Economists are playing a game of “can-you-top-this this,” seeing who can ramp up their US economic growth forecasts the most. (Those at JPMorgan now predict a 3.5% annualized rate for the current quarter, up from the measly 0.5% they expected at the end of July). Many are saying that the recession most all of them predicted was imminent at the start of the year isn’t happening anytime soon. The White House says these are the fruits of “Bidenomics.” In reality, it’s more like a sugar high.

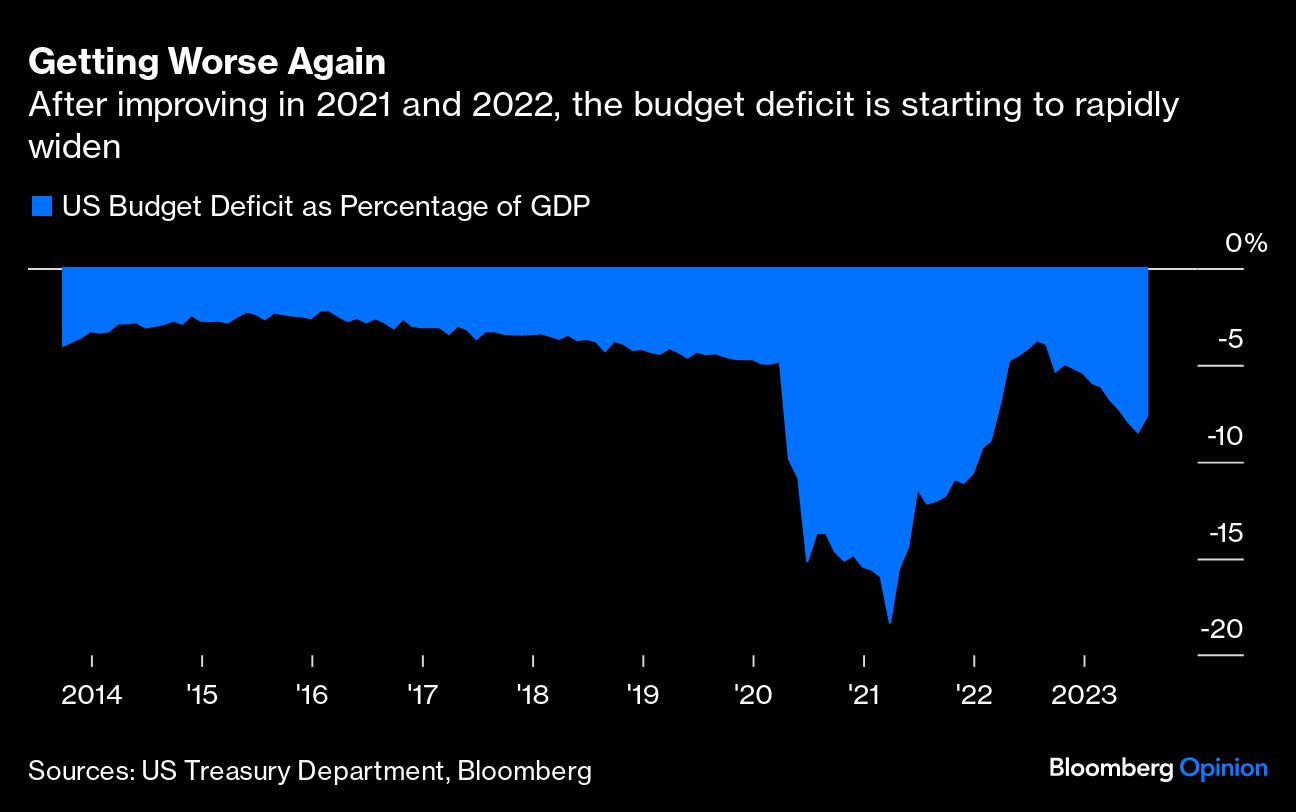

The hot economy may be getting all the attention, but the massive expansion in the federal budget deficit can’t be ignored. Back in May of 2022, the bi-partisan Congressional Budget Office projected a shortfall for fiscal 2023 ending Sept. 30 equaling 3.8% of gross domestic product. It revised that to 5.4% in February. With two weeks left in the fiscal year, the actual deficit is 7.9%.

This isn’t the way President Joe Biden’s Rescue and Recovery Plan for the economy was supposed to work. The idea was that by spending money up front to stabilize the labor market the administration would ensure a strong economy, leading to higher tax revenues and thus a lower deficit. The first two parts of the plan worked out. Unemployment has been below 4% for 19 straight months, the longest stretch since the late 1960s, and last year tax revenues as a percentage of GDP were at a record high of just more than 10%. So, how did it go wrong on the deficit? The short answer is inflation.

Prominent economists such as former Treasury Secretary Larry Summers warned that Biden’s 2021 stimulus package could “overheat” the economy and cause inflation rates to soar. The White House chose to ignore those warnings because it worried about a repeat of the slow recovery that followed the Great Recession, when unemployment stayed elevated for years.

Summers turned out to be correct. Consumer prices rose at the fastest pace in 40 years. Higher rates of inflation lead to higher government spending because benefits such as Social Security receive annual cost-of-living adjustments. In addition, tax brackets are also indexed annually to inflation. A high inflation rate in 2022 led to larger than usual bracket increases in 2023. For example, the standard deduction increased $1,800 this year while last year’s increase was only $600.

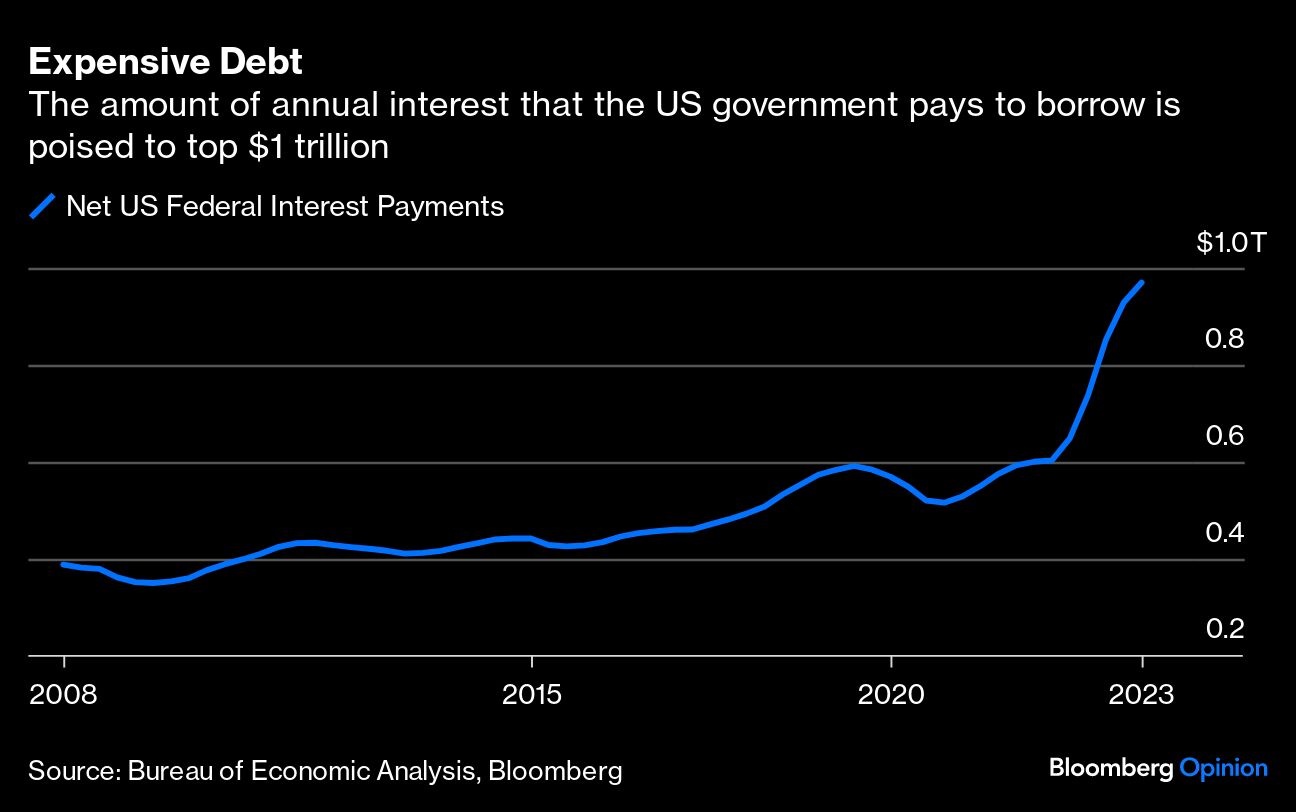

Inflation also has an impact on the deficit indirectly through interest rates. Starting in early 2022, the Federal Reserve raised benchmark rates at an unprecedented pace in an effort to get inflation back under control. Those higher borrowing costs added to the deficit in three ways. First, as rates rise it costs more to finance the federal debt, with interest payments reaching an estimated $969 billion on an annualized basis in the second quarter. That compares with $719 billion in fiscal 2022 ended Sept. 30 and $360 billion a decade ago.

Second, as the Fed began raising rates quickly, financial market assets turned lower, leading to bear markets in stocks and bonds in 2022. Although equities have rallied from the lows in 2022, they have yet to reach their 2021 peak. As a result, net capital gains from stock sales for tax purposes are lower than usual. Third, the Fed itself holds more than $8 trillion in Treasury and related bonds. In previous years, the interest the Fed earned on those holdings exceeded the interest it paid to banks that have reserve accounts with the Fed, with the difference handed back to the Treasury. As rates rose, the amount the Fed pays in interest on those reserves increased as well, leading the CBO to announce in February that it doesn’t expect the Fed to pay remittances at all in 2023, compared with the almost $100 billion it remitted the year before.

These factors overwhelmed the tendency for a strong economy to lead to narrower deficits. Biden’s economic team would argue that they would do it all over again. After all, the labor market is still strong and inflation has slowed over the last year, from a year-over-year peak of 9.06% in June of 2022 to 3.67% in August as measured by the Consumer Price Index.

Maybe so, but the US economy only has so much “fiscal space.” That’s the phrase economists use to describe the maximum amount the government can borrow before additional borrowing restrains growth and starts to increase the risk of a financial crisis. While there is no exact measure of fiscal space, Jason Furman, Chairman of the Council of Economic Advisors in the Biden administration, estimated that the US could accommodate a deficit of 3% of GDP over the long term. The CBO now projects, however, that the narrowest deficit the US can expect over the next 10 years is 5% of GDP. After that it only gets worse, expanding toward a projected 10% of GDP after 30 years.

And although the labor market is strong at the moment, history shows that could change at any moment. In fact, unemployment rates tend to trough at the start of, or right before, a recession. And although economists have pushed back their forecasts for an economic downturn, nobody is saying a recession will be avoided forever. Something will trigger a recession but we don’t know what will be the trigger. Perhaps it will be rising concern about America’s bloated debt and deficits and the resulting limited capacity to borrow without risking a repeat of rapid inflation or sharply rising interest rates. This is the price of economic policy designed to fight the last war and an unwillingness to heed warnings that the game has changed.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.