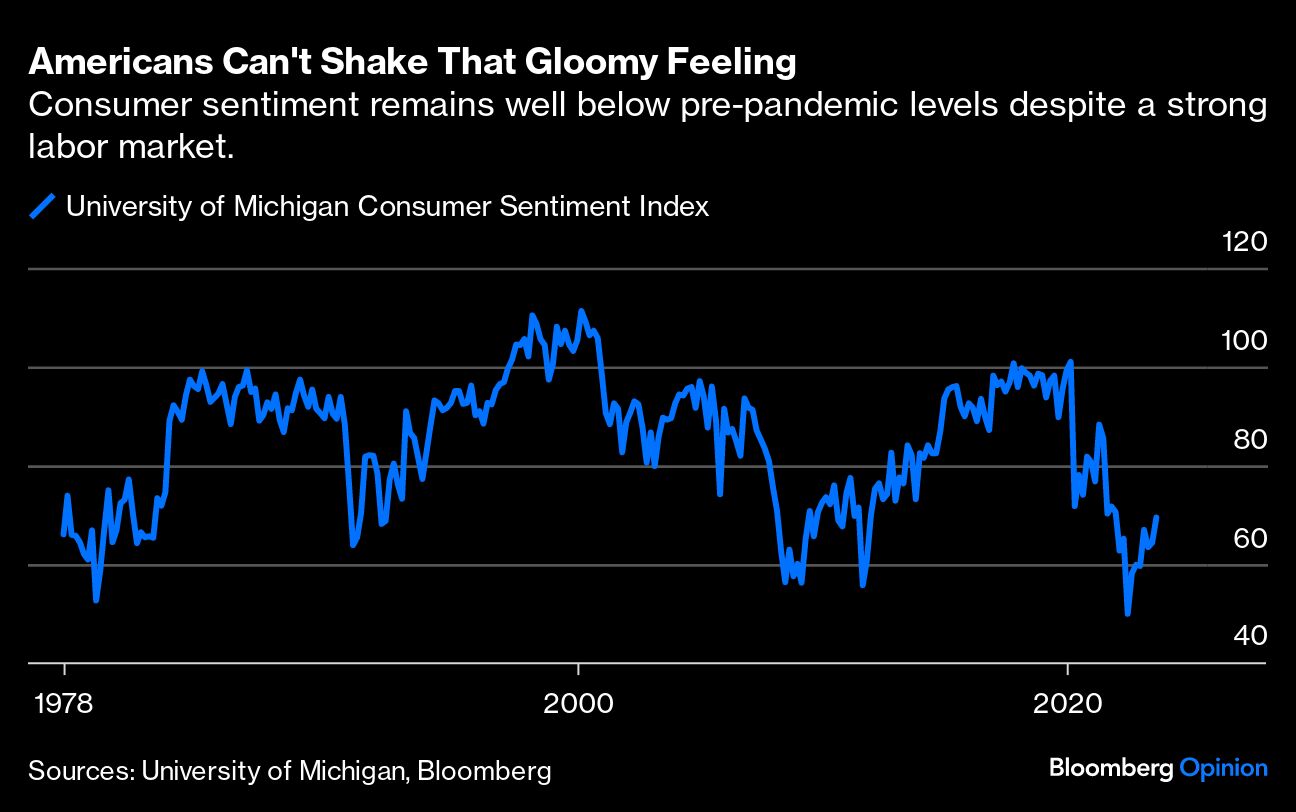

Americans are downbeat about the economy, even as inflation rates rapidly decline back toward more normal levels, the unemployment rate has held below 4% for the longest stretch since the late 1960s and economists race to raise their growth forecasts. And yet, sentiment has been at levels typically seen in recessions since the start of the pandemic.1

Lots of reasons have been given for the gloominess, including political partisanship, the media’s focus on negative news stories and bad “vibes” in general. There’s another, less talked about but more likely explanation for the disconnect: Covid-19 itself. The timing is clear, sentiment plunged at the start of the pandemic but failed to rebound when the economy re-opened and snapped back. In terms of sentiment, the pandemic caused a sudden increase in pessimism that hasn’t gone away.

In the debate over whether the US will fall into a recession, the conundrum around low levels of consumer sentiment is a big problem. Historically, sentiment was often helpful in predicting an economic contraction, but it seems to be out of commission as a useful signal at the moment.

Economists David Blanchflower and Alex Bryson showed that consumer sentiment predicted all US recessions since the 1980s up to 18 months beforehand. Based on their analysis, the US would have been in a recession in the fall of 2021, but that didn’t happen. Sure, it is possible that the predictive nature of sentiment will prove correct but with a longer-than-usual lag – we just won’t know until it happens (or doesn’t).

The thing to know about consumer sentiment or confidence surveys is that they ask people about the current state of things like their personal finances and business conditions and what they expect to happen going forward. Richard Curtin, the former director of the Surveys of Consumers at the University of Michigan, explained in his book, Consumer Expectations, how people likely form their answers. He argues that “economic expectations are an inherently social phenomenon,” so they reflect collective experiences, even non-economic ones at times. Covid-19 profoundly affected our individual lives and society overall, so it’s natural to see it clearly reflected in sentiment.

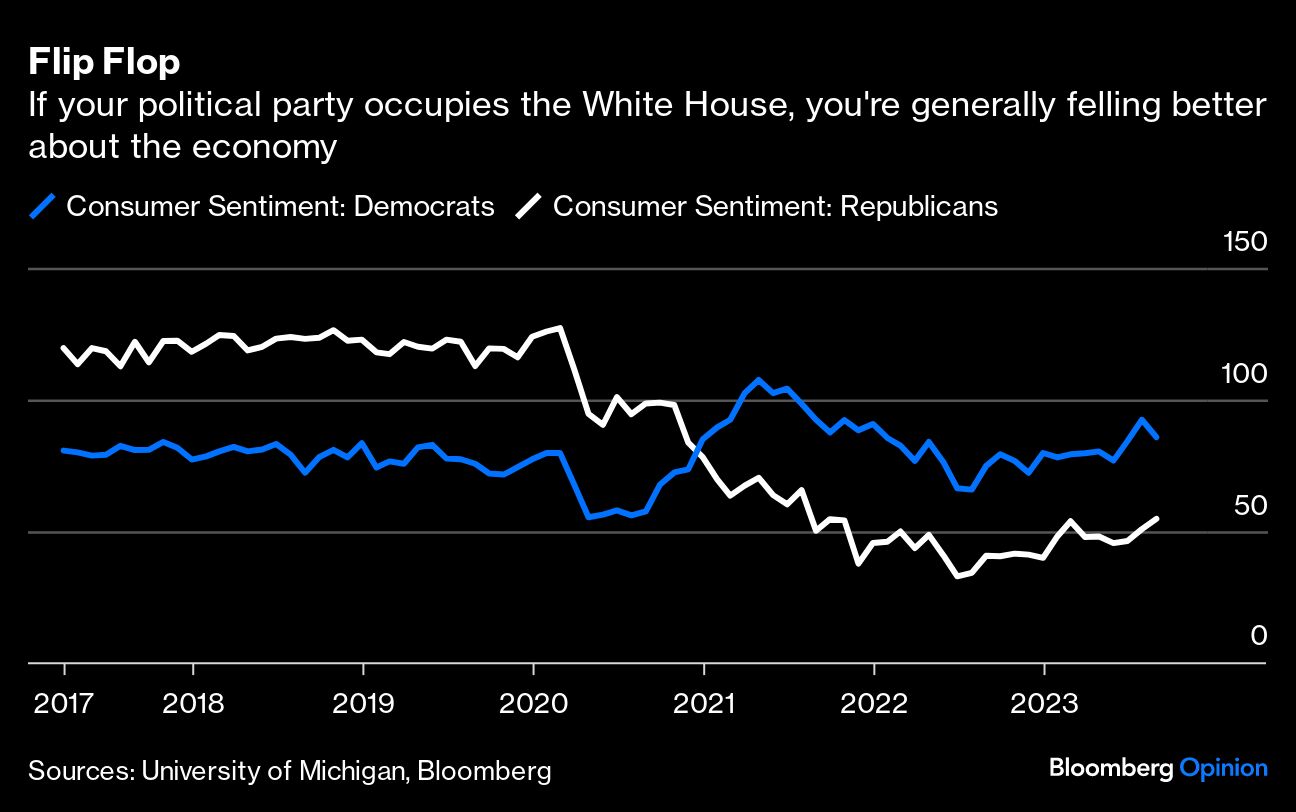

What about the current political situation, with the divide seeming wider than ever and its impact on sentiment? Yes, politics do affect economic sentiment in the surveys. All else equal, having a president from one’s party in the White House increases optimism about current and future economic conditions. And if that party loses the next election, optimism flips to pessimism. But given the magnitudes of the partisan bias on sentiment and the lack of influence on consumer spending, it must also be social or political. Whatever bias that politics is causing in sentiment, it was there well before the pandemic.

Next, the sharp rise in negative economic news at the start of the pandemic is reversing — unlike sentiment — in line with better economic conditions, according to the surveys, which also ask people what they have heard in the news about the economy recently. Unsurprisingly, people were much more likely to hear bad news than good at the start of the pandemic. Now, that split is back closer to the pre-pandemic levels. Even news about inflation is rapidly becoming more even between good and bad, and that’s consistent with the improvements in the economy.

Vibes are harder to dismiss because the pandemic almost certainly elicited strong emotional reactions due to the human tragedy and restrictions on daily life. More importantly, sentiment — with its perceptions and expectations — always has an aspect of mood. That’s one of its virtues since economic data don’t capture it well, and moods can pick up on a recession sooner than hard data. What’s missing from the vibe hypothesis, though, is why the collective mood is so much worse now.

The pandemic is a plausible answer. The specter of persistently high rates of inflation is not. Expectations about business conditions during the next five years shifted down along with overall sentiment but longer-term inflation expectations are stable. The median drifted up some last year as gasoline rose to $5 a gallon but is now back within the range of recent decades.

It’s not the first time that expectations “broke.” Income expectations (not in the sentiment index) plunged during the Great Recession and then rose slowly early in the recovery. Here again, economic conditions improved more than income expectations. Then, a few years later, expectations jumped and caught up to the usual pattern. Keep in mind that many economic relationships have broken since the pandemic began. For example, since the 1950s, two consecutive quarters of a contraction in gross domestic product have always occurred within a recession as determined by the National Bureau of Economic Research - until last year.

It would be a mistake to dismiss sentiment when thinking about current conditions. For instance, it could resolve what some view as a puzzle in consumer spending, which has remained strong in the face of faster inflation and rising interest rates. How? Later this month the Bureau of Economic Analysis will revise official statistics such as GDP and consumer spending, and we may learn that expenditures were not as strong as the initial estimates and are closer to the dour sentiment. It’s happened before. The break in income expectations after the Great Recession helped predict a sizeable downward revision in income, which lined up better with weak spending. Sometimes, one puzzle helps resolve another.

The question is, how long will this Covid-19 pessimism last? Prominent economic disruptions in the pandemic, like global supply chains and labor shortages, are basically back to normal. But that’s the economics. Sentiment has a broader lens, and so far the extra pessimism from the pandemic persists. And with Covid-19 cases rising once again, it may not end anytime soon.

1The measure of consumer sentiment here is from the Surveys of Consumers at the University of Michigan. It is a monthly, nationally representative survey of about 600 adults. The survey began in 1946. The headline index uses five questions: change in family finances in the past year and expected during the next year; buying conditions for durables; changes in business conditions during the next year and next five years.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.