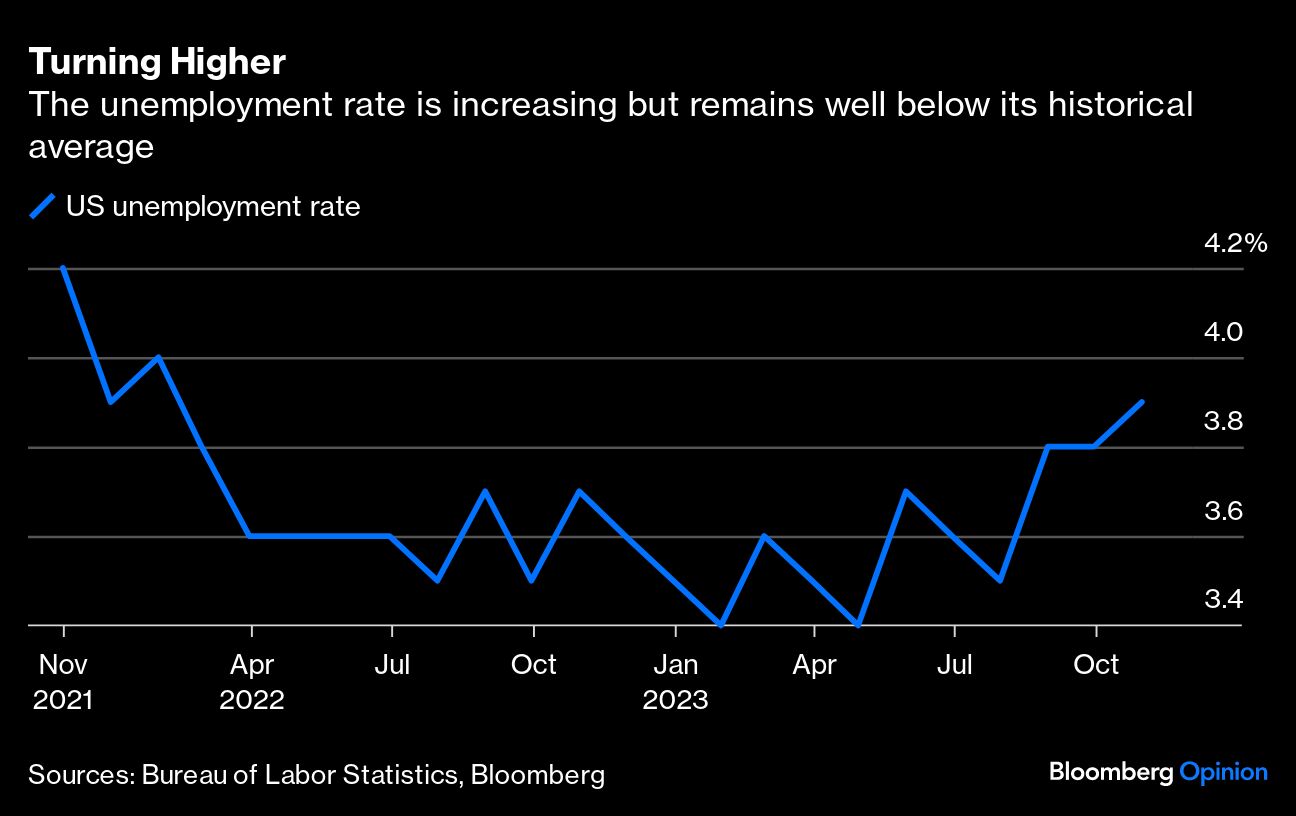

Alarm bells sounded Friday when we learned that the US unemployment rate rose to 3.9% for October, well above the 50-year low of 3.4% that it hit earlier in the year. The latest reading is still very low, so what’s with the doomsayers telling us a recession has arrived?

Relatively small increases in the unemployment rate, even starting from low levels, typically signal a recession. Where we are now is insufficient to make that call, but it’s worrisome. How do I know? Before the pandemic, I developed a highly accurate recession indicator, later named the Sahm rule. It would have triggered early in every recession since 1970. But it has not triggered now.

The Sahm rule is simple. If the three-month average of the unemployment rate (the monthly rate often bounces around too much) is half a percentage point or more above its low in the prior 12 months, the economy is in a recession. The current value is 0.33 percentage point, so it’s highly unlikely that we are in a recession - at least for now.

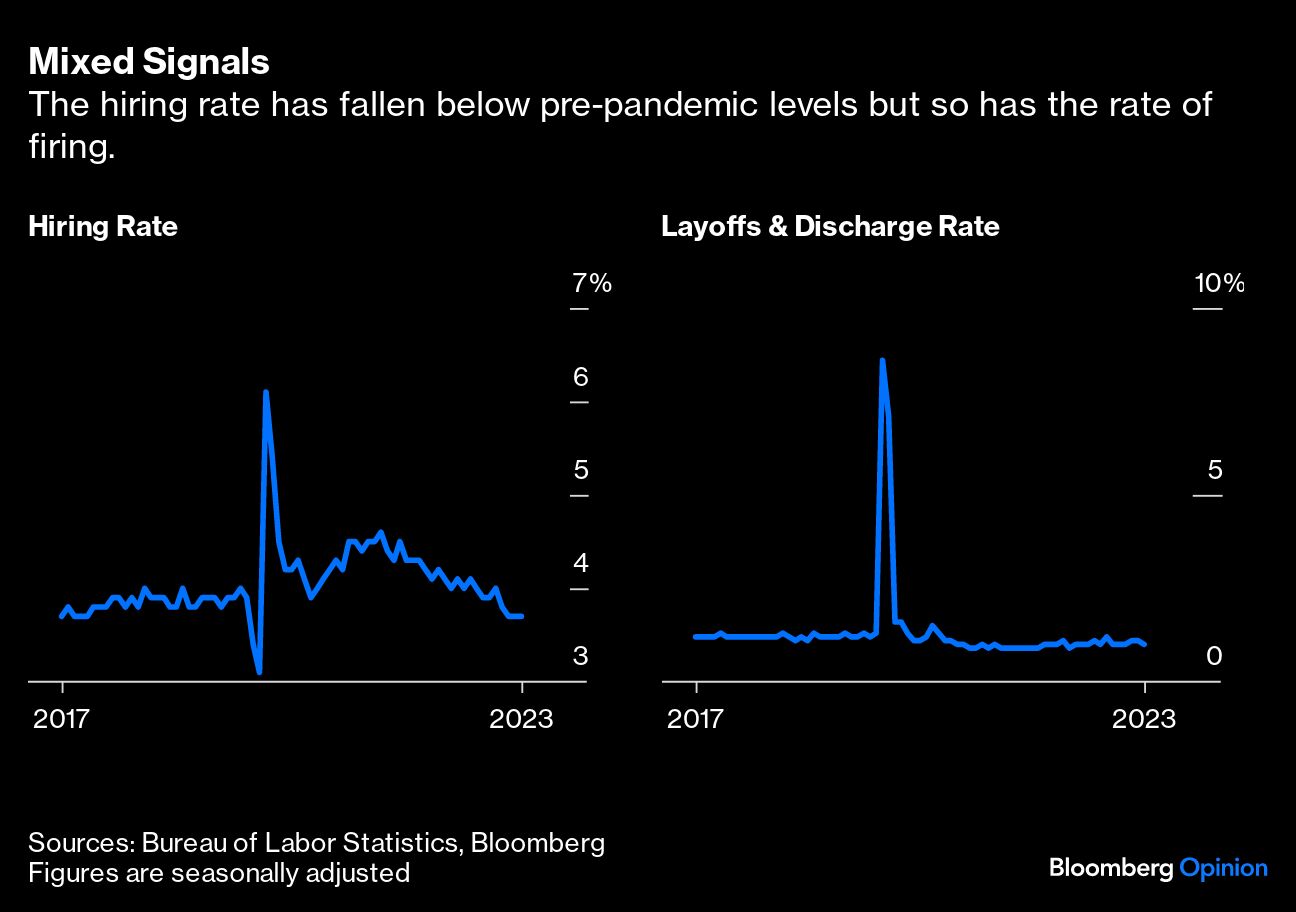

Even so, the unemployment rate has risen, threatening to trigger a negative feedback loop of further unemployment that leads to a recession. When workers lose paychecks, they cut back on spending, and as businesses lose customers, they need fewer workers, and so on. Currently, the signals are mixed: the hiring rate has fallen below pre-pandemic levels, while the firing rate remains low. And growth in consumer spending, even after accounting for inflation, has been strong this year.

Yet, it’s a risk that now warrants watching closely. Once the feedback loop starts, it is usually self-reinforcing and accelerates. Even in the mildest recessions, such as in 2001, the unemployment rate rises two percentage points from the pre-recession low, and typically it's almost four percentage points. Today, that would imply an unemployment rate exceeding 5% and at least three million more people without jobs. And a recession affects more than the unemployed: smaller wage gains, less career advancement, and reduced worker bargaining power—a sharp contrast from the current recovery.

But again, a recession is not inevitable. Indicators of economic downturns like the Sahm rule are empirical regularities from the past, not laws of nature. The pandemic was extremely disruptive, and the rebalancing of the economy has been messy and slow. That’s as true for inflation and supply chains as it is for the labor market.

The unemployment rate shot up to almost 15% within two months in the spring of 2020 and then plummeted to 3.4% only three years later. Recall that it took a decade from the start of the Great Recession in 2008 for unemployment to reach such lows. The story in the jobs market since the start of the pandemic is complex, with the supply and demand for labor moving sharply and often at different speeds.

After more than two years of severe labor shortages, workers are still coming back at a somewhat faster pace than new jobs being created. The labor force participation of prime-age women is at an all-time high after an outsized decline in 2020 in what was dubbed a “she-cession.” Workers with disabilities and Black men made historic gains this year, too. After a stoppage during the pandemic, immigrants on work visas are entering the country. Taken together, economist Julia Coronado, the president and founder of MacroPolicy Perspectives, argues that the rising supply of workers is good for the rebalancing of the labor market, even if it shows up initially in somewhat higher unemployment rates.

If that’s the case, recession indicators based on the unemployment rate, like the Sahm rule, may not be as accurate this time. On the path back to normal, unemployment may move above 4% for some time, which would trigger the rule but not a recession as jobs catch up to supply. The Sahm rule would not be the first recession indicator to “break” in this cycle. Last year, real gross domestic product declined for two consecutive quarters without the National Bureau of Economic Research declaring a recession — something that hadn’t occurred in the US since 1947. The declines were driven by a sharp drop in net exports and large swings in inventories – both of which are consistent with resolving disruptions in global supply chains.

To be sure, if the recent rise in unemployment continues, this time could be different in less sanguine ways. Typically, Congress — regardless of the party in power — enhances jobless benefits and other social safety nets in a recession. In fact, the reason I created the Sahm rule was to give lawmakers a tool that could tell them when to trigger those programs automatically. But such relief would be unlikely now with elevated rates of inflation, tensions over the federal budget deficit, and partisan rancor.

With the federal funds rate over 5%, the Federal Reserve has ample room to ease monetary policy, as it would in a recession. But it’s part of the orthodoxy that cutting rates at the first signs of a recession in the 1970s when high inflation was a mistake and actually fueled inflation. It’s unclear whether today’s Fed, hyper-focused on taming inflation, would do anything to soften the blow of a recession.

The question is not whether we can call a recession if it were to come; it’s what policymakers do next that will determine how much hardship it causes.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Claudia Sahm