Companies with healthy balance sheets are some of the best performing stocks this year, and their shares could keep rising, according to Piper Sandler & Co. strategists led by Michael Kantrowitz.

Investors are shunning zombie companies that survived for years because of low-interest rates. Macroeconomic uncertainty has instead driven US equity investors toward the firms readily able to pay their interest expenses with earnings, known as having high interest-coverage ratios.

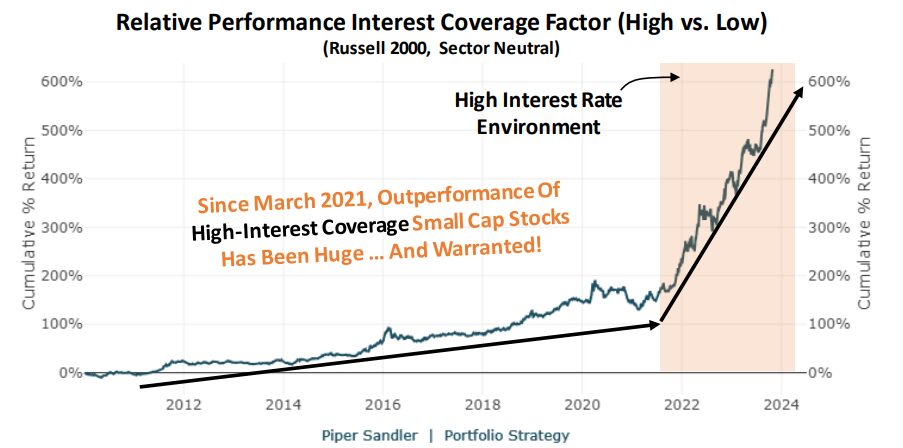

These are the best performing stocks in the Russell 3000 this year, a broad market index, according to Piper Sandler’s analysis of 118 different factors. They found that for interest coverage, the top performing 20% of stocks did the best relative to the bottom 20%.

The Federal Reserve held interest rates at a 22-year high for a second straight meeting on Wednesday, and Chair Jerome Powell reiterated that there’s a long way to go before inflation gets back to target levels, suggesting borrowing costs are likely to stay high for some time. Investors are gravitating toward companies that can bear this expense. The outperformance of companies with high interest coverage ratios is so dramatic it could be viewed as a bubble, but it probably won’t deflate soon, Kantrowitz said.

“We believe this bubble has room to run, and is unlikely to pop until either zombies go bankrupt, or interest rates collapse to much lower levels to keep them alive,” the strategists wrote. “If we’re in an extended period of higher rates for years, this could be the factor of the decade.”

Source: Piper Sandler

For companies in the Russell 2000 Index, the difference between the top 20% and the bottom tier was even greater, signaling that smaller companies with weaker balance sheets get punished even more than their larger counterparts. Interest coverage ratios for many of these companies could well deteriorate in the future, according to the strategists.

Overall, the Russell 2000 has fallen about 5.6% this year through Tuesday’s close, on track for a second straight year of declines. The companies most likely to default in the next 12 months have performed even worse, plummeting 26%, according to Bloomberg’s Issuer Default Risk model. Many are in industries like biopharma and energy.

These divisions in performance can help investors that are actively picking stocks. They can sift through companies and pick winners and losers, instead of being in a market where everything rises in lockstep. Steven DeSanctis, equity strategist at Jefferies LLC, likened the environment to the burst of the tech bubble at the turn of the millennium.

“We can be in the ‘Golden Age of Active Management’ across small caps as the indexes have become ‘lower quality’ thanks to an increase in nonearners and no-sales companies,” Desanctis wrote in a note to clients on Monday. “We think active managers can continue their success.”

Bank of America Corp. has also advised clients to seek out firms that generate good cash flow even if they have relatively low growth expectations, and stray away from “infinite duration” non-earners, or those that may take a long time to be profitable, as there is less certainty about their future success when it’s so expensive to borrow to fund their investments.

Many large companies with weaker balance sheets are shrinking. Since 2021, 50% more big companies have become small compared with those that grew into large corporations, according to Bank of America’s head of equity and quantitative strategy, Savita Subramanian. That’s an unusual reversal from prior decades, where more companies usually get bigger.

This suggests a “purge of weaklings,” leaving the S&P 500 Index in relatively good shape, according to Subramanian. For the Russell 2000, a record proportion of companies are losing money, she wrote.

Rising interest rates have hurt companies in at least two ways. It’s more expensive for them to borrow, and monetary tightening tends to weigh on profit growth.

“Higher rates can morph zombies from walking dead to actually dead,” said Steve Sosnick, chief strategist at Interactive Brokers. “If they offer lots of promise but little cash flow, and they need to refinance their debts in an environment when credit is scarce, that can make it impossible to stay in business.”

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Alexandra Semenova, Elena Popina