The yield on the benchmark 10-year Treasury is up 70 basis points this year, leading many to question the future direction of interest rates. Let’s look at the underlying causes of this and whether those conditions are likely to persist.

The yield on the benchmark 10-year Treasury is up 70 basis points this year, leading many to question the future direction of interest rates. Let’s look at the underlying causes of this and whether those conditions are likely to persist.

As head of economic and financial research at Buckingham Wealth Partners, I’ve been getting lots of questions about rising U.S. interest rates, both short- and longer term, which has surprised many investors and market forecasters. For example, on July 15, 2023, with the 10-year Treasury note at about 3.8%, Bloomberg published an article titled “History Says It’s Time to Buy Long-Term Bonds as Peak Rates Near” in which it noted: “Surveys by Bank of America Corp. and JPMorgan Chase & Co. have found that investors digesting the price action have jacked up their exposure to long-dated bonds.” Among those recommending extending duration was BlackRock President Rob Kapito, who told analysts that buying longer-term bonds was a “once-in-a-generation opportunity.” Defying forecasts, as of September 26 the 10-year yield had risen to 4.56%. With this in mind, let’s examine the factors that help explain why rates have continued to rise. There have been three persistent sellers of Treasury securities, helping to explain rising rates, and I’ve added several more reasons that may have contributed:

- In addition to raising interest rates, the Fed has been engaged in quantitative tightening (QT), shrinking its balance sheet by almost $100 billion every month. That’s draining liquidity, pushing rates higher than they otherwise would be.

- Brazil, Russia, India, China and South Africa (BRICS) countries are actively engaged in reducing their holdings of U.S. dollars as a reserve currency. And other countries are joining them, including Argentina, Iran, Saudi Arabia, Turkey, Venezuela and other Gulf States countries. These countries have all taken steps to reduce their reliance on the U.S. dollar in international trade and finance. The result is that the share of U.S. dollar assets in central bank reserves dropped by 12 percentage points – from 71% when the euro was launched in 1999 to 59% by 2021. The sale of U.S. Treasuries by the central banks of these countries puts upward pressure on rates.

- Among the largest holders of Treasury securities are U.S. banks. The commercial real estate crisis has created a capital problem for banks, especially regional banks. To raise liquidity, they could be forced sellers of Treasury securities, the most liquid asset they hold.

- While the Fed has been tightening monetary policy by raising rates and engaging in QT, the federal government has been engaging in massive fiscal stimulus, running a budget deficit of about 6.3% of GDP at a time of full employment (when we should be running surpluses to slow economic demand). Among the stimulants to the economy were the passage of the CHIPS and Inflation Reduction acts of 2022. The CHIPS act provided roughly $280 billion in new funding to boost domestic research and manufacturing of semiconductors in the United States. The act included $39 billion in subsidies for chip manufacturing on U.S. soil, along with 25% investment tax credits for costs of manufacturing equipment and $13 billion for semiconductor research and workforce training. The Inflation Reduction Act included $663 billion of the law's climate action investments that are embedded in the federal tax code. These bills have provided significant economic stimulus, leading to increased spending on infrastructure at a time of full employment.

- The fiscal deficit, with U.S. debt-to-GDP now exceeding 100% and forecasted to continue rising, has led to the downgrading of our debt rating. That could lead foreign investors to demand a greater risk premium to hold Treasury securities, pushing rates higher. In addition, the deficit leads to the increasing supply of Treasury bonds that must be issued to fund it, putting upward pressure on rates.

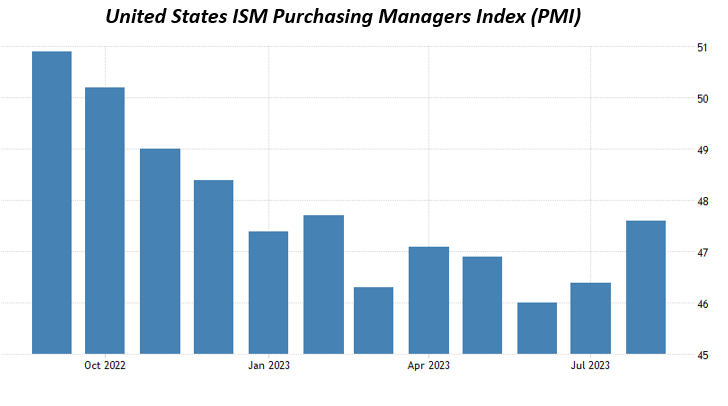

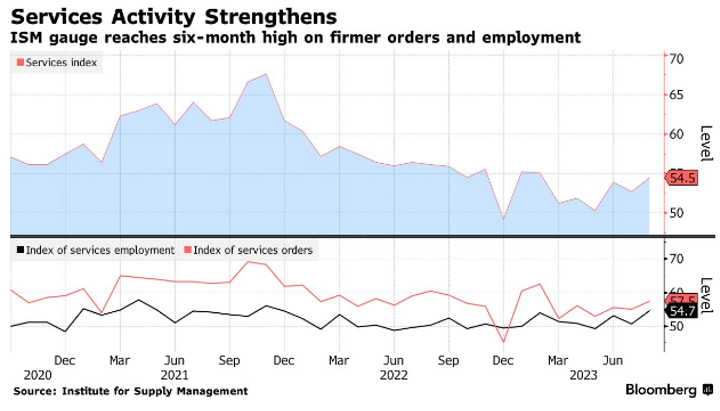

- The U.S. economy has been stronger than expected. The manufacturing sector, which accounts for only about 8% of employment, has been in recession since November 2022 as the Fed’s aggressive rate hikes cooled the interest-sensitive sectors of the economy (such as housing, autos, commercial real estate, manufacturing and durable goods). But service-sector spending, which is less sensitive to interest rates and constitutes about 78% of GDP, continues to be strong even as economic growth has slowed. As the following charts show, while the U.S. ISM PMI has been below 50 (contracting) since November 2022 (10 straight months), economic activity in the services sector expanded for the eighth straight month in August, hitting a six-month high of 54.5 (readings above 50 indicate expansion).

- Japanese yield-curve control (YCC) is ending. In July, the Bank of Japan (BOJ) began phasing out its seven-year-old YCC program, or at least took a major step toward an eventual exit. YCC suppressed Japanese bond yields, increasing demand for higher yielding assets such as U.S. Treasury bonds. The phasing out of YCC could be contributing to higher U.S. yields due to reduced demand from Japanese investors.