Corporate America’s spending on share buybacks, a driver of the US stock market rally for over a decade, is slowing in the face of higher-for-longer interest rates and an uncertain economic backdrop.

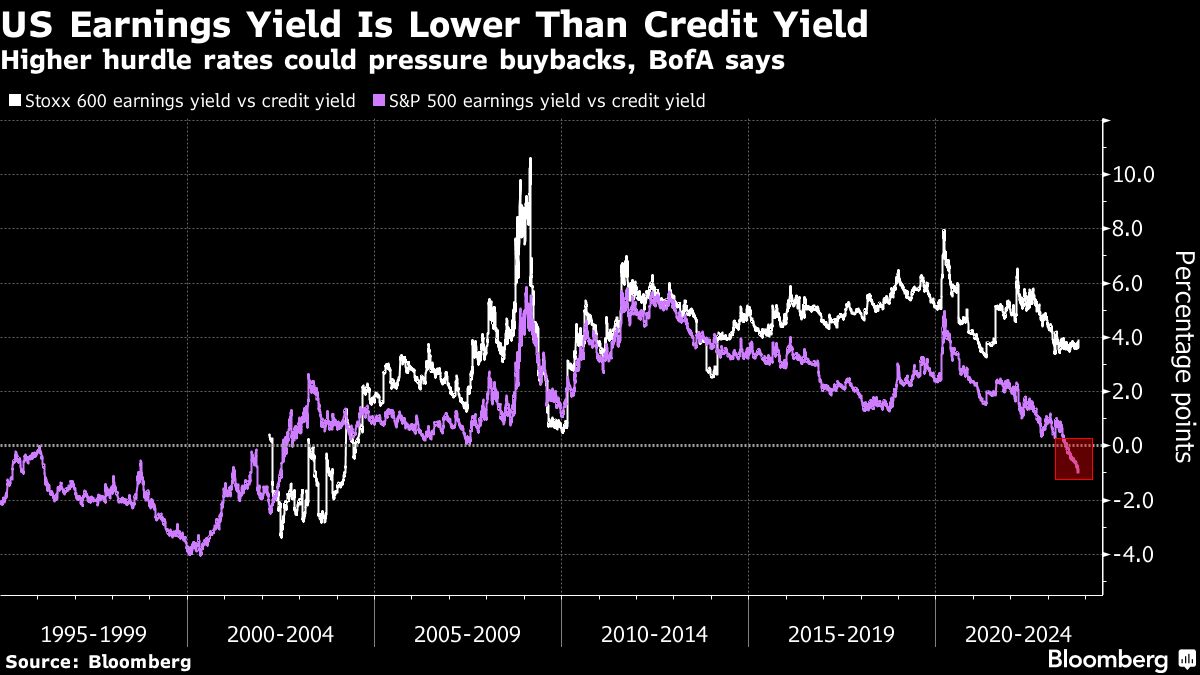

US stock repurchases are tracking a 3% decline in the third quarter after falling 26% in the previous three months, according to Bank of America Corp. strategists. Though the reversal appears to be becoming less severe, BofA says tightening credit conditions and increased cost of capital mean buybacks remain at risk.

Companies in the S&P 500 spent a record $923 billion purchasing their stock last year, extending a trend that gathered pace after the global financial crisis in 2008 as interest rates plunged to near zero and stayed low for the next decade. While the practice gets attacked by politicians and academics who argue the cash should be used to boost long-term growth, buybacks can be attractive for investors, boosting metrics like earnings per share because profits get divided between fewer shares.

“Buybacks were a post-GFC phenomenon, with companies taking advantage of cheap financing costs to repurchase their own stocks,” BofA strategists led by Savita Subramanian wrote in a note. That’s now at risk as the era of free money is over, with rates at 5.5% and seen staying higher, thanks to the Federal Reserve’s dogged campaign against inflation.

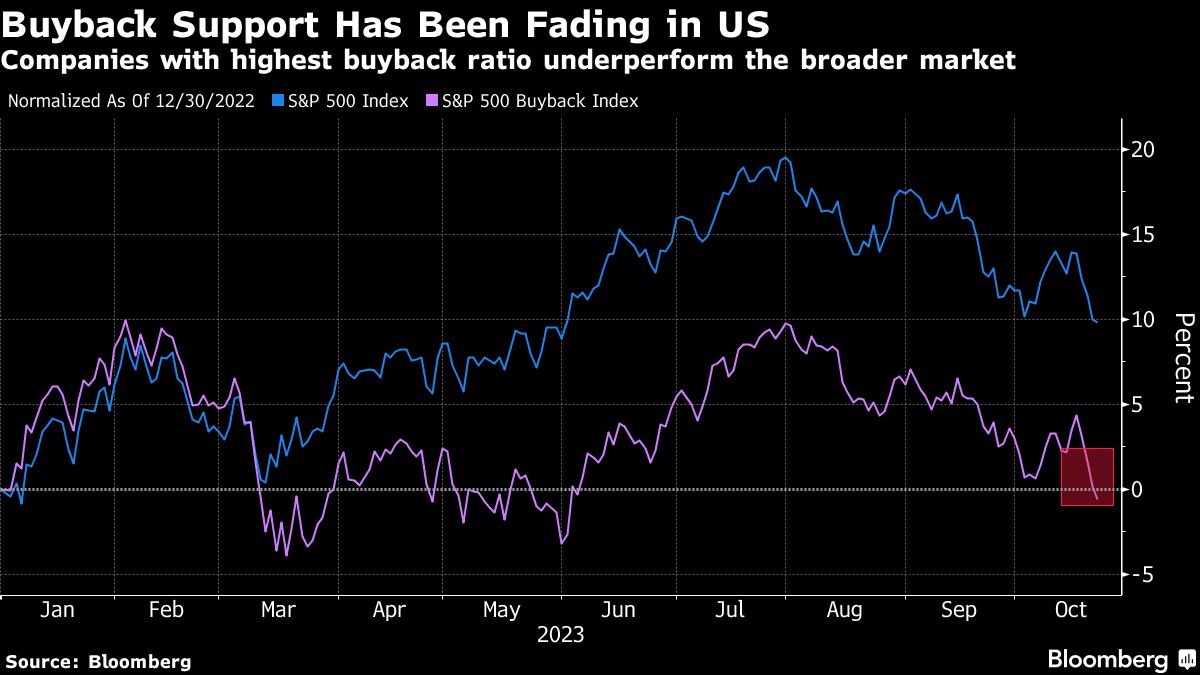

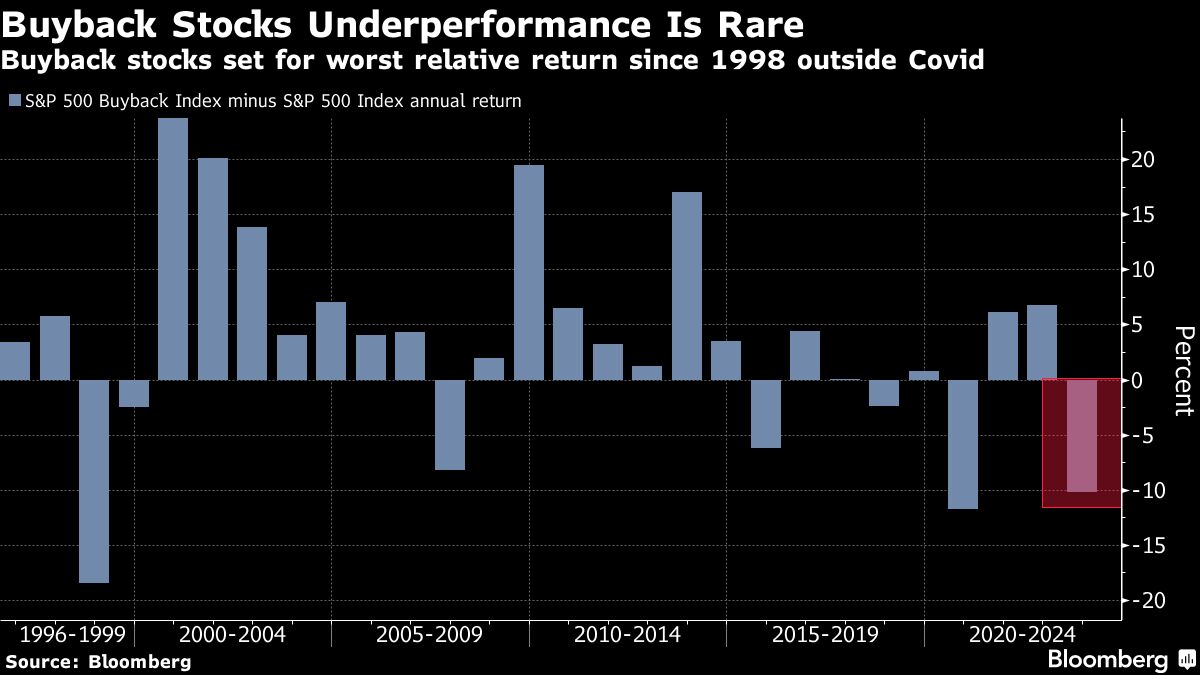

The S&P 500 Buyback Index has trailed the broader S&P 500 by about 10 percentage points this year, the worst showing since 1998 outside the pandemic year of 2020. The benchmark includes stocks such as Marathon Petroleum Corp., Valero Energy Corp., CF Industries Holdings, and Akamai Technologies Inc.

A tax on stock buybacks that took effect this year is another drawback for chief executive officers to consider, with heavyweights Apple Inc., Alphabet Inc., Meta Platforms Inc. and Microsoft Corp. among major companies that could bear the brunt of such levies. Those four have more than $110 billion in stock due for repurchase over the rest of the year.

The reporting season for technology large caps steps up a gear this week, bringing with it the potential for expanded buyback programs to support stocks in the sector.

Beyond the ranks of the cash-rich Big Tech names, companies have pursued buybacks through raising debt, an approach also faltering in the higher-for-longer rates environment. BofA says “muted debt issuance suggests buybacks are likely to remain tepid going forward.”

Major buyback news this earnings season has come largely from industries known for strong shareholder remuneration, like energy, where Chevron Corp. and TotalEnergies SA bulked up their programs. Banks, for example, have been more cautious, with Citigroup Inc. indicating that it expects to do modest buybacks in the fourth quarter.

For Goldman Sachs strategist David Kostin, buyback spending could see a modest 4% rebound next year after the predicted 15% decline in 2023. The strategists say the drop this year accompanies virtually zero earnings growth, higher interest rates, and recession concerns among corporate management.

“Buybacks are one of the most volatile uses of cash as firms adjust repurchase activity depending on the operating environment,” the strategist wrote. Kostin and his team expect the improvement in the economic climate next year, the end of the Fed hiking cycle and improving earnings growth to lead to the small pick up in activity.

Despite the slowdown, they see corporations remaining the largest buyers of US equities in 2023 and 2024.

In Europe, the picture has been different. Historically, companies in the region preferred rewarding investors through dividends. But after the pandemic, stock purchases gained popularity, according to Goldman Sachs strategists led by Guillaume Jaisson.

This faces a threat from cash-strained governments, such as those in Spain and Italy, who have already announced their intention to tax buybacks or have put temporary levies on sectors benefiting from high-interest rates, such as banks.

“Buyback is the new return,” Jaisson said, adding that they provide more flexibility than dividends, and noting a growing appetite from investors for his firm’s basket of companies high buyback yields. “However, potential taxes on buyback executions could pose a risk.”

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Michael Msika