Embattled debt investors like the look of 5% Treasury yields as they weigh the risk-versus-reward scales for the world’s biggest bond market.

The rise in yields to levels last seen before the financial crisis reflects a run of solid data, with the US economy growing last quarter at the fastest pace since 2021. And a rising tide of Treasury debt issuance, meanwhile, has prompted the return of a positive risk premium for owning longer-dated bonds.

For all the pain in the bond market — and some traders are betting there’s more to come— the notes look a lot more attractive to long-term buyers once Treasury yields are running at 5%-or-higher.

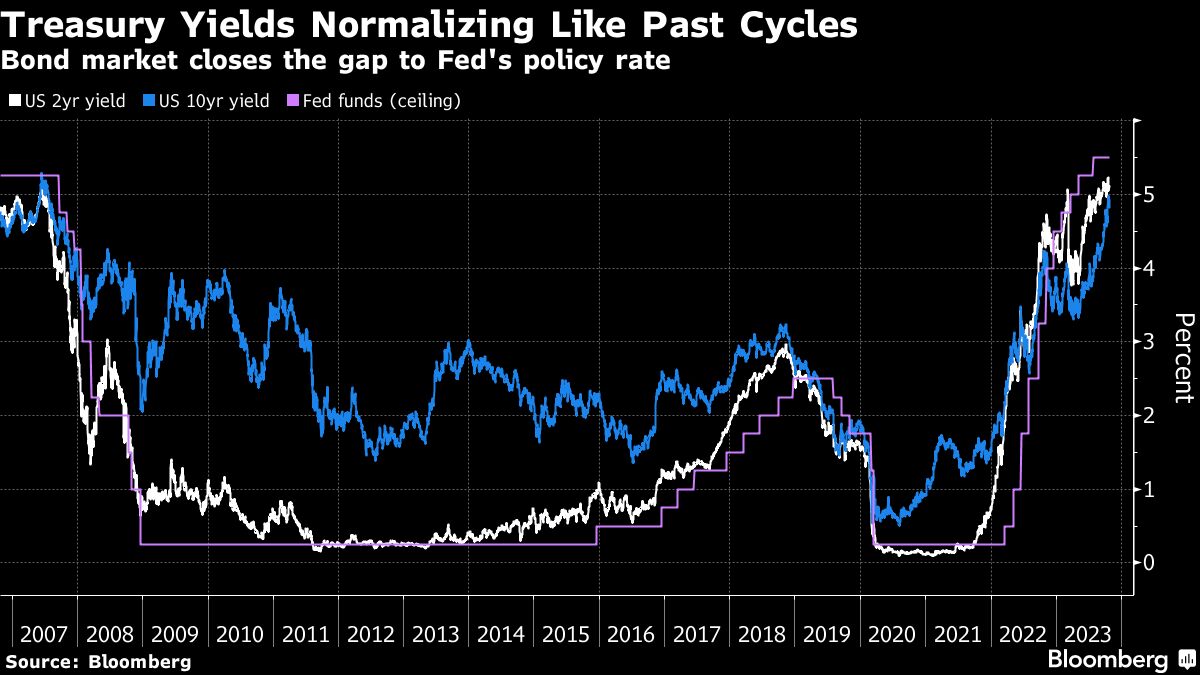

Those levels nudge them closer to the Federal Reserve’s current policy-rate ceiling of 5.5%, allowing buyers to lock in elevated income before officials eventually embark on any easing cycle.

“The arithmetic starts to move in your favor after having been out of your favor for a very long time,” said Stephen Bartolini, a fixed-income portfolio manager at T. Rowe Price. “It takes a lot larger increase now to wipe out total return over a 12-month horizon because you’re getting yield.”

Buyers emerged Thursday, spurring a drop of some 10 basis points across the Treasury curve as another round of disappointing earnings caused equities to slide. The 10-year yield was little changed at 4.85% on Friday in Asia, about 16 basis points below the 16-year high touched on Monday.

Investors are in need of a silver lining as they nurse wounds from the worst selloff seen for Treasuries in more than four decades. The Bloomberg US Treasury Index has dropped since a string of regional bank failures fanned expectations of a credit crunch and recession in early April. The yield on 10-year notes, meantime, has soared to above 5% this week from a 3.25% April low.

Amy Xie Patrick, head of income strategies at Pendal Group in Sydney, said she’s bullish on bonds given their current yields. There’s not much of a case for inflation and economic growth to re-accelerate, indicating “that the ‘soft landing’ is behind us,” she said.

Treasury fixed-rate coupons around 5% also provide investors with the highest source of bond income since 2007, helping the debt to compete against bills and equities. They also make a portfolio more resilient in periods of enduring market pain in risk assets.

Vanguard Asset Management has been a recent buyer of five- to 10-year Treasuries, said Roger Hallam, global head of rates at the firm — with plans to “add more if yields rise further.”

“At these levels of yields your risk/reward is much better,” Hallam said. The belly of the yield curve — bonds maturing between five and 10 years — “will benefit most in the initial stages of any economic weakness.”

A favorable quirk of bond math is that higher-coupon bonds are less sensitive to price changes, a dynamic known as duration. Low-coupon bonds, by contrast, are far more sensitive to prices, and the current bond rout dates from August 2020, when the 10-year yield was a paltry 0.5%. The benchmark yield subsequently increased ten-fold, leaving investors well educated about the adverse impact of duration.

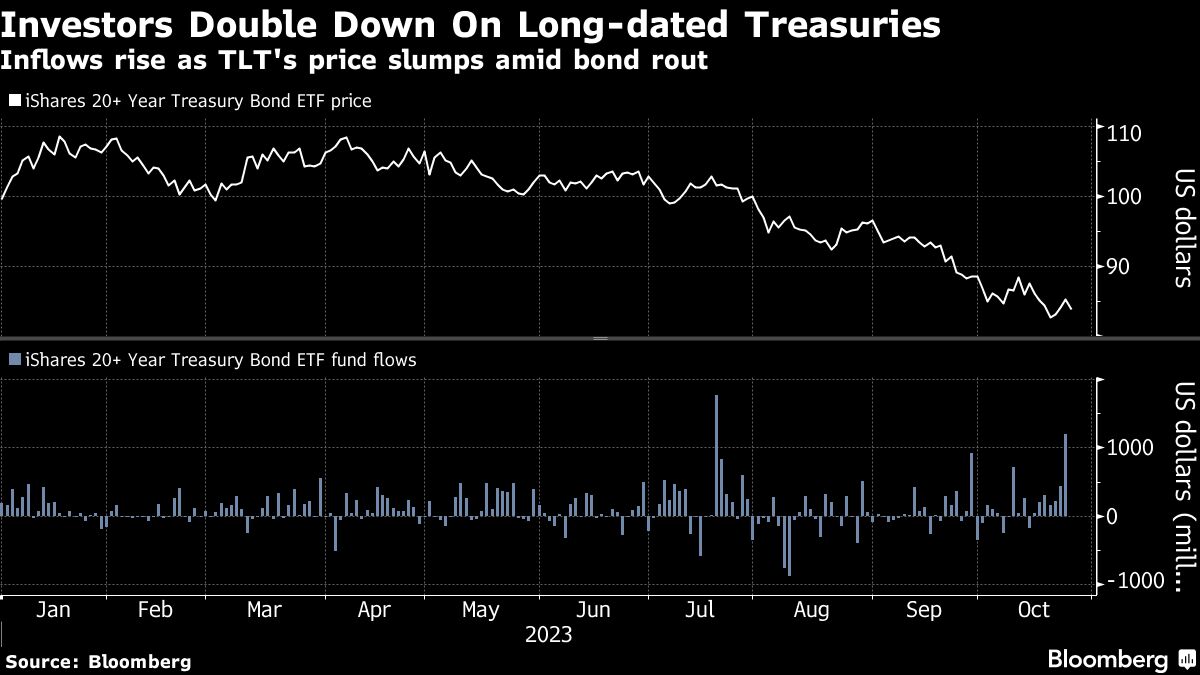

But that risk has been reduced as long-dated coupons settle in the 5% zip code, illustrated by the risk/reward profile of the $40 billion iShares 20+ Year Treasury Bond ETF. While the exchange-traded fund, known by its ticker TLT, has slumped 50% from its 2020 peak, yields above 5% are attracting inflows. At current levels, a long-end yield decline of 0.5% is expected to deliver a double-digit price gain for the TLT, whereas a 50-basis point rise in yields would cause a price drop of only around 1% over a 12-month period.

“If the 30-year rallies a hundred basis points, you’re making 20%,” said T. Rowe’s Bartolini. “And if the five year rallies a hundred basis points, you’re making 4%.”

Bartolini said the firm prefers owning Treasuries with a maturity of five years or less as the Fed signals it’s near the peak of its rate-hiking cycle. Even so, increased Treasury supply could still shove 10- and 30-year yields higher as the market needs “to create an incentive for those bonds to be distributed and the incentive to make that happen is higher yields,” he said.

A renewed push to higher yields beckons over the coming week, with central bank meetings on the calendar for the Fed and the Bank of Japan. Investors will also watch for the latest US monthly employment report, along with a much-anticipated update from the Treasury about its quarterly borrowing needs.

“The normalization of the bond market is what we are seeing right now,” said Anthony Saglimbene, chief market strategist at Ameriprise Financial. The firm is telling financial advisers and clients to start moving their cash into bonds as the Fed wraps up its tightening cycle and inflation ebbs. “The longer rates stay at these levels the greater the refinancing pressure for consumers and small businesses.”

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.