The inflation scare is barely behind us, and it is already time for the Federal Reserve to focus on recession risks. The recent trajectory of job growth means policymakers can no longer rule out unemployment snowballing in 2024, which should force a shift in how they think about managing their dual mandate.

Lowering the Fed Funds rate by 50-75 basis points over the next few quarters would reduce the risk of more drastic interest rate cuts in a recession — and may even stave off recession.

Last week marked a turning point for the balance of risks to the economy — for now at least. The unemployment rate at 3.9% in October is slightly above the Fed’s end-2023 forecast of 3.8%. More significantly, it has risen 50 basis points since April, an exceptional move for a healthy economy. By this point in 2001, 2007 and 2020, the US economy was entering recession.

As much as one can make the case that everything is fine, and that the rise in unemployment is influenced by unusual factors — the way so much has been in recent years — policymakers can’t shrug off a trend like this, and I suspect they won’t.

The ‘everything is fine’ camp would argue that the rise in the unemployment rate isn’t a concern because it’s been coupled with an increase in both productivity and the size of the labor force.

Productivity growth was a scorching 4.7% in the third quarter we learned last week, following a robust 3.6% improvement in the prior three months. The economy has produced more output without needing a surge in employment, which has boosted gross domestic product growth while unemployment has risen modestly.

At the same time, the labor force has grown by 3.1 million people over the last year due to participation rising faster than overall population growth. This is likely due in part to the strength of the job market — people tend not to come off the sidelines unless there’s a perception that they will find work.

But more recently, this labor force growth has not turned into employment growth — over the past six months, more than one million people have joined the workforce, of which just 191,000 have found employment while 849,000 are unemployed.

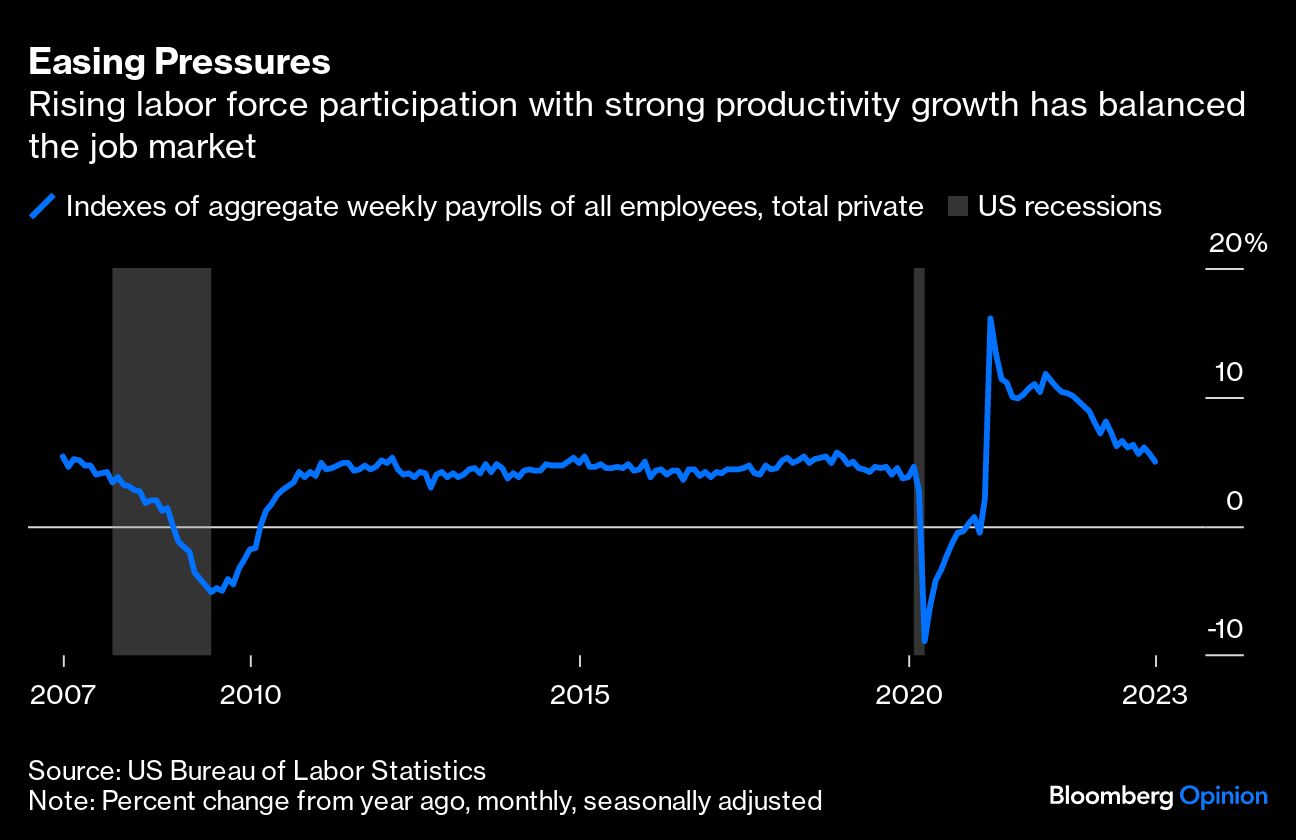

However one wants to frame it, rising labor force participation coinciding with strong productivity growth rebalanced the job market. Aggregate weekly payroll growth — a measure that incorporates jobs, hours worked and wages to offer a useful proxy for the growth in worker incomes — grew 5% year-over-year in October, in line with the general trend we saw in the 2010s when inflation was less of a concern.

If you’re a Fed policymaker, you now have reason to believe that the labor market has rebalanced, which should reduce your concern about a wage-price spiral fueling inflation in the medium-term. At the same time, because the unemployment rate has risen and is above your year-end target, you can’t rule out a continued worsening in 2024. Downside risks to employment now outweigh upside risks to inflation.

In the name of both economic and financial market stability, the right course of action is to signal a few interest-rate cuts in 2024. Lowering interest rates by 50-75 basis point — the kind of insurance cuts the Fed employed in 2019 — would reduce the risk of having to cut by 2-3 percentage points in a recession brought on by too-tight financial conditions.

With both the labor market and inflation heading into 2024 softer than they were a year ago, this would simply be calibrating monetary policy to reflect the current environment rather than the rapid rate-cut cycles we’ve become accustomed to in downturns over the past 25 years.

A modest easing would also help un-invert the yield curve, relieving some stress in the financial system where institutions that borrow short-term funds to lend over longer horizons have felt margin pressure.

There’s a good chance that by doing this, the Fed wouldn’t have to cut interest rates any further in 2024 — a hawkish outcome compared with the current market expectation for slightly more than 100 basis points of reductions next year.

There are reasons to think that the recent rise in the unemployment rate is just one more way in which the economy is normalizing following the Covid-19 disruptions. The sharp rally in bank and housing-related stocks last week signaled that, for now, markets don’t think the economy is headed into a recession.

But without a stabilization or reversal in the unemployment rate, which wouldn’t show up in the economic data for at least a few months, the Fed should be more focused on the risks to employment rather than inflation. There’s no need to cut rates yet, but it’s time to signal a shift in approach just in case.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Conor Sen