If you take your signals from the corporate bond market, the world looks much less scary than it did a few months ago. These days, high-yield US bonds yield just 378 basis points over Treasuries, more than 2 percentage points below the 2022 high and close to the narrowest gap since the Federal Reserve started raising interest rates last year. Some of that reflects the vagaries of investor sentiment, no doubt, but there have been some encouraging developments to suggest the trend just may be justified.

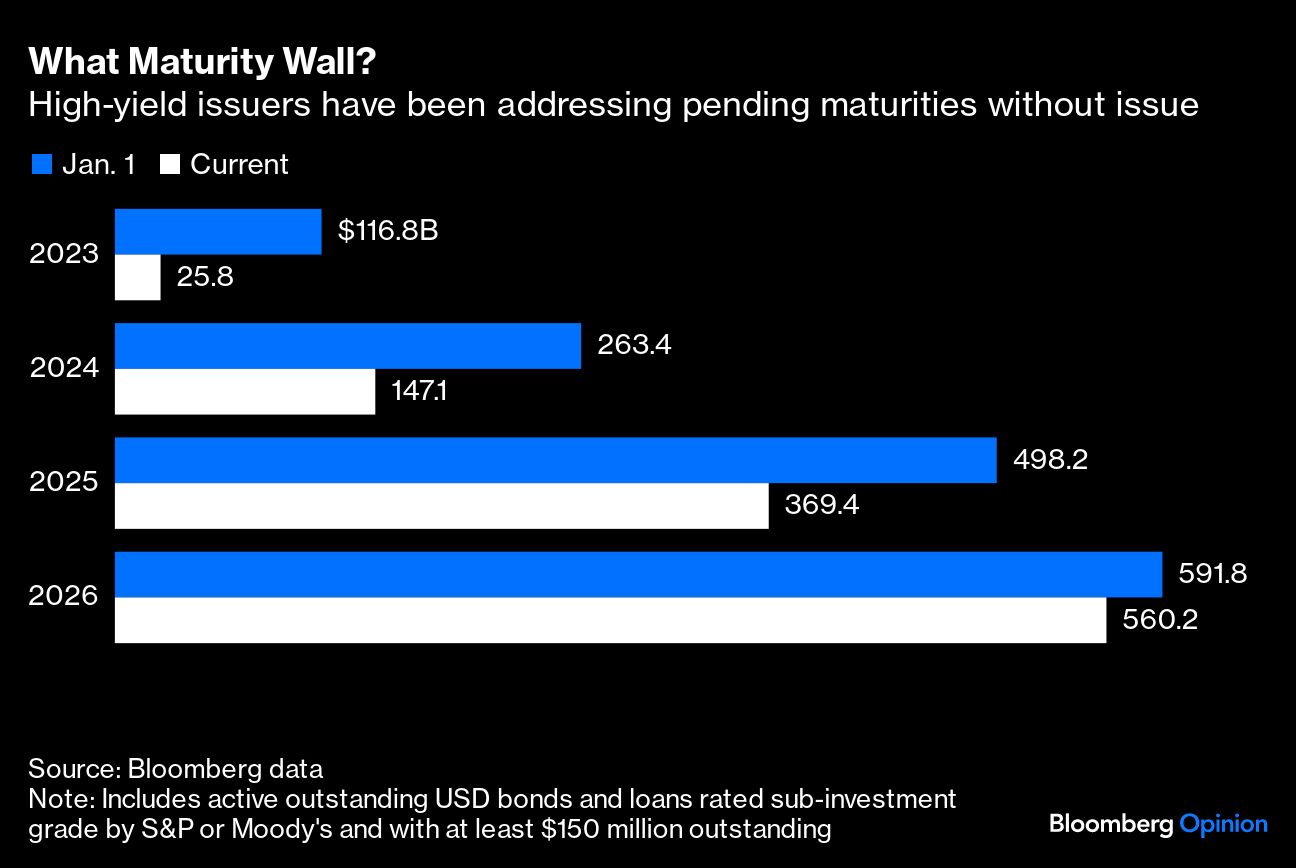

First, the hand-wringing about the Great Maturity Wall appears to have been wildly overdone. A year ago, the bear case held that interest rates were rising and the economy was deteriorating at the same time that a surfeit of high-yield debt was coming due. But ever since that point, companies have been quietly extending their debt calendars. At the start of 2023, high-yield issuers had about $878.4 billion in significant dollar-denominated bond and loan issues coming due through 2025. And since then, issuers have whittled the number down by about 38% to $542.3 billion. Most signs suggest they will continue to make plodding progress.

Noel Hebert, Bloomberg Intelligence’s chief US credit strategist — who has been doing this for longer than I have — told me that worries about “maturity walls” come around every so often but that since the early 2000s he couldn’t remember when the issue truly came down to the wire. As Hebert put it, the high-yield market has just become much bigger and more diverse than it gets credit for, so it’s hard to imagine a scenario in which companies simply can’t borrow new funds at any price. “If you are a high-yield issuer, you have corporates, loans and private — the market is nearly $4 trillion and global,” he told me Friday. “If you are a company and can trade off between three relatively active markets, you have to be in pretty rough shape to not attract any of them.”

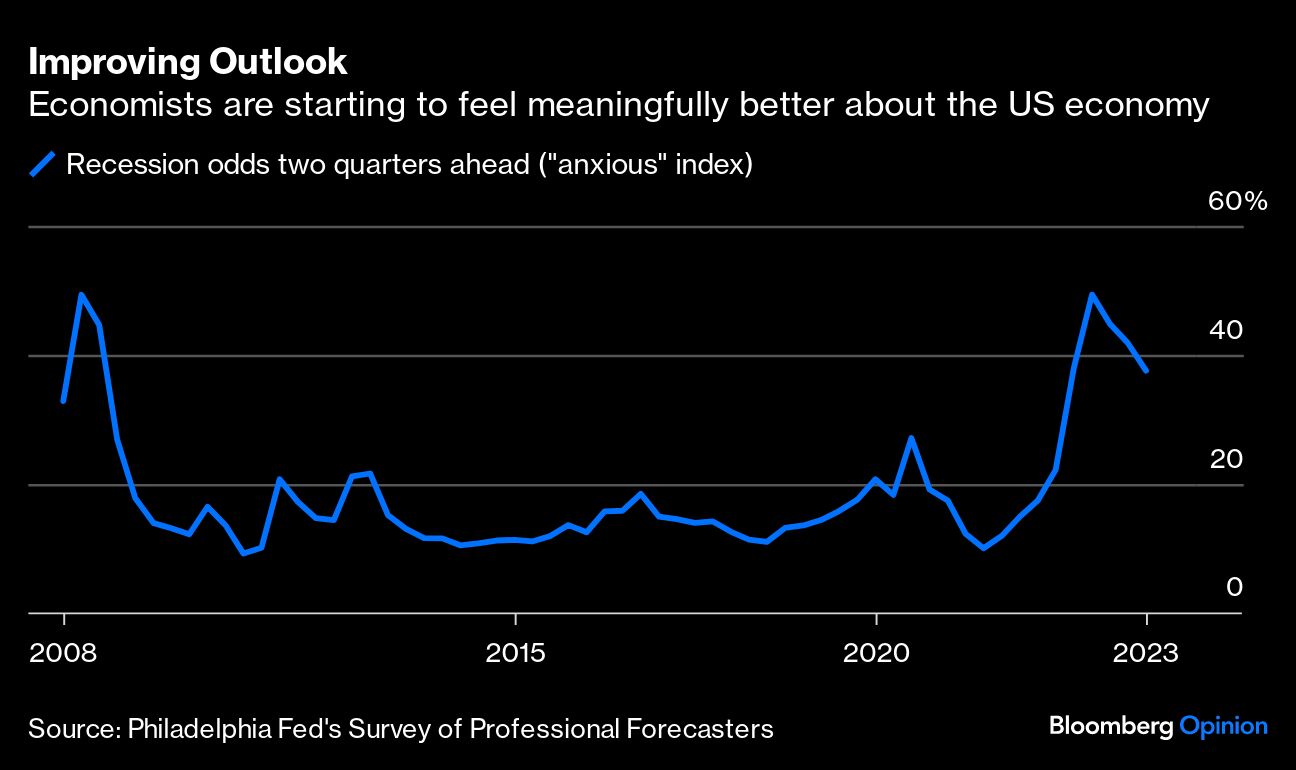

Second, the market’s consensus macroeconomic outlook has improved drastically. Despite concerns that the Fed’s inflation fight would push the economy into recession, policymakers have made meaningful progress, and the economy remains demonstrably resilient. While an unforeseen shock is still possible (as it always is), fewer and fewer economists are projecting a recession in the next two quarters in the Philadelphia Fed’s Survey of Professional Forecasters. Even if you expect trouble in 2024 or 2025, it would be unusual for credit markets to price a downturn this far in advance. Among issuers on the US corporate high-yield index, the trailing 12-month rate of defaults had been gently drifting higher, but it then seemingly plateaued around June and has slipped back to about 1.6%. Importantly, improving perceptions of the economy can have a self-fulfilling quality if they lead household and businesses to spend more.