A robust earnings season could be all it takes to fuel a year-end rally on Wall Street, eclipsing recent jitters from geopolitical tensions.

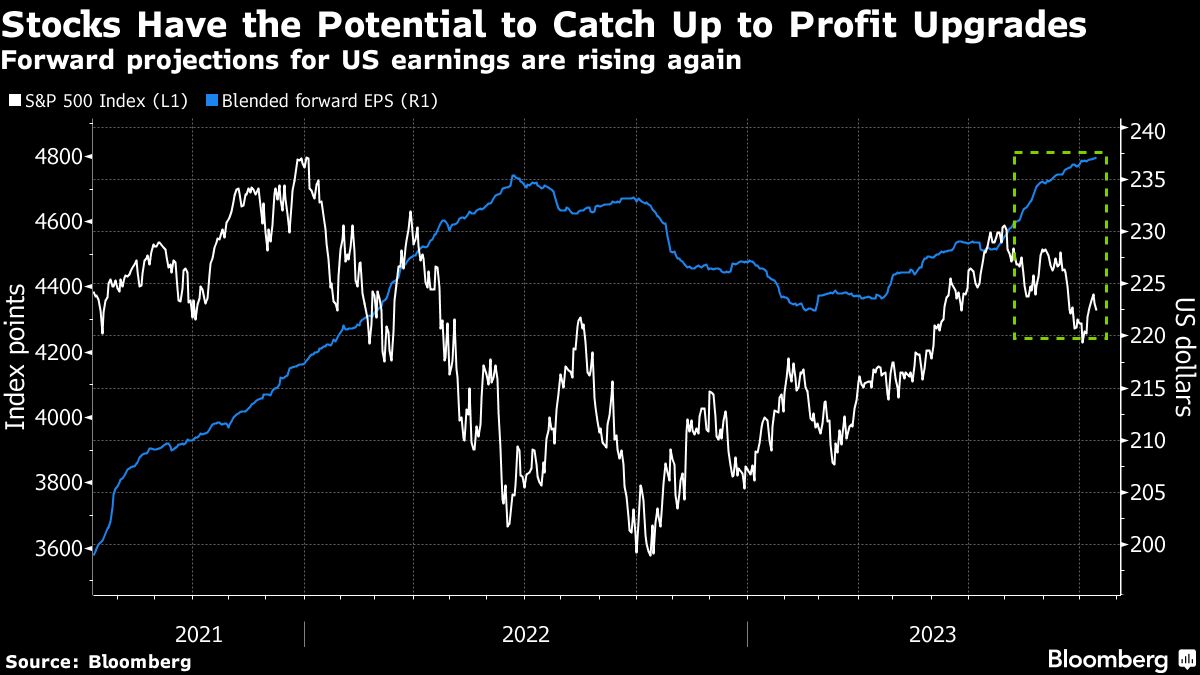

Having endured a turbulent summer amid worries about higher-for-longer interest rates, the S&P 500 Index has been drifting lower since hitting a July peak, bringing valuations closer to long-term averages. With analysts ramping up their earnings estimates and bond yields starting to retreat from 16-year highs, it leaves scope for gains.

“The market overshot to the downside in recent weeks due to the blowout top in yields,” said Thomas Hayes, chairman of Great Hill Capital LLC. “But with some calmer seas ahead for yields, the focus can get back to fundamentals — which are poised to be better than estimates — and set the stage for a year-end rally that most managers are not yet positioned for.”

Early reports suggest Corporate America is on the right track. The S&P 500 constituents that have reported quarterly earnings so far have beaten analysts’ estimates by 9%, thanks to robust margins and higher productivity, data from Bank of America Corp. shows.

Then take a look at share valuations. The S&P 500 now trades at 18.7 times forward earnings, having slipped from this year’s high of about 20, reached in July, according to data compiled by Bloomberg. The equal-weighted S&P index — which pares the influence of the rates-sensitive technology behemoths — is even cheaper, displaying a price-to-earnings ratio of 15, compared with a 10-year average of 17.

What’s more, over half of the participants in BofA’s latest investor survey expect a year-end rally, though they highlighted war in the Middle East and persistent inflation as posing risks to this outcome.

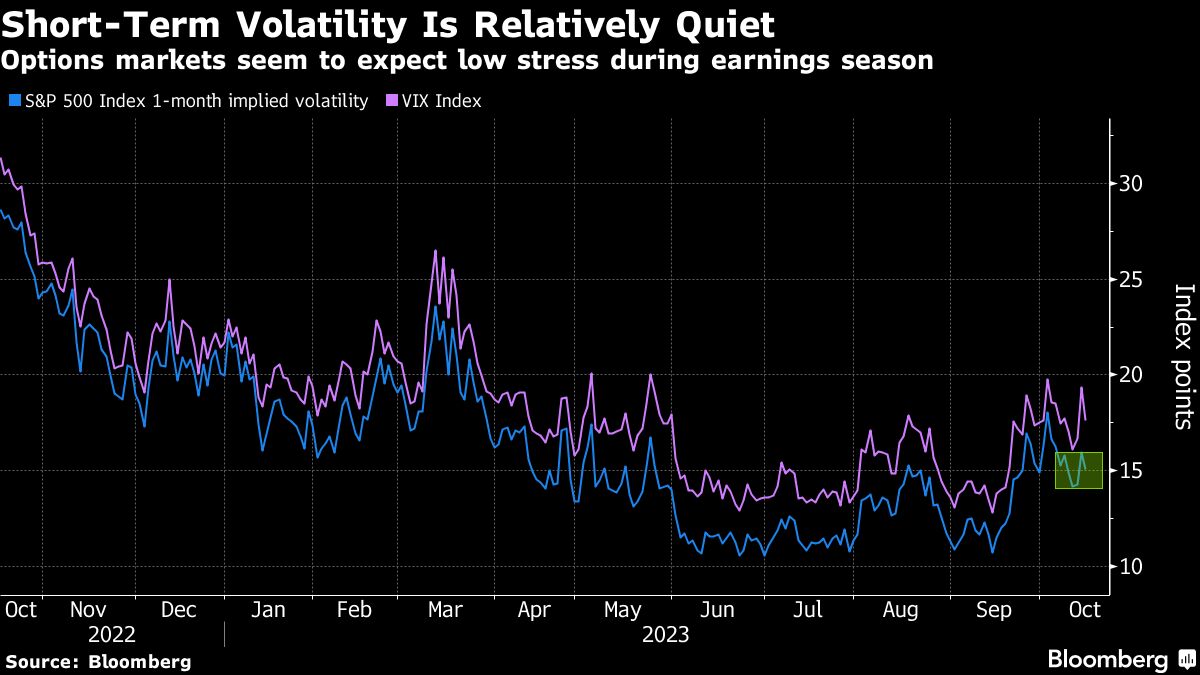

The options market is flashing positive signals, too. One-month implied volatility on the S&P 500 is among the lowest in the curve through January 2024, suggesting investors don’t view the earnings season as a big risk event. The gauge trades at around 15, significantly lower than the Cboe Volatility Index’s 17.

Of course, the low-volume picture could also reflect dangerous complacency, carrying the potential to blow up in investors’ faces should earnings underwhelm.

Some strategists fret about the recent weakening in earnings revisions. An index compiled by Citigroup Inc. shows profit downgrades have outnumbered upgrades for five weeks in a row. If upgrades fail to pick up again, it would mean other risks, including around economic uncertainty, are seeping into the outlook, according to Morgan Stanley strategist Michael Wilson.

That would reduce the odds of a fourth-quarter rally, Wilson warned.

Finally, there’s the risk that shares linked to the US economic cycle are reflecting excessive optimism about the world’s biggest economy. While business activity has indeed bounced in recent months, the rally in cyclical sectors such as oil and gas, semiconductors and autos appears to have outpaced the growth acceleration.

For many, that implies economic growth at a pace reminiscent of the sharp rebound from the Covid-induced slump of 2020 — but that was the exception rather than a typical recovery pattern.

Still, Bloomberg Intelligence strategist Gina Martin Adams said the direction of business activity indicators may matter more for stocks than actual levels. Typically over the past decade, Purchasing Managers’ Indexes have tended to peak before stock-market highs are reached, according to Martin Adams. PMI troughs, on the other hand, are less consistent as leading indicators for equity markets, she added.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Sagarika Jaisinghani, Michael Msika