One consistent overhang in an otherwise pretty good year for the US economy has been tightening credit standards at banks.

Lower loan growth has meant more expensive or in some cases non-existent credit availability for people looking to purchase things like cars, or for small and midsize businesses.

It’s noteworthy then that banks provided some clarity on when they expect to loosen the purse strings during their recent earnings conference calls. In many cases, it’s as soon as the next couple of quarters.

This doesn’t mean the problems that surfaced in March, leading to the failure of four lenders, are entirely resolved. It implies instead that a number of banks feel confident enough of their capital position that the headwind the sector posed for growth is likely to start receding in the near future — a constructive turn since other drivers of economic activity appear to be cooling.

Bank credit has been tight this year because large and midsize lenders — those with assets above $100 billion — have been building up capital buffers in anticipation of sweeping regulatory changes to the way they account for, and protect against, the risks associated with their business. Most banks now have enough of a cushion — so-called excess common equity tier 1 capital, or CET1 — to meet the tougher requirements, which will be phased in from 2025.

Apart from the regulatory uncertainty, losses on government bond holdings also made lenders cautious, especially once an erosion of confidence among depositors helped bring down Silicon Valley Bank and Signature Bank.

To see the numbers and rationale behind banks building up their capital buffers, consider the PNC Financial Services Group, the sixth-largest bank by domestic assets in the US as of June 30. It increased its CET1 capital ratio from 9.1% to 9.8% in the first three quarters of 2023. Its regulatory minimum as of Oct. 1 was 7%, leaving a significant buffer.

Yet, as the bank explained in an investor presentation, if new regulations force it to hold capital against the unrealized losses on investment securities — the kinds of losses that contributed to the demise of Silicon Valley Bank — as well as other possible changes under what’s known as Basel III Endgame — PNC’s excess CET1 ratio would shrink to 40 basis points.

While every bank finds itself in a different place, this general dynamic — building capital every quarter this year, comparing capital levels with current and potential future requirements, and taking into account economic and regulatory uncertainty — has made banks cautious on lending and other activities such as share buybacks.

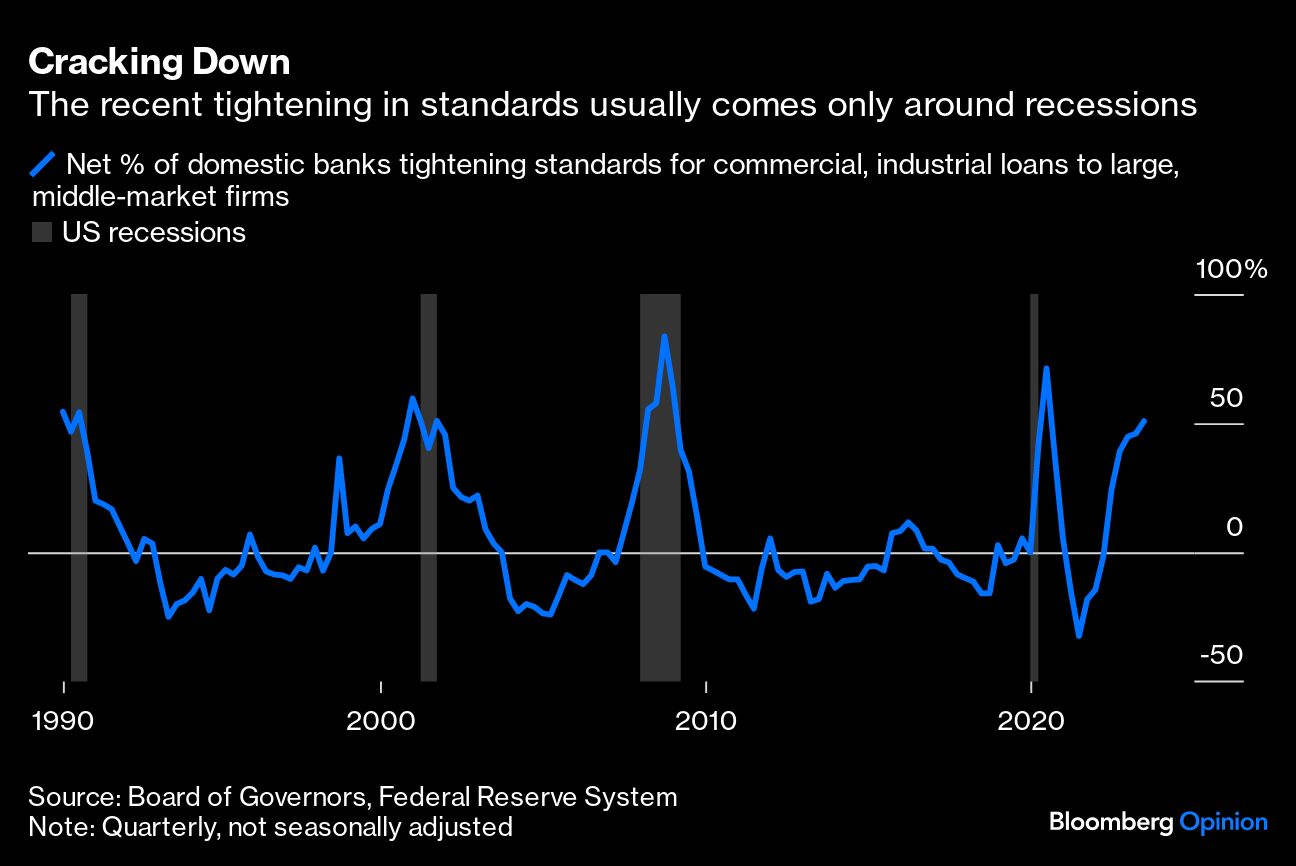

It’s why the Federal Reserve’s quarterly survey of loan officers shows banks tightening standards for lending at a scale that typically only happens in the middle of recessions. And while there won’t be a single moment when markets, bank executives or regulators give the “all clear” for lenders to increase their risk-taking activities, the pullback should begin to abate over coming quarters.

For example, Regions Financial Corp. has been building its CET1 ratio at a rate of 0.2%-0.3% per quarter, and exceeded its 10% target by 30 basis points in the third quarter. So, executives now feel like they are in a position to use the excess capital on share buybacks or lending as opportunities arise, Chief Financial Officer David Turner said on an earnings call.

Other banks have different thresholds for shifting out of capital-build mode, but even that’s likely measured in months.

U.S. Bancorp’s CEO Andy Cecere said he would continue to bolster the bank’s cushion until the Basel III rules are finalized and next June’s Federal Reserve stress tests, which evaluate whether lenders are able to weather economic storms. Comerica Inc. CFO Jim Herzog said that in addition to regulatory clarity, he wants to see the unrealized losses on the bank’s securities stabilize — in other words, see longer-term interest rates stabilize.

With longer-term rates falling meaningfully this week and investors more confident that we’ve reached the end of a cycle of interest rates increases, such unrealized losses have shrunk for banks, boosting capital levels and perhaps leading executives to feel more confident that the worst is behind them.

A rapid deterioration in the economic environment would obviously lead to a different discussion. Barring that, the likely path for banks is a natural increase in CET1 capital ratios of 0.2%-0.3% per quarter in most cases, regulatory clarity on capital requirements, and a growing confidence that they can put excess capital to work to assuage anxious investors.

This could take the form of lending if demand and underwriting make sense, and share repurchases if there’s money left over. Banks should be in a better position to make loans in 2024 than they were in 2023, reducing one of the biggest economic concerns that people have had this year.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Conor Sen