Guaranteed Lifetime Income is a Better Solution than Taxable Bonds

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

With interest rates at near 20-year highs, guaranteed lifetime income locks in those rates for the rest of one’s life, creating better retirement outcomes.

If you own a home, then you’re probably wishing you had locked in a mortgage rate back in 2020 when 30-year mortgage rates were under 3%. Buying a home in 2023 is not nearly as attractive when interest rates are at near 20-year highs.

While high interest rates are not good for borrowers, they are for those who lend money at high interest rates. What if there was a product that allowed you to be the lender and lock in today’s high interest rates for the rest of your life? Guaranteed lifetime income is one such product. By lending money to an insurance company today, you are locking in these high interest rates for the rest of your life while also benefiting from mortality credits that improve the return, hedge against interest rate risk, and are tax efficient.

As I’ll show in this article, guaranteed lifetime income products provide significantly better retirement outcomes than traditional retirement solutions for the following reasons:

1. Access to long-term bond yields without interest rate risk

At their core, insurance and annuity products provide clients access to the long-term bond yields of an insurance company’s investment portfolio without having to absorb the interest rate risk. The insurance company absorbs that risk on behalf of the client in exchange for a spread earned on the assets between what the portfolio earns and what they’re crediting to clients. This gives clients higher risk-adjusted yields than just investing in short- or long-term bonds directly.

2. Access to risk-pooling and mortality credits

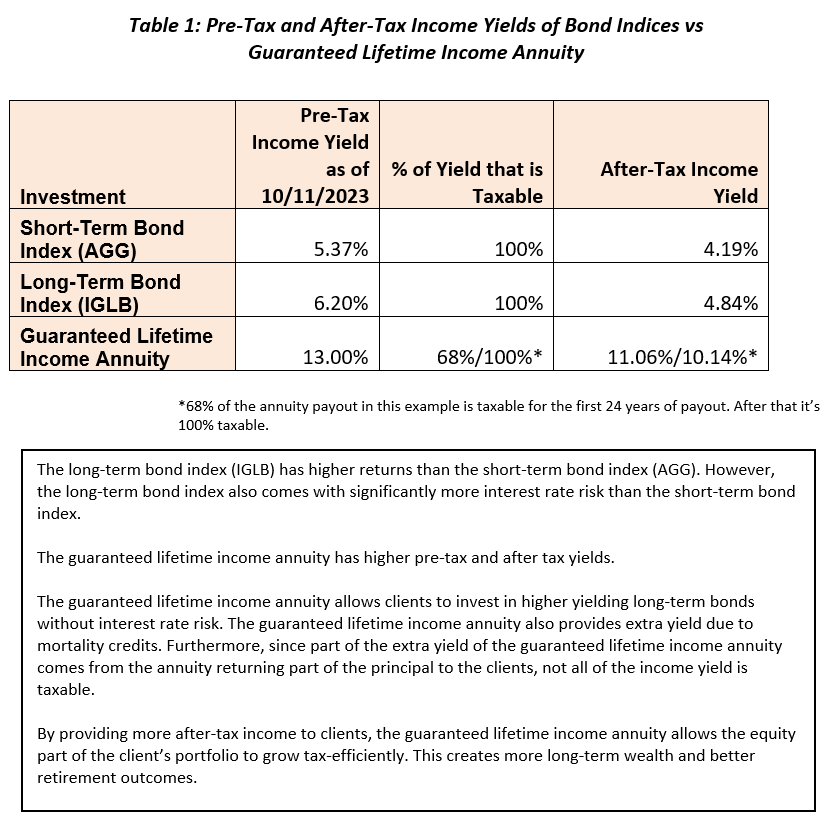

Guaranteed lifetime-income annuities also provide clients to access higher yields than just investing in long-term bonds due to risk-pooling and the benefits of mortality credits. In other words, since the insurance companies know that some clients will die early, they can provide clients higher income yields than those clients would achieve if they invested in long-term bonds directly – as we saw in Table 1 above.

Some clients will die early, and receive less in income payouts than the amount of money they invested. The investment was a loss for them. But it’s a gain for other clients, because the income payouts that would have gone to the clients who died early are shared with the clients that lived.

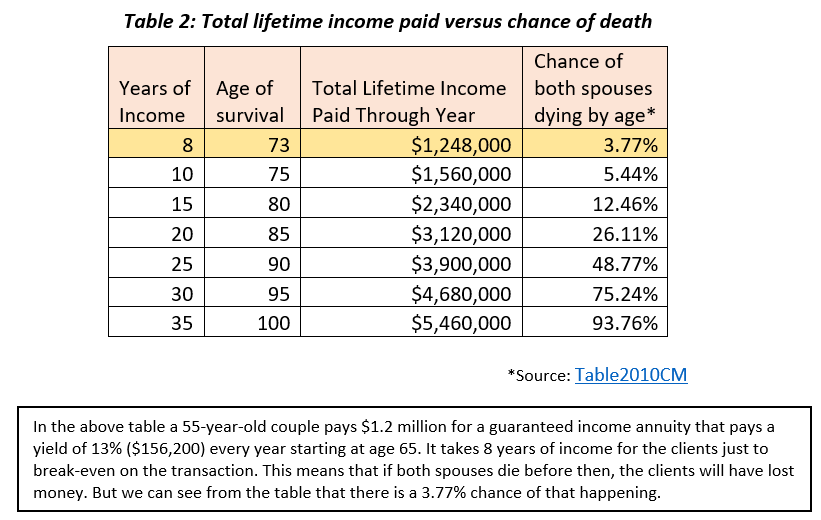

There are a couple of points to note here. The number of clients who invest in guaranteed lifetime-income annuities who die young, and therefore earn less in annuity payouts than the amount they originally invested, is extremely low. We can see this in the table below, where fewer than 3.77% of clients will receive less than the amount they originally invested.

Even for the clients who die early, this loss is partially offset by the fact that since those clients were able to access more retirement income from their guaranteed lifetime-income annuity, their tax-efficient equity portfolio compounded more effectively without having to be sold to provide additional income. We’ll see the benefit of this more clearly when we compare using traditional bond allocations versus allocations to guaranteed lifetime income annuities.

3. Tax-efficient income distributions

Another key advantage of guaranteed lifetime-income annuity products over bonds is that their payouts have favorable tax treatment compared to bond-coupon payments. This is because bonds return only your principal at maturity, whereas guaranteed lifetime-income annuity products slowly return your principal over time. Since principal payments back to the client aren’t taxable, whereas bond coupon payments are fully taxable, that means a $1,000 guaranteed lifetime income annuity payout will incur less in taxes than a $1,000 bond coupon payout. This is why in table 1 above the after-tax yield of the guaranteed lifetime-income annuity was 11.06% for the first 24 years of payouts and 10.14% afterwards, but only 4.684% for the long-term bond index (IGLB).

Using guaranteed lifetime-income instead of bonds increases the probability of successful retirement outcomes, after-tax wealth, and reduces volatility in retirement outcomes.

A great way to quantify the value of guaranteed lifetime income is to replace the bond part of the portfolio with guaranteed lifetime income and have that be the primary basis for retirement spending.

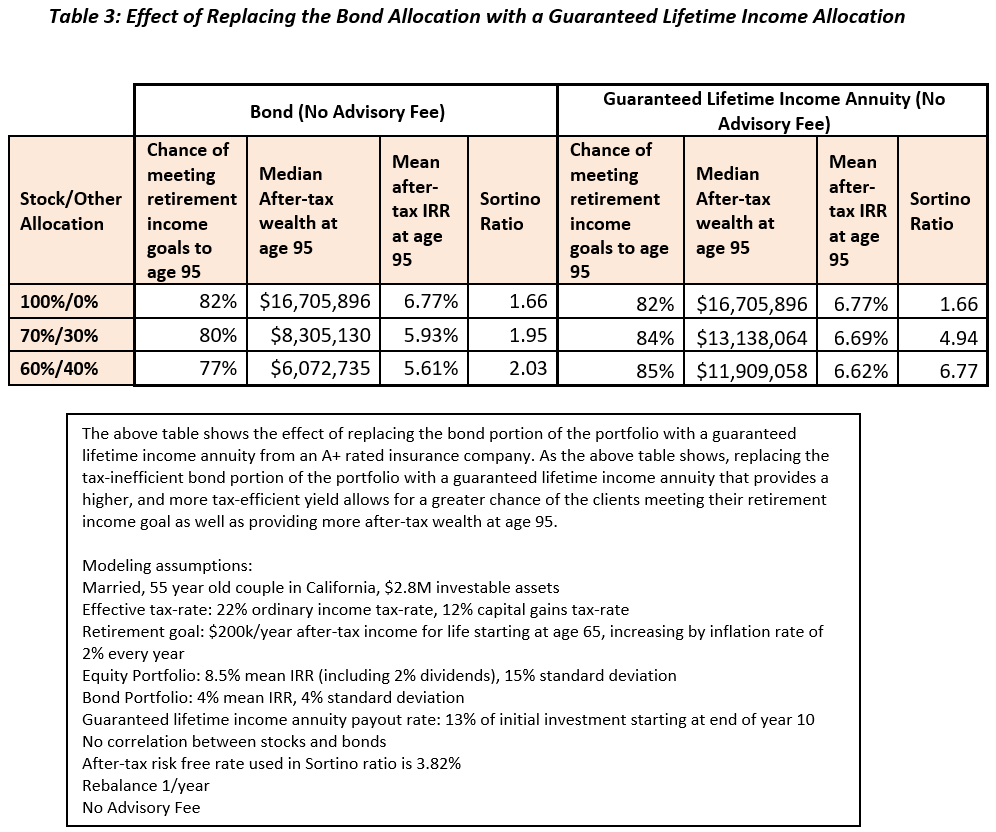

We can see the effect of this by looking at the chance of a 55-year-old married couple meeting their retirement goals if they were to replace the bond allocation with a guaranteed lifetime-income annuity that starts paying at age 65 when they retire and pays as long as at least one of them is alive. For example, instead of a 70% stock/30% bond asset allocation, the client would use a 70% stock/30% guaranteed lifetime-income annuity allocation.

As the above table shows, using a guaranteed lifetime-income annuity in place of a bond allocation provides greater after-tax wealth and reduced volatility:

1. Using the guaranteed lifetime-income annuity improves chance of meeting retirement goals

In both the 70/30 and 60/40 portfolios, the chance of the client meeting their inflation adjusted $200,000/year is increased by using the guaranteed lifetime-income annuity instead of the bond allocation due to the high after-tax yield of the former. In the 70/30 portfolio, the chance of the client meeting their annual retirement income goal is increased from 80% to 84% by using the guaranteed lifetime-income annuity in place of a bond allocation. With the 60/40 portfolio it is increased from 77% to 85%.

2. Using the guaranteed lifetime income annuity increases after-tax wealth significantly

The greatest impact of using the guaranteed lifetime-income annuity is on the after-tax wealth that the client leaves to their beneficiaries at age 95. For example, using a 70% equity/30% guaranteed lifetime-income annuity allocation increases the median after-tax wealth at age 95 by 58% from $8,305,130 to $13,138,064. The 60% equity/40% guaranteed lifetime-income annuity allocation increases this wealth by 96% over its 60% equity/40% bond counterpart ($6,072,735 to $11,909,058).

3. Using the guaranteed lifetime income annuity reduces the volatility in the portfolio

While increasing the median after-tax wealth of a retirement solution is important, so is reducing the volatility of the downside scenarios. The guaranteed lifetime-income annuity improves upon this significantly over the use of taxable bonds. This is because the value of a stock-bond portfolio can reduce to $0 and fail to produce any retirement income portfolio for the client from that point forward. But with an equity-guaranteed lifetime-income annuity portfolio, even if the equity portfolio reduces to $0, it still produces income. While it isn’t the full retirement income of $200,000/year on an inflation-adjusted basis that the client wanted, it’s still $80,000-$110,000k/year of annual income that they otherwise wouldn’t have had if they went with a stock-bond portfolio instead that had no value. We can measure this reduction in downside volatility by looking at the Sortino ratio in each of the scenarios. For the 70/30 portfolio, the Sortino ratio increased by 152% from 1.95 to 4.94 when the guaranteed lifetime-income annuity was used instead of the bond allocation. For the 60/40 portfolio, the Sortino ratio increased by 232% from 2.03 to 6.77.

Most guaranteed lifetime-income annuities are commissionable. This means that there is no ongoing fee as there would be with an advisor. The results shown in the table account for the fact that the commission to the agent has already been paid. But an advisor that charges an ongoing fee takes it from the portfolio. This would make the traditional equity-bond retirement results look significantly worse – as we saw in a previous article I wrote. Therefore, an advisor using a traditional equity-bond model as a retirement solution and charging an ongoing fee on both the equity and bond portfolio amounts would have significantly worse results for their clients than an advisor who is charging an ongoing fee only on the equity portfolio and using a commissionable guaranteed lifetime-income annuity in place of the bond portfolio.

The insurance industry is becoming more friendly to RIAs that charge an ongoing fee by introducing guaranteed lifetime-income annuity products that allow RIAs to charge fees on the assets. While guaranteed lifetime-income annuity products that RIAs can charge their fee on are currently not as competitive as their commissionable brethren (that charge an upfront fee), these “fee-only” products allow RIAs that otherwise wouldn’t use annuities to do so in a way that aligns with their business model. And ultimately, even these fee-only annuities provide better retirement outcomes for clients than just using a traditional stock-bond portfolio as a retirement solution.

The failure of traditional retirement models

As Table 3 above shows, if your entire retirement strategy – or the one your financial advisor devised for you – consists only of shifting assets away from stocks and towards bonds, it will cost you and your beneficiaries millions of dollars over the course of your retirement without providing any guaranteed protection that you’ll be able to meet your retirement goals. The problem with the traditional retirement approach used by AUM-based advisors is that it doesn’t properly account for the fact that the stock part of the portfolio is responsible for generating tax-deferred (or tax-free with step-up in basis) wealth, while the bond portion of the portfolio is responsible for providing yield and downside protection against sequence of return risk.

What are ways that would more effectively use the tax-efficient nature of stock investments with the yield and downside protection that bonds provide?

The first step is to use bonds to defer the taxation on their gains until maturity, hedge against interest-rate risk, and add risk-adjusted yield. The more bonds are used for yield, the less has to be withdrawn from the tax-efficient, higher earning stock portfolio.

This is exactly what guaranteed lifetime-income annuity products provide.

Furthermore, since these products aren’t underwritten, and wealthier people live longer than non-wealthy individuals, wealthier clients in good health can essentially receive a pricing benefit at the expense of less wealthy and less healthy individuals who purchase annuities. This pricing arbitrage helps wealthy people who are in good health and cannot be replicated in capital markets.

Furthermore, while traditional retirement accounts like IRAs allow for tax-deferred or tax-free growth, HNW clients are usually phased out from utilizing them. Insurance products like guaranteed lifetime-income annuities are one of the few vehicles HNW clients can use and benefit from tax-deferred growth.

Another key problem with traditional retirement models is that they seek to protect against downside risk by regularly rebalancing the portfolio between stocks and bonds.

While this reduces risk in the portfolio, it also reduces long-term after-tax wealth. Shifting assets away from an equity portfolio that is earning 8% tax efficiently towards a bond portfolio that is earning 4% in a tax-inefficient manner provides downside protection, but it hurts long-term after-tax wealth.

Using a product like a guaranteed lifetime-income annuity allows the stock portion of the portfolio to grow at a faster rate without the constraints of rebalancing. This is because the lifetime-income product generates a much higher after-tax income yield than the equivalent taxable-bond portfolio, which means less of the higher earning, tax-efficient stock portfolio has to be sold to generate this retirement income yield. This allows the stock portfolio to grow at a faster rate – without the limitations of rebalancing the portfolio towards bonds – since the stock portfolio is only sold to fill-in gaps to the extent that the income yield from the guaranteed lifetime-income annuity falls short of the desired retirement income goal. And as I mentioned previously, part of the guaranteed lifetime-income annuity is a return of principal, which means that the client is getting the benefit of investing in long-term bonds and having their principal returned over time without the interest rate risk that comes with investing in those bonds. This allows the yield portion of the portfolio to cover the sequence-of-return risk in the early years while allowing the stock portfolio to generate wealth over the long-term. The higher-earning, tax-efficient part of the portfolio coming from the unrealized growth of the equity component compounds in a way that is not possible with a traditional retirement portfolio model. This is why the after-tax wealth at age 95 was so much higher in the scenarios in Table 3 when a guaranteed lifetime-income annuity was used in place of a bond allocation.

The guaranteed lifetime-income annuity provides qualitative benefits that taxable bonds cannot.

In addition to the quantitative benefits described above, several qualitative benefits are not accounted for in my analysis:

1. Insurance protection/guarantees versus credit risk of bonds

Investing in long-term bonds via an insurance product comes with significantly higher default protections than investing in other investment-grade, long-term bond portfolios. The insurance company is well-regulated and required to have sufficient reserves to back the payments it is making. It is protected via state guarantee associations and economic interests that protect insurance companies from failing to deliver on their obligations. No such protections come with corporate bonds. Corporate bonds carry the full credit risk of their issuers without such protections. Investing directly in an A-rated corporate bond is not the same risk as buying an insurance product from an A-rated company.

2. Pricing arbitrage

As I mentioned previously, most lifetime income products don’t require underwriting. As a result, clients in good health can receive more of the mortality credit from these products than clients in worse health. Since wealthier people have better access to healthcare and live longer than their non-wealthy counterparts, wealthy clients benefit from the guarantees provided at the expense of other purchasers.

3. Probability versus certainty and volatility reduction

A Monte Carlo simulation projecting a probability of success (including the analysis I did in this article) is heavily dependent on the capital market assumptions assumed. While we know in hindsight what the capital markets have returned historically, we have no idea how they will perform over the next 30 years of a client’s retirement. Using insurance products like guaranteed lifetime-income annuities reduces volatility in the portfolio to a significantly greater extent than direct-bond investments. Furthermore, in a world in which defined benefit plans are disappearing and being replaced by defined contribution plans, consumers at large want protection and guaranteed income that they can rely on.

Conclusion

The use of taxable bonds as a diversifier of risk in retirement is heavily flawed because bonds are low yielding, highly taxable, subject to interest rate risk, and can be positively correlated to stock returns when bond returns are negative (e.g., like in 2022 when both bonds and stocks took losses). Insurance products like guaranteed lifetime-income provide a way for individuals to invest in bonds with enhanced protections and mortality credits in a way that allows the portfolio to grow at a faster rate than would otherwise be possible if tax-efficient assets like stocks were constantly being sold and rebalanced with a bond portfolio.

The downside with insurance products is that they often come with heavy surrender charges if clients choose to exit the investment early. But so do traditional retirement vehicles like 401ks and IRAs – which most high-net worth earners are either phased out of contributing to completely or limited in the contributions they can make. These traditional retirement plans encourage long-term wealth building through retirement plans in exchange for asking participants to forego liquidity. Insurance products that provide retirement solutions are asking for the same thing. While the surrender penalties for using insurance products are more severe, they are also providing significantly greater retirement benefits than can be achieved from investing in bonds through either taxable accounts or retirement vehicles alone. As more fee-only guaranteed lifetime-income annuity products come to the market, more RIAs will be able to use these products in a way that both compensates them for using them and creates better retirement solutions for their clients.

Rajiv Rebello, FSA, CERA is the principal and chief actuary of Colva Actuarial Services . Rajiv works with UHNW clients, RIAs, family offices, estate attorneys, and CPAs to help them implement fiduciary life insurance, annuity, and alternative investment solutions (including tax-free PPLI solutions) into their current practice to help increase clients’ after-tax returns and reduce volatility in their clients’ portfolios. Rajiv can be reached at [email protected]

Income is evolving, is your portfolio? Join industry experts as they dive into fixed income markets and a range of income strategies. Register for our next symposium, October 27 at 11 am ET. Click here.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Live Virtual Event: Join Now

Upcoming Virtual Events View All