Helping an investor cash out of a gummed-up buyout fund used to be a niche business. Now it’s mainstream. So-called secondary funds, which offer to buy unwanted private equity holdings, have become widely accepted. It would be a shame if normalization overshadowed one of the key reasons they have flourished — to remedy seemingly ill-disciplined investment in private markets during the era of easy money.

Secondaries enable existing private equity investors — or “limited partners” — to liquidate some or all of their holding in a fund. It’s a welcome service if that fund is struggling to return cash by selling its underlying investments. Secondaries can also take direct stakes in buyouts lacking decent exit options. The private equity manager then gets to achieve a partial gain and secures extra time to complete the buyout strategy.

This isn’t a new phenomenon. Secondaries performed a similar role in the financial crisis. But fund managers have become much more willing to let their LPs use them, and activity has boomed.

Hence the secondaries market is bringing together two categories of private equity investor. On one side are seasoned LPs who want to raise cash. Their private-market assets may be a disproportionately large slice of their portfolios, a problem exacerbated by valuations lagging declines in public markets. On the other are newer dabblers in the asset class who are tempted by the chance to build exposure rapidly to a variety of private assets by buying a secondhand fund stake.

The supply-demand dynamics seemingly favor buyers: Transactions are typically conducted at a discount to the net asset value of the fund (although the true haircut depends on whether the NAV is accurate).

For the selling LP, realizing their interest below NAV is the price paid for securing cash to invest elsewhere. An alternative to swallowing that discount would be to borrow against the fund stake, but the rates here are steep, as Bloomberg News reported Friday.

Secondary investors may see lower gains on a money-in, money-out basis versus conventional buyouts. But they don’t have to wait so long for the fund to mature, so the payback comes faster and the internal rate of return may still be comparable.

Small wonder capital continues to flow into secondaries. Goldman Sachs Group Inc.’s asset-management arm last month closed a fundraising $14 billion, following a $10 billion fund in 2020. It also garnered $1 billion for a secondaries fund focused on infrastructure, while Blackstone Inc. in January raised a record $22 billion fund to invest in both fund stakes and underlying portfolio assets.

The risks to secondaries as a subsector are clear. Competition could narrow the discount at which transactions are done — good news for fund sellers, but a recipe for disappointing returns for buyers. A revival of M&A and initial public offerings would enable buyout funds to sell assets and return cash to LPs the old-fashioned way.

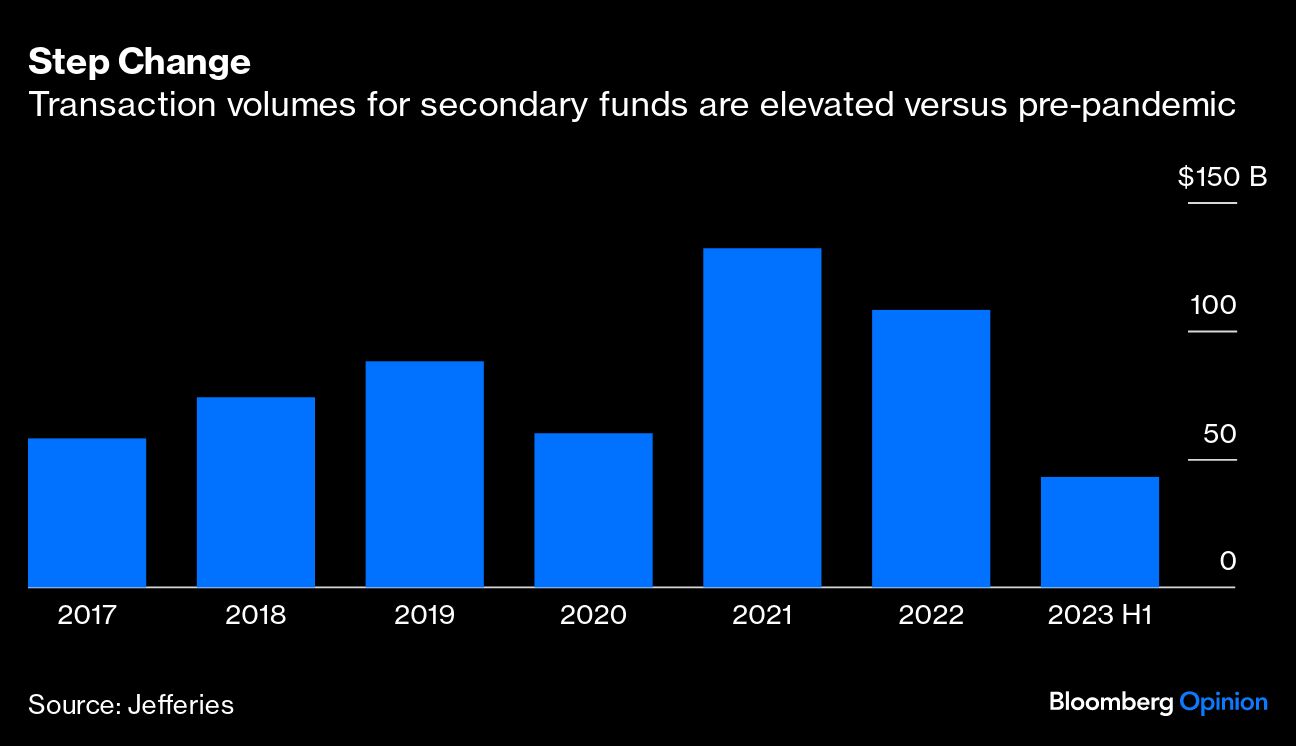

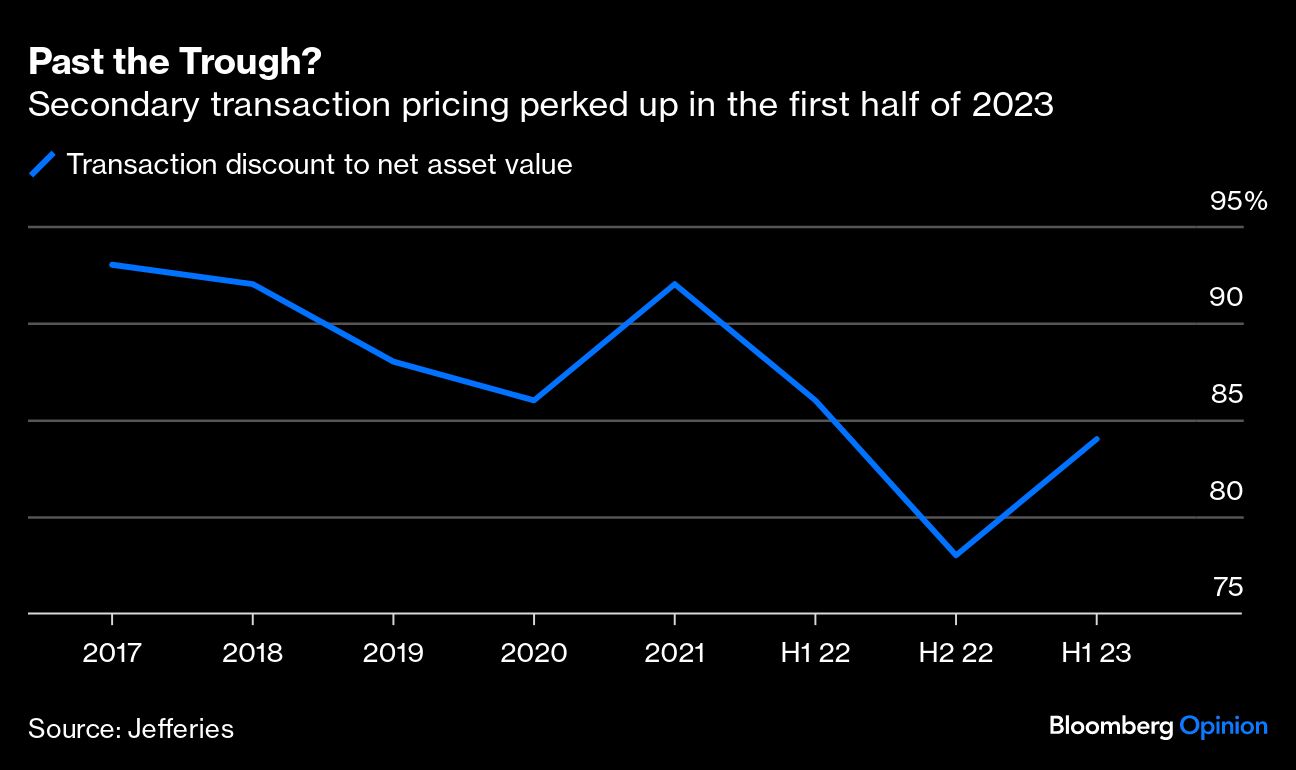

Indeed, the latest review of the industry by investment bank Jefferies Financial Group Inc. found average NAV discounts in secondaries transactions jumping to 84% from 78% between the end of December and the end of June. Global transaction volume in secondaries fell 25% year-over-year in the first half, and Jefferies lowered its forecast for the full year to at least $100 billion from $120 billion or more.

Still, activity remains higher than it was pre-pandemic. And Goldman et al. could enjoy a strong negotiating position as providers of liquidity to LPs for some time. Not many firms have the technical capability to run due diligence on fund stakes. This is a concentrated sector, with fundraisings historically dominated by the top 10 most active participants, McKinsey & Co. points out. Secondaries are still a minnow in a private assets industry with more than $10 trillion under management.

And while the motivations of selling LPs vary, one driver remains in place: Many are simply overexposed to private markets. This is not just a technicality due to private and public assets valuations moving at different speeds. The more fundamental issue is the spendthrift funneling of ever-more money to private markets after the 2008-2009 crisis. With the buyout industry in overdrive, investors recycled private equity proceeds back into the next fundraising, seemingly trapped in a use-it-or-lose-it mindset. When rates abruptly rose, the merry-go-round stopped, cash returns dived and indigestion set in.

Hopefully, the normalcy of secondaries won’t prevent investors from being more disciplined in their allocations between private and public markets in the future.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Chris Hughes