The US economy just enjoyed its strongest quarterly growth outside of the pandemic era since 2014, expanding at a 4.9% annualized rate in the three months ended Sept. 30. The economy’s resilience has continually frustrated the gloom and doomers, who have been predicting an imminent recession for more than a year now.

Still, even the optimists are bound to wonder how much longer a downturn can be avoided at a time of elevated consumer prices, benchmark interest rates at their highest level in a generation and soaring credit-card debt. The answer just might be longer — much longer.

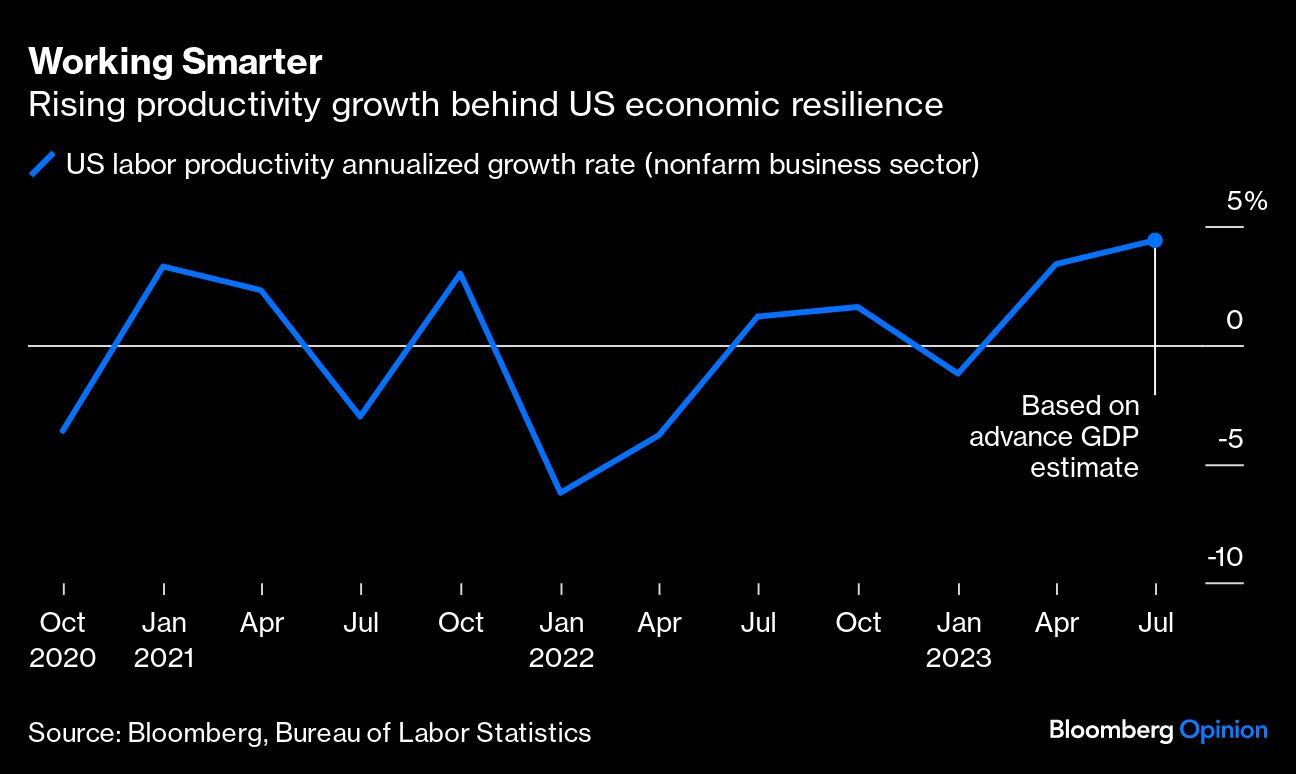

The reason may be due to labor productivity, which grew last quarter by a very rapid 3.7% on an annualized basis. This quarter, it could come in as high as 4.4%, based on the trends in the gross domestic product report. Performance like that would be welcome at any time, but at this moment it’s helping to offset the stiff headwinds facing the economy. (The government said today that overall productivity rose at a 4.7% annualized rate in the third quarter, the highest outside of the pandemic era since the end of 2009.)

Rising labor productivity means the economy can create more stuff with the same number of workers, working the same number of hours. That’s crucial because getting inflation back under control requires either businesses to increase the supply of goods and services or consumers to decrease their demand.

It's always been the case in America that a growing workforce supplied a constant tailwind for increasing supply. But things have gotten harder since the turn of the century, with the labor force participation rate dropping from around 67% to 63%. It has gotten even tougher for employers to find workers in the last few years, forcing many that wanted to substantially expand capacity to offer equally substantial wage increases to attract workers, even those with no experience.

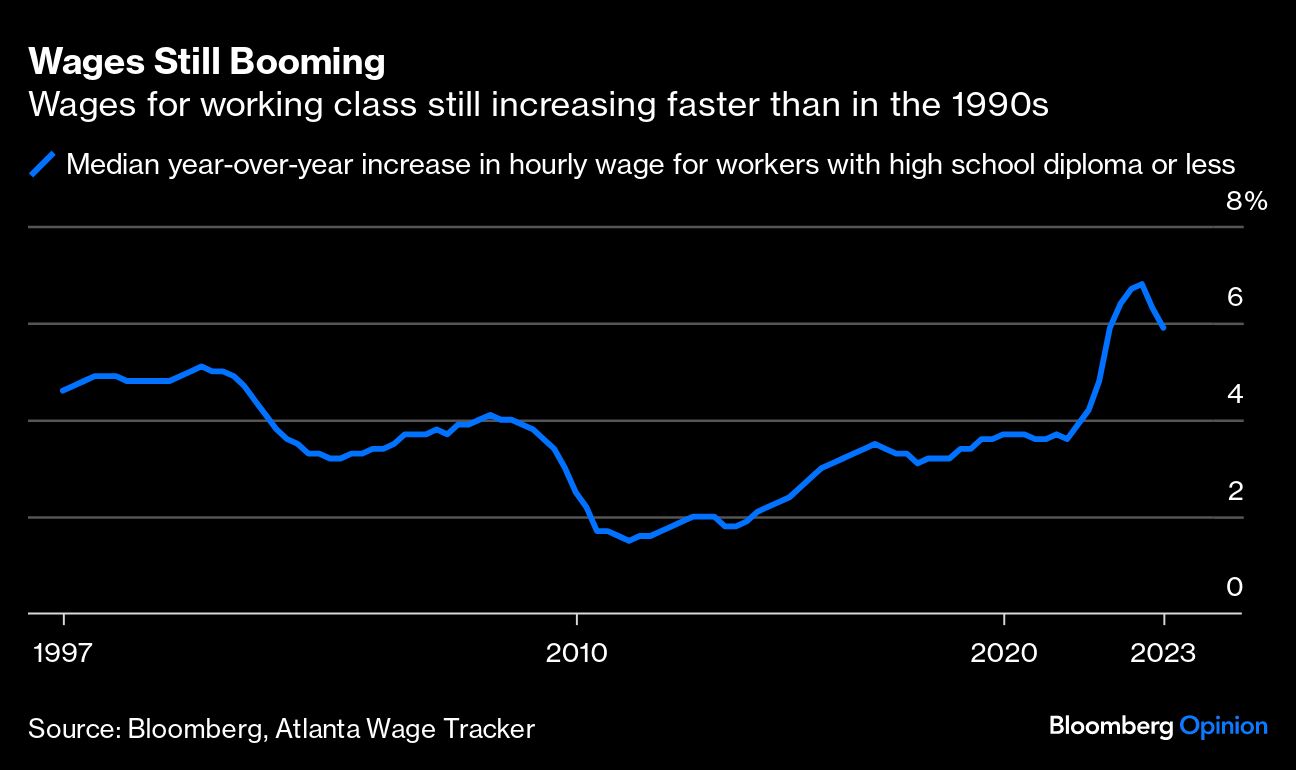

According to the Federal Reserve Bank of Atlanta’s wage tracker indexes, wages for workers with only a high school diploma were increasing at a record 6.8% year-over-year in March. Rapidly rising wages tend to lead to faster inflation because businesses attempt to recoup added labor costs by raising prices and workers spend the extra income. Increasing productivity does just the opposite; it allows companies to keep a lid on prices without cutting wages.

In some industries such as consumer electronics, where rapid productivity growth is the norm, we’ve come to expect prices to fall year-after-year — just compare current prices for big screen TVs to those from 20 years ago -- and for manufacturers to regularly introduce more advanced features that weren’t available for any price just a few years before. That’s the kind of energy the broad economy needs right now, especially the struggling manufacturing sector.

Likewise, interest rates are brutally high because the Federal Reserve was alarmed by the surge in inflation rates in 2021 and 2022 that accompanied a persistently tight labor market. In response, the central bank raised its target for overnight loans between banks more than 5 percentage points between early 2022 and mid-2023.

The Fed has paused its rate increases for now but will only consider dropping them if the rate of inflation continues to fall back toward its 2% goal (it was 3.7% in September as measured by the Consumer Price Index). Inflation rates have come way down, in part, because bottlenecks in global supply chains tied to the pandemic have eased. But inflation will only continue to slow if the economy can continue to find ways to expand supply or — and this is a much worse outcome — if consumer spending collapses and leads to a drop in demand throughout the economy.

It’s that second outcome that most economic observers thought would happen. In their view, the persistently strong consumer spending we’ve seen this year has only prolonged the inevitable. And when spending does finally correct itself, the adjustment will be swift and painful. But strong productivity growth upends that narrative. Each additional quarter of sustained economic growth raises labor productivity higher, expands supply further and brings inflation closer to 2%. No slowdown in consumer spending is needed to temper inflation.

Robust consumer spending is not so much a sign of Americans’ addiction to shopping but of their accurate appraisal of their own future income prospects. The average household has no idea what productivity growth even is, much less able to gauge whether it's relatively strong or weak. Yet, as long as Americans accurately assess the job opportunities that are relevant to them and act accordingly, their behavior should accurately reflect economy-wide gains in productivity. That seems to be what’s happening, and there is no reason why it can’t continue. The real question is how long unfounded pessimism can be sustained.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Karl Smith