But, But, What about Buffett and Lynch?

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits This article was excerpted and modified from pages 70–76 of the second edition of The Four Pillars of Investing, with the kind permission of the publisher, McGraw-Hill Inc. You can purchase this book from the link on this page.

This article was excerpted and modified from pages 70–76 of the second edition of The Four Pillars of Investing, with the kind permission of the publisher, McGraw-Hill Inc. You can purchase this book from the link on this page.

Skeptics of the efficient market hypothesis and passive investing are quick to point out three of its most prominent exceptions: Peter Lynch, Warren Buffett, and Jim Simons, obviously skilled money managers who convincingly outperformed the market over a long period.

Let’s start with Lynch. After serving as a summer intern at Fidelity in 1965, he hired on full-time in 1969 as a stock analyst, rose to director of research in 1974, and took the reins of the Magellan Fund in 1977. At the time, it was an “incubator fund,” open to the public for a few years following its 1963 founding, during which few investors purchased it, then open only to Fidelity employees until 1981, when the public was allowed back in.

At the time, the incubator fund tactic was a common ruse in the fund world: Establish a cohort of incubators, kill off or merge the laggards into the winner, then advertise the heck out of the best one’s prior performance. This is exactly what happened to the Fidelity Salem Fund, which was merged into Magellan just before it reopened. (This tactic recalls a common stockbroker scam: Mail out three different random buy recommendations to hundreds of prospects, then contact the one eighth of the prospects ([½]3) to whom the laws of probability gave all three of the winners.)

From mid-1981 to mid-1990, Magellan returned 22.5% per year, versus 16.53% for the S&P 500; impressive, to be sure, but not, as we’ll soon see, not in the same league with either Buffett or Simons, and barely just outside the bounds of pure chance and random variation.

These returns, turbocharged with Fidelity’s vaunted marketing muscle, drove massive inflows; beginning with assets of under $100 million in 1977, Magellan grew to more than $16 billion by the time the overworked Lynch retired nine years later. Lynch’s name and face became household items; more than a generation after his retirement, his gaunt white-maned visage is still among the most recognized in finance.

Lynch was out of the country in the days leading up to the market crash of 1987. That year, he underperformed the market by almost 5%, which threw his type-A work style into overdrive and he turned in good performances in 1988 and 1989.

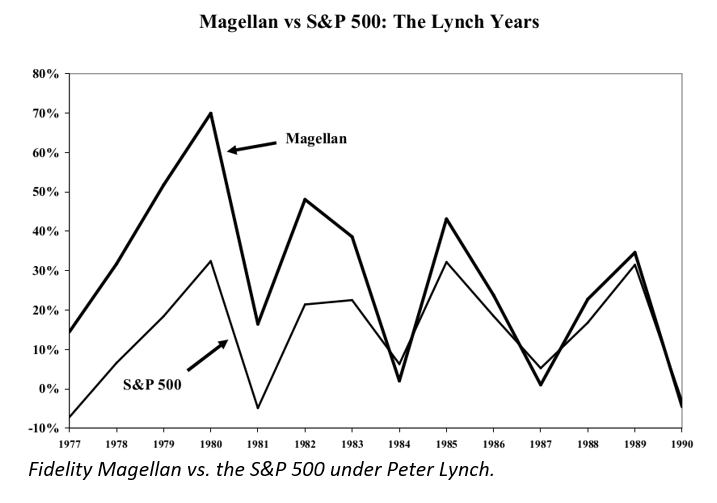

His performance soon fell victim to asset bloat. If there is such a thing as stock selection skill, then the greatest profits should be made in smaller companies that have scant analyst coverage – in Lynch’s case, names like Crown Cork & Seal, LaQuinta, and Congoleum. But the smaller the stock, the greater the impact cost for a given dollar amount of trading, and in a desperate attempt to avoid these costs, Lynch had to focus on ever larger stocks, and finally to spread his bets among a larger number of company shares; by the end of his tenure, he was buying Fannie Mae and Ford and held more than 1,700 names, effectively becoming an expensive index fund. Both of these compromises drastically lowered Lynch’s performance relative to the S&P 500 benchmark. The below plot vividly plots his decreasing margin of victory versus this index. During his last four years, he outperformed the S&P 500 by only 2% per year. Exhausted, he quit in 1990.

Warren Buffett’s track record astounds in a way that Lynch’s does not. Mesmerized at an early age by the stock market, he was blessed with a priceless exposure to Benjamin Graham at the Columbia Business School in 1950–1951. Graham, who gave Buffett the only A+ he ever awarded, initially turned down his job application at the Graham-Newman Corporation; given the anti-Semitism rampant in the investment business in that period, the firm reserved its analyst positions for Jews. Buffett returned to Omaha to work for his father’s brokerage firm; a few years later, Graham relented and hired him on. Following Graham’s retirement in 1956, Buffett returned to Omaha, where he operated a number of investment partnerships. In the early 1960s one of them began to acquire Berkshire Hathaway, a failing textile manufacturer, at an average of about ten dollars per share, into which he gradually folded his other partnership holdings. Over the more than half a century between 1965 and 2021, Berkshire returned an annualized 20.21%, versus 10.52% for the S&P 500. That sounds impressive enough, but as the recent pandemic demonstrated all too clearly, humans do not fully grasp exponential math: Compounding 20.21% annual growth over 57 years turns each share that Buffett paid a ten-spot for into just short of half a million dollars.

Warren Buffett kept his outperformance going for far longer than Peter Lynch did for three reasons. First, Berkshire’s asset bloat was purely internal, the result of successful purchases, not of capital inflow. Second, Buffett is more businessman than fund manager. The companies he acquires are not passively held in a traditional portfolio; he becomes an active part of their management. And, needless to say, most modern companies would sell their metaphorical mothers to have him in a corner office for a few hours each month. Finally, Buffett enthusiasts are fond of pointing out that the “float” of premiums collected by the insurance companies he’s fond of functions as cheap leverage for Berkshire’s holdings.

Parenthetically, it’s worth noting that although the famed economist Paul Samuelson was one of the first supporters of the EMH and wrote one of the seminal pleas for the establishment of index funds, he knew a good thing when he saw it. In 1970, just five years after Buffett acquired Berkshire, Samuelson was shown the stock’s track record by a private investor named Conrad Taff, who had, like Buffett, studied under Graham at Columbia.

The intellectually supple Samuelson recognized Buffett as the exception that proved the rule and bought some Berkshire. Still, after Vanguard’s John Bogle took up Samuelson’s challenge and established the first widely available index fund in 1976, Samuelson stopped buying individual stocks. (Before 1976, Samuelson was also smart enough to recognize that it was better to own an asset management company than to be one of its customers. Noting that “as there is only one place for a temperate man to be in a saloon, behind the bar and not in front of the bar,” he also bought the shares of a mutual fund management company his secretary had told him about.)

But even Buffett cannot defy the Gravitational Law of Asset Bloat. The above figure plots the trailing 5-year returns of Berkshire versus that of the S&P 500; just as happened to Mr. Lynch, Buffett’s spectacular initial results sowed the seeds of Berkshire’s outperformance; over the past 20 years, you’d have been slightly better off buying an index fund.

In fairness, Mr. Buffett favors value stocks, which have had some rough sledding in the past few decades. When one statistically adjusts for his value exposure, Mr. Buffett still managed to provide excess risk-adjusted returns over the past twenty years, but by nowhere near as much as his late twentieth-century margins. If and when value investing comes back into vogue, I suspect that the now 93-year-old Buffett just might be able to again open up his margin over the market some more.

The point cannot be overemphasized: Superstar managers sow the seeds of their own destruction simply because their portfolios grow too large; Buffett’s outperformance outlasted Lynch’s because, while the former has not received capital inflows for more than half a century, the latter didn’t shut off the fire hose of cash that soaked Magellan. (Fidelity finally did so in 1997, then reopened in 2008.)

A few years back, The Wall Street Journal’s Jason Zweig uncovered the story of another fund manager who benefitted from the absence of inflows, Wilmot H. Kidd III, the manager for nearly half a century of Central Securities Corporation, a closed-end fund that bested the S&P 500 by 2.8% per year before he stepped down at the end of 2021 at age 80. Closed-end funds trade as stocks and thus cannot take on new money. This protected Central Securities, in the same way as Berkshire, from inflow-caused bloat; at the end of 2021, it held only $1.3 billion in assets, a small amount for a fund that has turned in such a remarkable record.

Finally, there are managers who beat the market by even more than Lynch, Buffett, and Kidd. As you might suspect, there’s a catch: They do not want publicity, and more important, they don’t want your cash. After all, were you able to crush the market by that much, you would have no desire to invest anyone’s money but your own.

The archetype of this rare breed of superinvestors is Jim Simons. Unlike Buffett, Simons didn’t start out obsessed by investing. After being awarded a Ph.D. in mathematics from Berkeley in 1961 at age 23, he straddled the world of high-level academics and code-breaking at the NSA before founding hedge fund Renaissance Technologies in 1982.

Simons’ approach could hardly have been more different than Buffett’s. Rather than analyzing in detail individual companies, he began by painstakingly digging out massive amounts of data from primary documentary sources and virgin electronic data, much of it unrelated to finance. He then brought in the skills of world-class mathematicians and super-computer equipped data scientists to crunch these numbers in blindingly complex fashion.

His strategies fed off short-term price movements and in the process grossly violated the EMH, which says that price moves have no bearing on future ones. His performance made Buffett look like a little leaguer: In the 31 years between 1988 and 2018, the Medallion Fund, the flagship of Simon’s Renaissance Technologies, achieved a breathtaking 66% gross return – 39% after the humungous fees he was able to charge.

After just its first five years, Medallion solved the asset bloat problem by booting its clients; thereafter the fund became the exclusive preserve of Renaissance’s owners and employees. The owners of Medallion shares possess the next best thing to the Federal Reserve’s keyboards. In 2016, Renaissance fired one of its employees, David Margerman, for airing in The Wall Street Journal his objection to the politics of Robert Mercer, Simons’ right-wing partner. When Magerman sued the firm over his discharge, it settled by granting him the effortless wealth offered by access to Medallion.

The above story suggests what might be called “Simons’ Law”: The most talented investors quickly privatize their talents by shutting their portfolios to all but family and employees; if someone’s good enough to regularly trounce the market, they don’t want your money.

William J. Bernstein is a neurologist, co-founder of Efficient Frontier Advisors, an investment management firm, and has written several titles on finance and economic history. He has contributed to the peer-reviewed finance literature and has written for several national publications, including Money Magazine and The Wall Street Journal. He has produced several finance titles, and four volumes of history, The Birth of Plenty, A Splendid Exchange, Masters of the Word, and The Delusions of Crowds about, respectively, the economic growth inflection of the early 19th century, the history of world trade, the effects of access to technology on human relations and politics, and financial and religious mass manias. He was also the 2017 winner of the James R. Vertin Award from the CFA Institute.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our full schedule of upcoming CE-approved virtual events.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All