Economists, policymakers and politicians are used to there being two variables that serve as a scorecard for how the public feels about the economy — unemployment and inflation. A year ago, when inflation was at 40-year highs, public unhappiness made sense. The thinking at the time was that the Federal Reserve would raise interest rates, inflation would come down, and if that could happen without a surge in unemployment, economic confidence would rise.

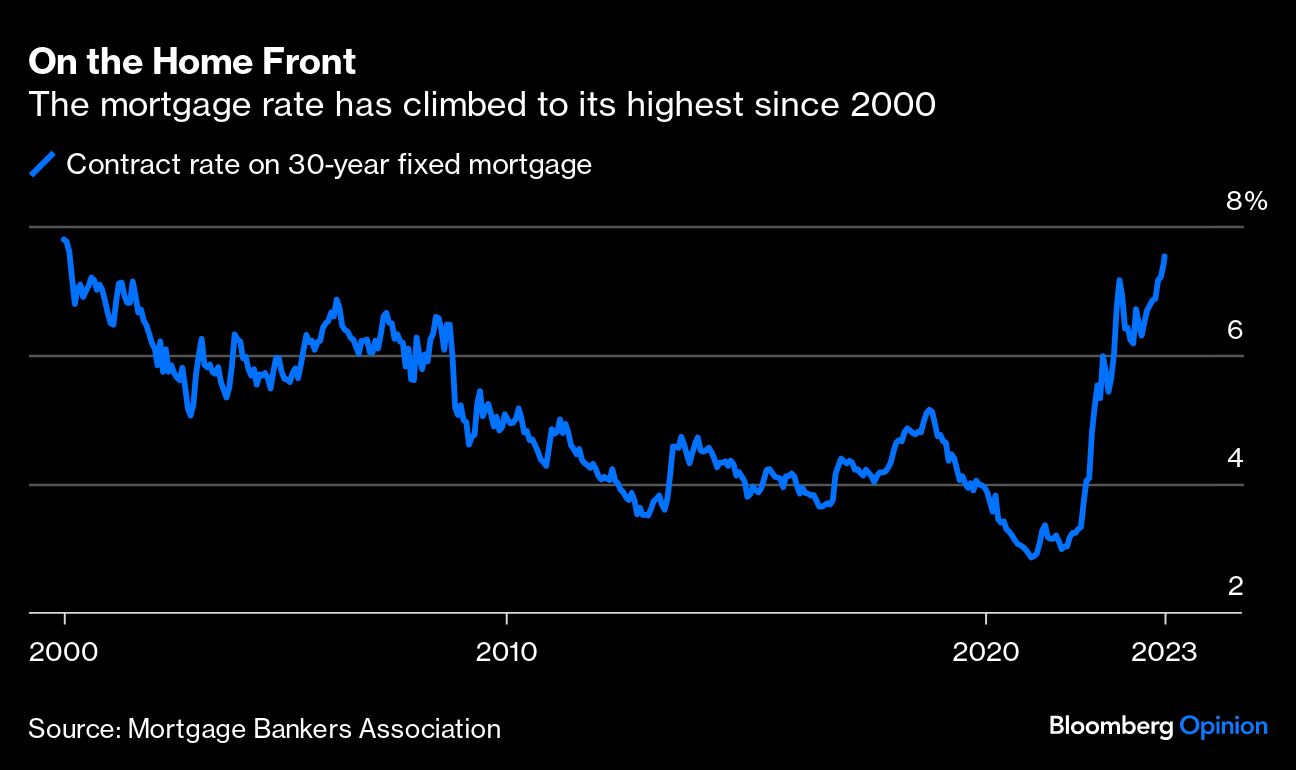

The Fed, inflation and unemployment have played out remarkably well so far, but confidence has not been restored in the way people had hoped. The rise in interest rates is part of the problem, particularly at the longer end of the bond market’s yield curve which influences products such as mortgage rates. Inflation is falling yet mortgage rates are climbing — this wasn't supposed to happen. And while it’s the Fed’s job to control price pressures, if structurally high interest rates are the problem, that’s a job for Congress. Unfortunately, the events of the past week show that there’s currently no political will to do anything about it.

Higher longer-term interest rates at a time of falling inflation show up in rising real interest rates — essentially, the rate once we’ve accounted for the market’s expectation of future inflation. Market-based measures of inflation expectations have been stable this year, so the spike in 10-year Treasury yields has pushed 10-year real yields to levels higher than we've seen for most of the last 20 years.

Households and businesses don't borrow at the Treasury rate, of course, they pay a premium above that. So, 30-year mortgage rates are currently above 7.5% while market expectations of future inflation are around 2.3%. The gap of more than 5 percentage points is something that hasn’t persisted since the 1990s. It was closer to 2.5 percentage points in the 2010s.

Perplexingly, the gap has been widening despite the downtrend in inflation. Between the end of 1981 and the end of 1984, the Fed’s preferred measure of inflation fell by 3.6 percentage points accompanied by a 3.8 percentage point drop in 30-year mortgage rates — falling inflation, falling mortgage rates. In the past year, the Fed’s preferred inflation gauge has fallen by 1.3 percentage points while 30-year mortgage rates have risen by around 1 percentage point. We're in somewhat uncharted territory here.

There are scenarios where this divergence proves temporary. Maybe bond investors need more data to convince them that inflation is trending lower on a sustained basis. Maybe the bond selloff of the past month reflects the inherent volatility and rhythms of the market. Maybe the effects of the Fed’s aggressive rate tightening campaign have not yet been fully felt in the real economy, and as they slow economic growth, longer-term interest rates will decline.

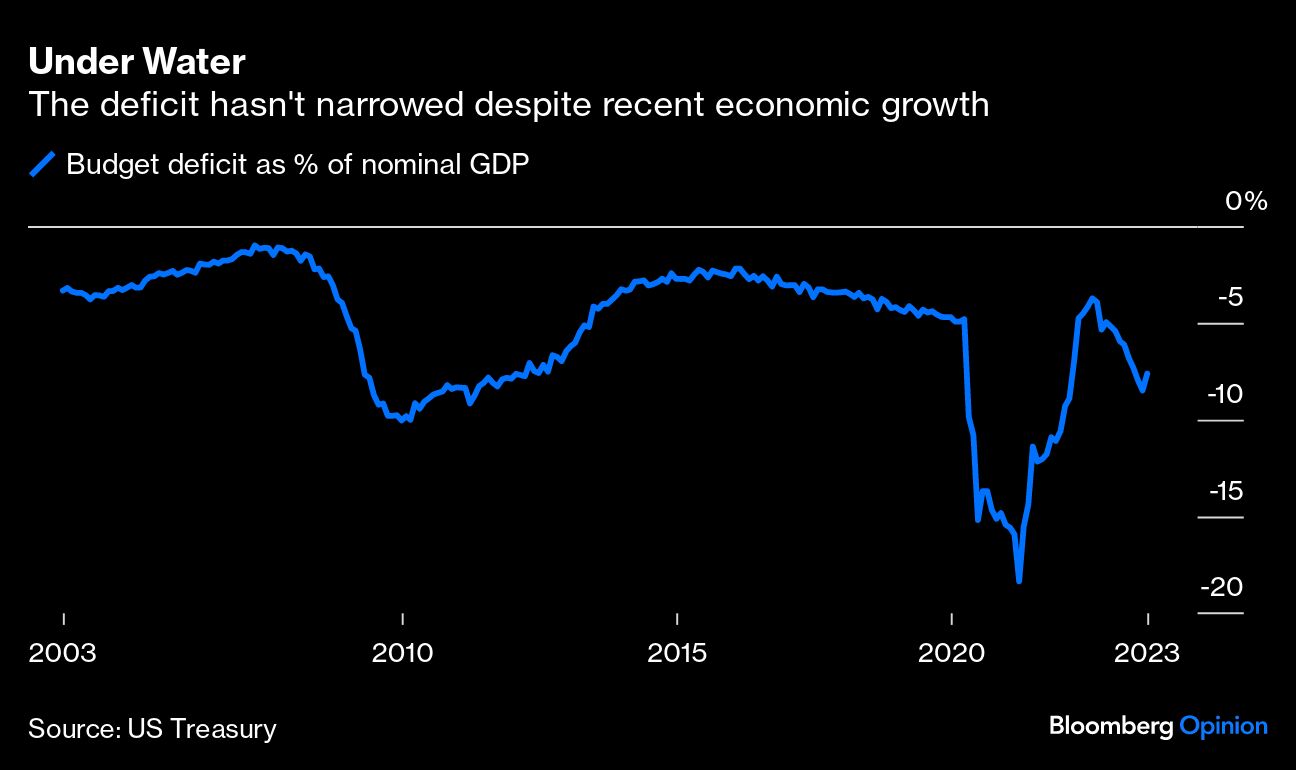

But it’s reasonable to wonder if the structural budget deficit and elevated levels of government debt that people have worried about for years are finally affecting markets. There was a feeling last year that high inflation would drive a “red wave” in the 2022 midterm elections, helping Republicans take control of Congress with a mandate to rein in spending and reduce deficits. That largely hasn't happened.

Through the first 11 months of the fiscal year ending Sept. 30, the federal deficit was $1.5 trillion, up sharply from $946 billion in the comparable period a year earlier — and during a period of economic well-being. Each annual deficit adds to an already staggering amount of publicly held debt at $26.4 trillion.

Yet Congress raised the debt ceiling in June without the kind of spending cuts fiscal conservatives had hoped for. And the weekend deal that prevented a government shutdown through at least mid-November only cut aid to Ukraine, costing House Speaker Kevin McCarthy his job.

Notably, 10-year Treasury yields rose 22 basis points between Monday and Tuesday with the stock market selling off, suggesting investors weren’t happy with what transpired.

If reducing the budget deficit is in fact what’s needed for longer-term interest rates to fall, it’s not clear that the two major American political parties are currently situated to do this. Former President Donald Trump repositioned the Republican Party to no longer prioritize cutting entitlement spending, helping him win older voters in key Midwestern states. President Joe Biden has reoriented the Democratic Party by pledging that there will be no tax hikes for Americans making less than $400,000 a year, helping him win over upper-middle-class voters in key states like Georgia and Arizona. With the prospect of a presidential election rematch between the two looking more likely than not, it doesn't appear that deficit reduction will be a key theme in the campaign.

Without any obvious catalyst for longer-term interest rates to fall, those upset about rising borrowing costs may be stuck in a sort of political and economic purgatory for some time. And without a decline in interest rates, a return of inflation to the Fed’s target of 2% may be seen as an incomplete mission by the public.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

More Real Estate Topics >