Some seven weeks ago, hedge fund investor Bill Ackman laid out his rationale for shorting long-term US bonds, and I took exception.

Since then, 30-year Treasury yields are up about 34 basis points and grazed the highest level in 12 years, and Ackman has taken to X — the platform formerly known as Twitter in which he’s an investor — to double down on his earlier call. But while I’ve been humbled by the moves of recent weeks, I still think that his logic is flawed and that if he makes any more money on the trade, he may be right for the wrong reasons.

Consider Ackman’s latest musings on the theme:

I believe that long-term rates, e.g, 30-year rates, will rise further from here. As such, we remain short bonds through the ownership of swaptions.

The world is a structurally different place than it was. The peace dividend is no more. The long-term deflationary effects of outsourcing production to China are no more. Workers and unions’ bargaining power continues to rise. Strikes abound, with more likely to come as successful walkouts achieve substantial wage gains.

Energy prices are rising rapidly. Not refilling the SPR was a misguided and dangerous mistake. Our strategic assets should never be used to achieve short-term political objectives. Now we must refill the SPR while OPEC and Russia cut production.

The green energy transition is and will remain incalculably expensive. And higher gas prices will raise inflationary expectations. Just ask your average American. They see the prices at the pump and in the grocery store and don’t believe inflation is moderating.

Our national debt is $33 trillion and rising rapidly. There is no sign of fiscal discipline by either party or by the presumptive presidential nominees.

I’ve quoted less than a third of the note, but you can read the whole thing here. The upshot, as Ackman sees it, is that the long-term inflation rate won’t go back to 2% “no matter how many times” Federal Reserve Chair Jerome Powell “reiterates his target.”

That’s an interesting theory except that’s not why yields are moving higher. Breakevens and inflation swaps, which provide the purest estimates of how the market is thinking about inflation, have barely ticked up since Ackman made his call on Aug. 2. What’s driving nominal yields higher is the real yield.

After many months of defying the Fed’s forecasts, bond markets have more or less accepted that the Fed intends to keep rates restrictive for the long haul to crush inflation.

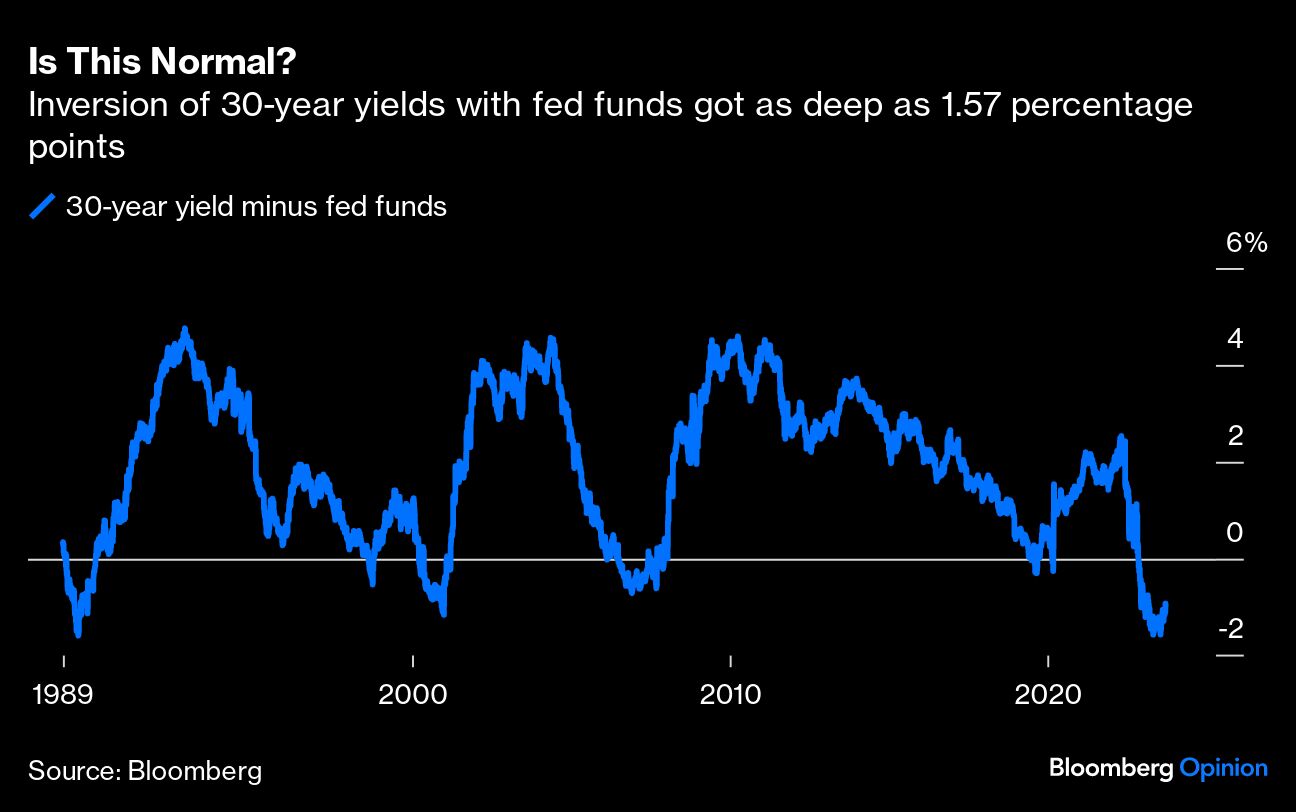

Part of that has been the market’s acknowledgment that the economy is a lot stronger than previously thought and that a recession — while clearly still possible — is not necessarily imminent. Fed funds and 30-year year bonds typically invert during periods of aggressive policy tightening, but this has been — at its deepest — the biggest inversion since 1989. Now, the world is returning to a semblance of normal.

In his latest remarks, Ackman lays out some important risks. US deficits clearly demand attention; deglobalization is picking up steam; and the world faces a complex and potentially expensive adaptation process in the face of climate change — risks that no one can ignore.

But to my eye, he’s too dismissive of the Fed’s ability and determination to deliver 2% inflation. Since former Fed Chair Paul Volcker came onto the scene, the central bank’s leadership has provided little reason to doubt its commitment to low and stable prices (save for policymakers’ overly dovish stance through 2021, which they have mostly learned from). The fact that they are still weighing additional interest-rate increases after the 525 basis-point onslaught since March 2022 should only reinforce that view. The Fed is obsessed with its 2% inflation target and has the tools to deliver on it, and Ackman would have to maintain his short position for years — maybe decades — to even see a serious internal debate about abandoning that policy framework.

In the meantime, the more salient debate concerns whether “real” rates have moved materially higher for the long run, and there I’m also cautiously optimistic. As term premiums for long bonds rise a bit from recent lows, it’s reasonable to think that they’re signaling a modest but growing uncertainty about the neutral real rate of interest — and, consequently, the level of policy rates that central banks must maintain to deliver on those inflation targets that they obviously hold so dear.

But as International Monetary Fund economists have noted, developed economies are coming off an extraordinary period of declining real interest rates since the mid-1980s before the recent inflation scare. While there may be serious risks on the horizon, a careful breakdown of the trend’s drivers suggests that real rates are driven foremost by demographics and total factor productivity, and they’re likely to head back toward where they came from once inflation is beaten. While Ackman’s concerns are understandable, the IMF economists think it would take an unlucky combination of several such risks to move the needle. Here are IMF economists Jean-Marc Natal and Philip Barrett from a note earlier this year:

Overall, our analysis suggests that recent increases in real interest rates are likely to be temporary. When inflation is brought back under control, advanced economies’ central banks are likely to ease monetary policy and bring real interest rates back towards pre-pandemic levels. How close to those levels will depend on whether alternative scenarios involving persistently higher government debt and deficits, or financial fragmentation materialize. In large emerging markets, conservative projections of future demographic and productivity trends suggest a gradual convergence towards advanced economies’ real interest rates.

All told bond yields have clearly moved up, and there’s always a risk that they’ll continue to do so. Yet they’re not primarily reacting to inflation concerns, but — foremost — to the market’s realization that the Fed means what it says. In a fuzzier sense, they may also reflect a growing concern about the future of real rates, however overblown, which may yet fuel volatility in the months to come. In other words, the Ackman bond short may continue to make him money. Even then, I still think that makes him more lucky than right.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.