. I find those conclusions to be overly pessimistic.

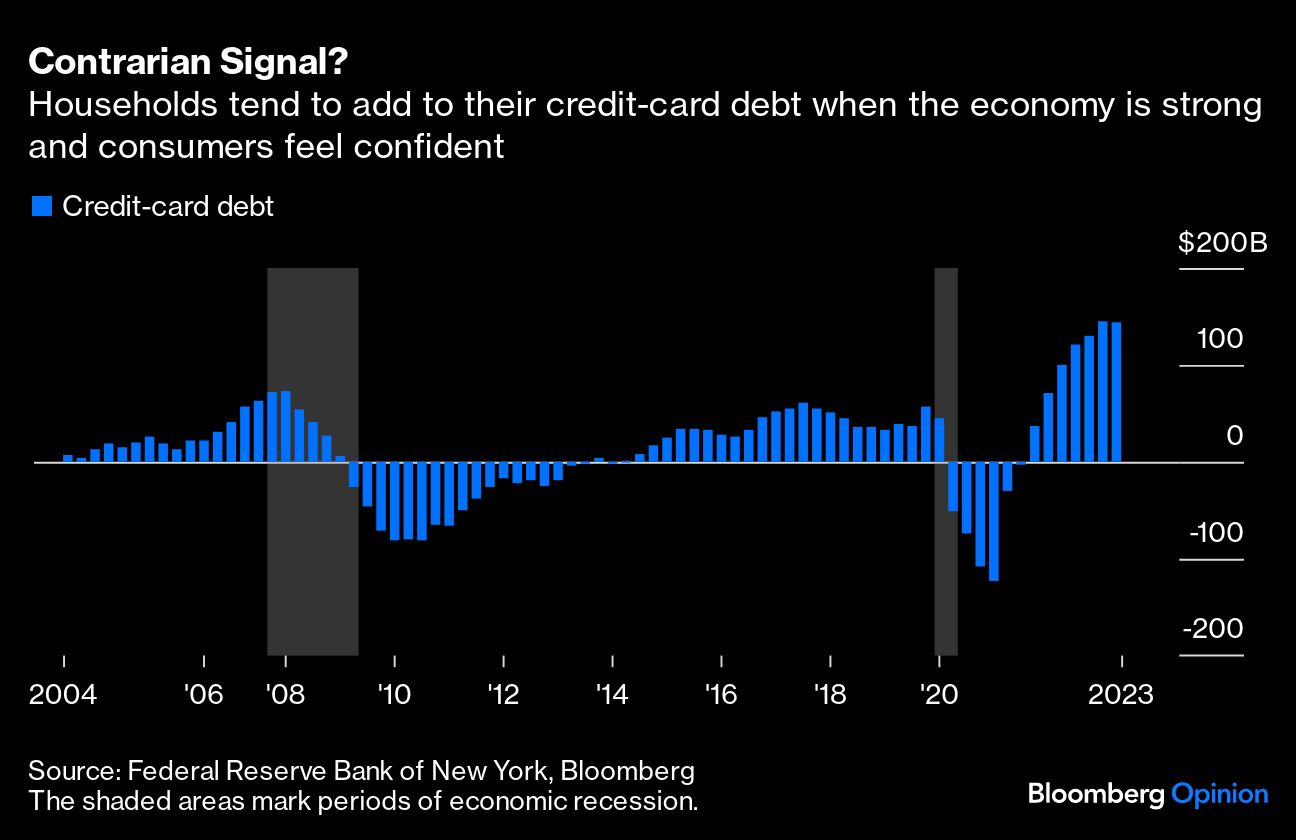

Rising credit card debt is, generally, neither a bad thing for the economy nor a sign of trouble among consumers. It seems the knee-jerk reaction to the latest data has been to assume households are stressed, turning to their credit cards for funds because they are strapped for cash or otherwise suffering under the weight of inflation. The reality, though, is that credit card debt tracks the business cycle, rising as the economy expands and shrinking as it contracts — just like business investment.

An alternative view is that households use credit cards primarily to fund larger ticket purchases of longer-lasting goods and services. Under this view, credit-card purchases are almost like a form of investment, and consumers usually only make such purchases when they are feeling confident about their personal financial situation. And let’s not forget that the unemployment rate has been at 4% or below since the start of 2022, with wages expanding at a faster rate than the pre-pandemic pace.

Indeed, this is precisely what we see in the data. Year-over-year growth in total credit card balances peaked in the first quarter of 2008, just as the economy was entering recession, and turned negative in 2009, not turning positive again until the recovery was well underway in 2014. Over the last several quarters, credit card debt accumulation has risen, consistent with an economy that seems to be gaining steam. Economists have steadily increased their forecasts on how much gross domestic product will grow in 2023, increasing them from a median of 0.3% at the start of the year to 2% currently, according to data compiled by Bloomberg.

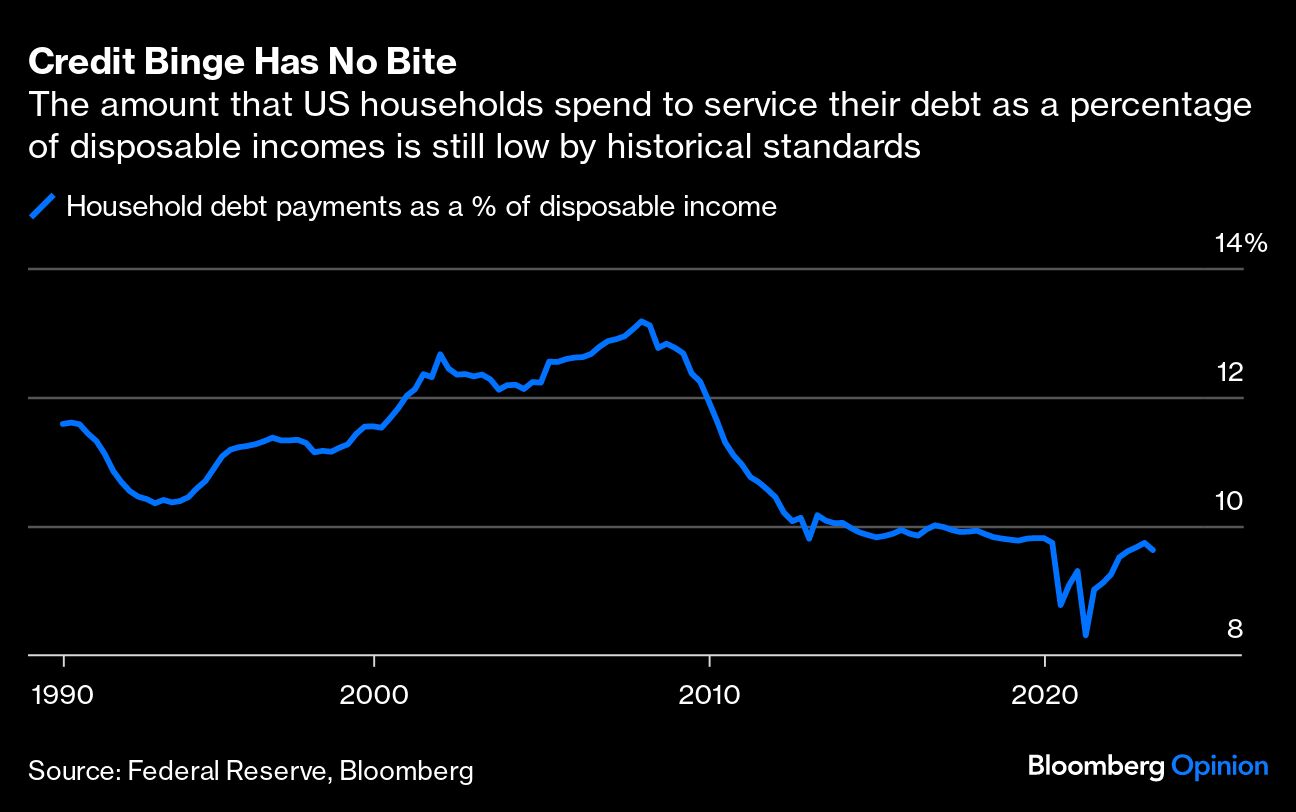

The question is really whether, given the latest surge in debt and the high rates of interest that come with that, are consumers close to feeling tapped out. The answer is that they are likely far from that point. Thanks in large part to rising wages, US households spent just 9.6% of their disposable income on debt payments, well below the peak of 13.2% in 2007, according to the Federal Reserve. As for savings, the picture there is more nuanced. At 4.6%, the personal saving rate is low by historical standards, but that’s largely a response to the unprecedented cash buffer US households built up during COVID-19.

Numerous research has been published attempting to quantify how much of the trillions of dollars in fiscal stimulus during the pandemic is still in the pockets of consumers. Most of these efforts start with old assumptions about what level of savings households ought to have. The core problem with such a starting point is that the long-term trend in saving steadily fell from 2009 through 2019, then soared to a record 14.7% in 2020 as the economy was locked down and consumers had few ways to spend their money. All this makes it difficult to estimate the underlying trend. Even a paper from the IMF suggests that all the shifts are illusory and that the saving rate is still on a downward trend.

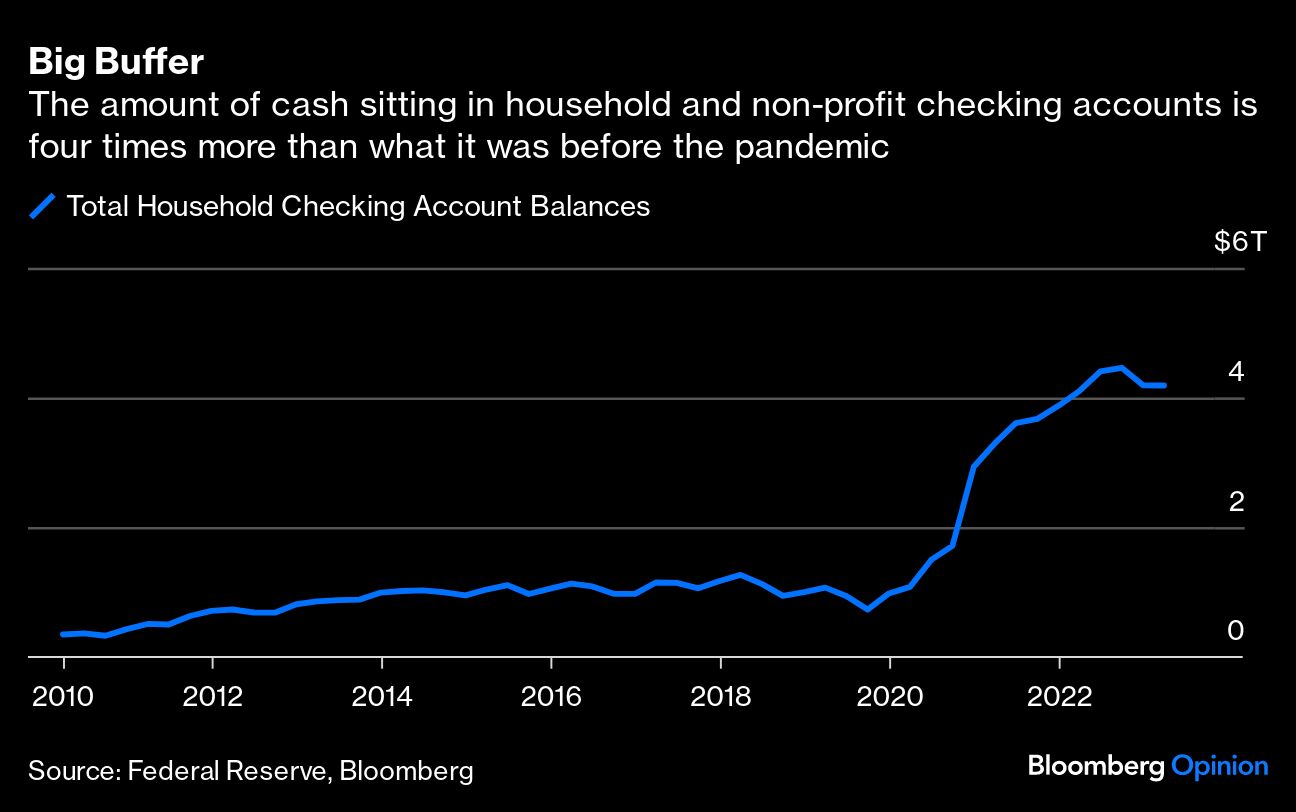

Perhaps a more concrete measure is to look at checking accounts. Prior to the pandemic, money in checking accounts for households and non-profit organizations totaled just below $1 trillion. That figure shot up to a record $4.77 trillion in the third quarter of 2022 before easing back a bit to $4.51 trillion at the end of March, according to the Fed.

So why is most all research on the subject warning that excess savings accumulated during the pandemic almost all gone? It’s because the research mostly relies on the assumption that households should have accumulated far more illiquid investments over the past three years than they actually did. So, because they didn’t, the research concludes that all the excess savings have largely been spent. That may be true, but the absence of asset accumulation doesn’t constrain consumers anywhere near a shortage of cash, which they still have in abundance.

When all these factors are considered together, it becomes apparent that the $1 trillion of credit card debt is not a sign that consumers are running out of cash or otherwise having a hard time making ends meet. Rather, it’s a sign that many households are benefitting from low mortgage rates taken out before the Fed began tightening monetary policy, sizable cash buffers and a strong job market. It may be a cliché, but it’s true that you should never bet against the American consumer.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our full schedule of upcoming CE-approved virtual events.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Karl Smith