S&P 500 Options Quirk Mints Billions, Stirring Manipulation Talk

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThe fate of stock options with a face value of trillions of dollars is being influenced by unusual trading activity in the S&P 500 outside regular market hours, new research has found.

A monthly pattern sees key prices jump just before the expiration of derivatives tied to the benchmark US gauge, directly affecting which contracts will pay out, according to a study posted online last week. The phenomenon is generating profits of roughly $3.8 billion per year for bullishly positioned investors, it said.

The authors of the paper — Guido Baltussen of Robeco, Julian Terstegge of Copenhagen Business School and Paul Whelan of the Chinese University of Hong Kong — struggled to find an explanation for the moves, leaving them to speculate that “manipulators” could be at work. Their hypothesis: traders may be taking advantage of a window of thin trading, pushing up the index either through futures or the pre-market to benefit their option positions.

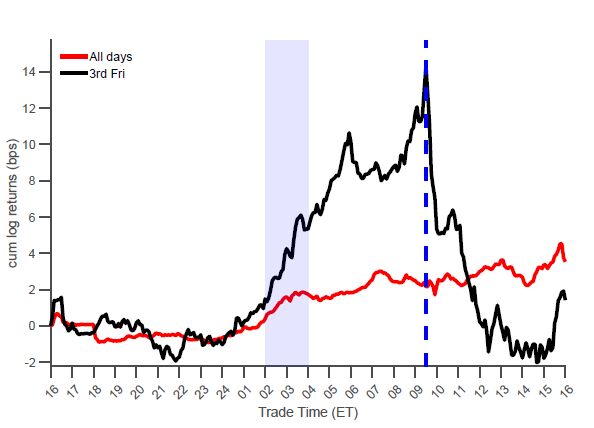

The market jumps just before options expiration on the third Friday of every month. Source: The Equity Derivative Payoff Bias.

That’s a bold claim in the biggest and most liquid stock and options market in the world, and the trio concede it’s hard to find tangible evidence to support it. It’s also debatable whether buying in one part of the market to support positions elsewhere would constitute manipulation.

They also raised a more benign alternative theory familiar to most traders: Option market makers could be driving stocks up as they hedge their positions right before the Friday morning expirations.

Either way, the pricing anomaly is sure to grab attention on Wall Street, where investors have a long-standing paranoia over how much power large institutions wield over certain corners of the market. In recent years, concerns have been raised over everything from the VIX Index being rigged or options hedging driving S&P 500 swings to the possibility economic data is being leaked.

Whelan, Baltussen and Terstegge’s paper raises important questions about a statistically significant pattern that appears to be minting cash for well-positioned investors.

“We care because it’s a market inefficiency,” Whelan said in an interview. “There could be hedge funds or professional customers out there which are profiting from this effect.”

Manipulation Window

The study is titled The Equity Derivative Payoff Bias and centers on the third Friday of every month, when payouts for option holders are decided at the market open.

Instead of using the S&P 500’s opening price or its previous close to settle the contracts, exchanges like Cboe Global Markets use what’s known as the Special Opening Quotation (SOQ). It’s calculated by S&P Dow Jones Indices based on the first traded price of every member stock in the S&P 500, and can deviate from the gauge’s official opening level because the latter uses the previous day’s close for any share that doesn’t immediately trade at the open.

The researchers found the SOQ is routinely higher than the Thursday close by an average 18.5 basis points — but only on the monthly expiration days. On all days the gap is just 2.3 basis points.

It turns out the market has a propensity to rise during the night before Friday’s settlement and then pull back just after — a pattern the authors assert could be deliberately manufactured.

“Equities trading pre-open is much less liquid than during regular trading hours, making the overnight window most suited for manipulation,” the trio wrote. “Subsequently, prices revert as manipulators offload their positions.”

This temporary premium is transferring a large amount of wealth to some options traders at the expense of others. From 2003 to 2021, those buying bullish calls pocketed $2.8 billion a year more than they would have if the settlement had been based on the Thursday close, the researchers said. Investors selling bearish puts reaped $1 billion more profits per year.

They also found based on Cboe data that pro customers tended to boost their exposures the day before option expiries so that they would benefit from the overnight price spike.

In response to an inquiry from Bloomberg News about the findings of the paper, Cboe emphasized its focus on preserving the market’s integrity and protecting investors’ interest.

“Cboe takes any market abuse, including manipulation, seriously and maintains a regulatory program that surveils for unusual trading activity,” a spokesperson for the firm said in a statement.

CME Group, another major derivatives exchange, declined to comment. S&P Global, which calculates the SOQ, referred to the calculation methodology.

Hedging Theory

To Roni Israelov, chief investment officer of Boston-based financial services firm NDVR, the hedging theory could explain the move, since market makers would typically go to the futures market to balance their positions in a process known as delta hedging.

“There’s likely a natural mechanical reason why the market’s moving in this way, probably associated with the fact that delta is important and the dynamics for delta around the time options expire can be complicated,” he said.

In what he calls an “untested hypothesis,” market makers may opt to take part in stock trading in the opening auction to minimize the basis risk arising from the discrepancy between the price at which they liquidate their hedge and the options’ settlement prices, which are tied to the S&P 500’s SOQ.

Whether it’s nefarious or not, Whelan says the persistent pattern shows the morning settlement can be easily influenced. The same effect can’t be seen near the close, where other types of option contracts — including the booming zero-day ones — expire, because markets are much more liquid and harder to move at that time, he said.

“It’s impossible to prove if it’s manipulation or hedging,” said Whelan. “The point is that this illiquid period bangs up against a very important time when it becomes liquid, but at that instant there’s this massive payoff calculated. So it’s incredibly important economically.”

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Bloomberg News provided this article. For more articles like this please visit bloomberg.com.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All