Low interest rates can lead people to rationalize all sorts of bad ideas: investing in companies that will never make a profit, financing share buybacks with debt, spending billions on terrible streaming content, to name a few. But maybe the most irrational belief encouraged by a low-rate environment is the notion that private equity provides diversification for your investment portfolio.

It’s possible, of course, that it could, especially if your portfolio doesn’t have many publicly traded stocks to begin with. But even if that’s the case, there are cheaper and more efficient ways to get diversification.

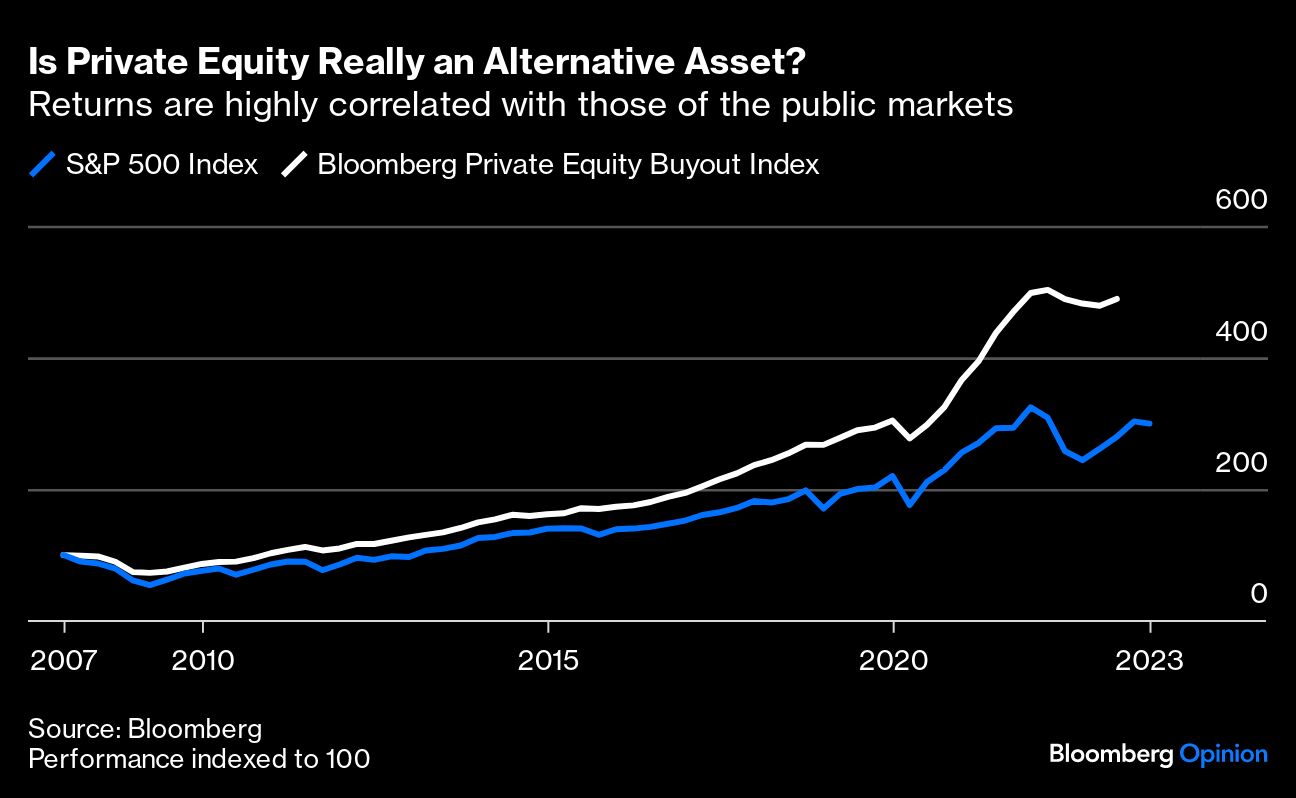

Private equity as an asset class has grown tremendously in the last decade, increasing more than four-fold to about $7.6 trillion. There are many explanations for its growth — public pensions chasing yield, for example, or fewer companies going public — and a common justification is that it provides diversification to an investor’s portfolio. And it does that, the thinking goes, because it is a so-called alternative asset.

The purpose of diversification is to reduce risk. If you invested all your money in Apple in the 1980s, for example, you’d have made a fortune compared to investing in the S&P 500. But it would have been a much riskier investment, because Apple could have failed. Diversification does not just mean lots of stocks, it can also mean lots of asset classes: commodities, bonds and, lately, alternatives such as private equity. If you get the right mix of assets, theoretically, you can strike the perfect risk/reward balance — the highest possible return for the least possible risk.

At a certain point, however, adding more assets does not alter the risk/return calculus. In fact, depending on how the asset correlates with the rest of your portfolio, a new asset may even increase risk. And that is what private equity generally does, depending on the type of fund. Often private equity simply adds leverage to a portfolio without much diversification. This can increase expected returns, but it does not reduce risk.

Private equity funds can include investments in venture capital, real estate, infrastructure and, lately, private debt. If these funds contain investments that can’t be found in public markets, they can potentially provide diversification. But often “private equity” funds are just buyout funds, which accounted for 28% of the market in 2022, measured by assets under management. These funds collect money from investors, take on debt (leverage), then buy a significant stake in a company — either taking a public one private or buying an existing private company.

In many ways this is no different, from a risk perspective, than buying shares in a publicly traded company. Measuring private equity returns and comparing them with those in the public markets is not a trivial task. Private investments are illiquid and there is no objective market return. Funds do report internal rates of return, but they are easily manipulated and not updated very frequently. Even after all that, the returns are highly correlated with those of the public markets.