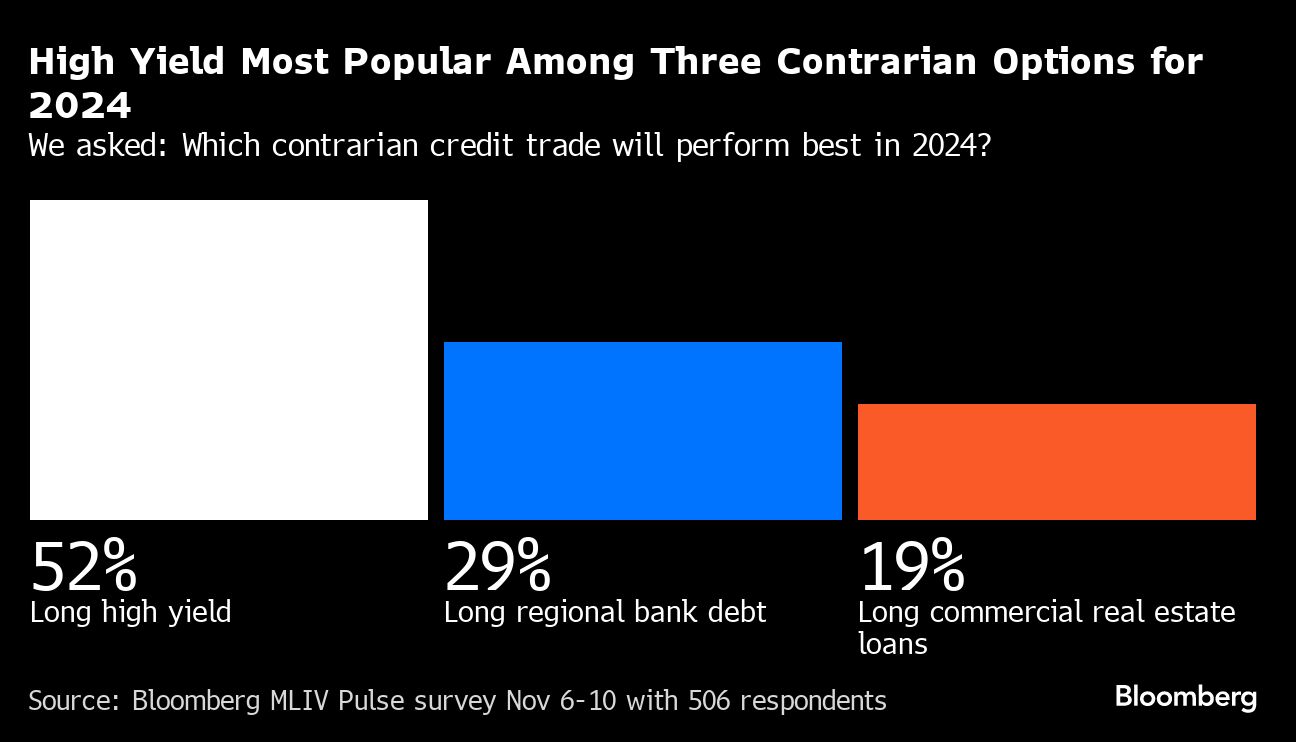

Worries about an economic downturn aren’t enough to dissuade market participants from being bullish on risky debt as their top contrarian trade, according to the latest Bloomberg Markets Live Pulse survey.

Despite heavy outflows in 2023 and countless warnings about the health of heavily indebted companies, 52% of 506 respondents see opportunities in high-yield bonds, while remaining more cautious on some of this year’s laggards including regional bank debt and commercial real estate loans.

The results are a sign of trust in the balance sheets of corporate America, even as the Federal Reserve looks to squeeze growth to rein in inflation. Technical catalysts may be another reason otherwise cautious investors still see opportunities in junk bonds. The global high-yield market has shrunk more than 20% since its 2021 peak to $1.94 trillion, according to Bloomberg data. Less supply has already helped fuel a gain of more than 6% in the asset class this year.

“There’s actually been outflows for high yield, but the universe has shrunk more at the same time,” said Matt Brill, head of North America investment-grade credit at Invesco Ltd. “If you can get inflows — which should happen as the Fed pauses and yields stabilize — combined with a shrinking universe, it’s a very good combination.”

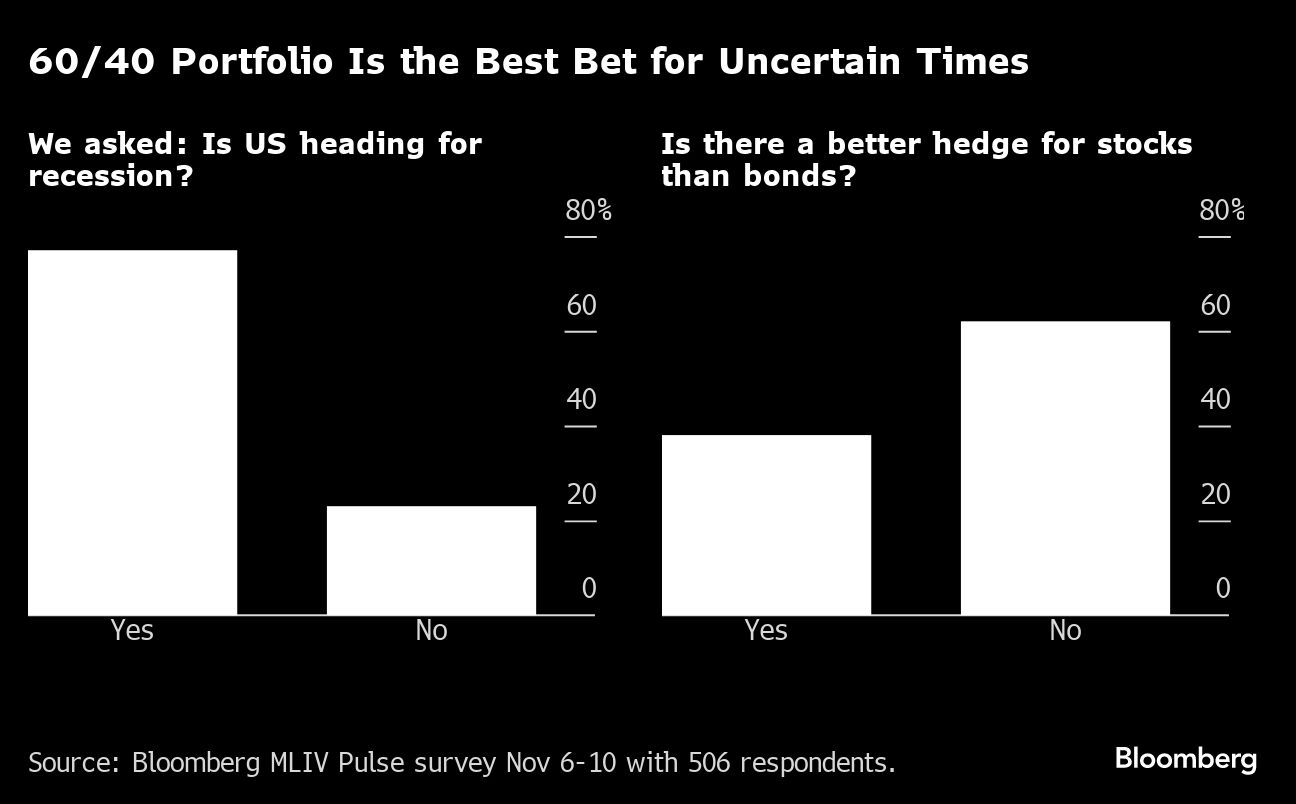

More than three quarters of survey respondents still expect the US to slip into recession, and a majority say buying bonds remains the best way to counter stock volatility.

That’s a vote of confidence in the balanced portfolio strategy that’s come under fire in the inflationary era as bonds failed to hedge the equity downturn.

As far as inflation is concerned, responders pointed to employment and CPI data among the most overhyped by investors this year.

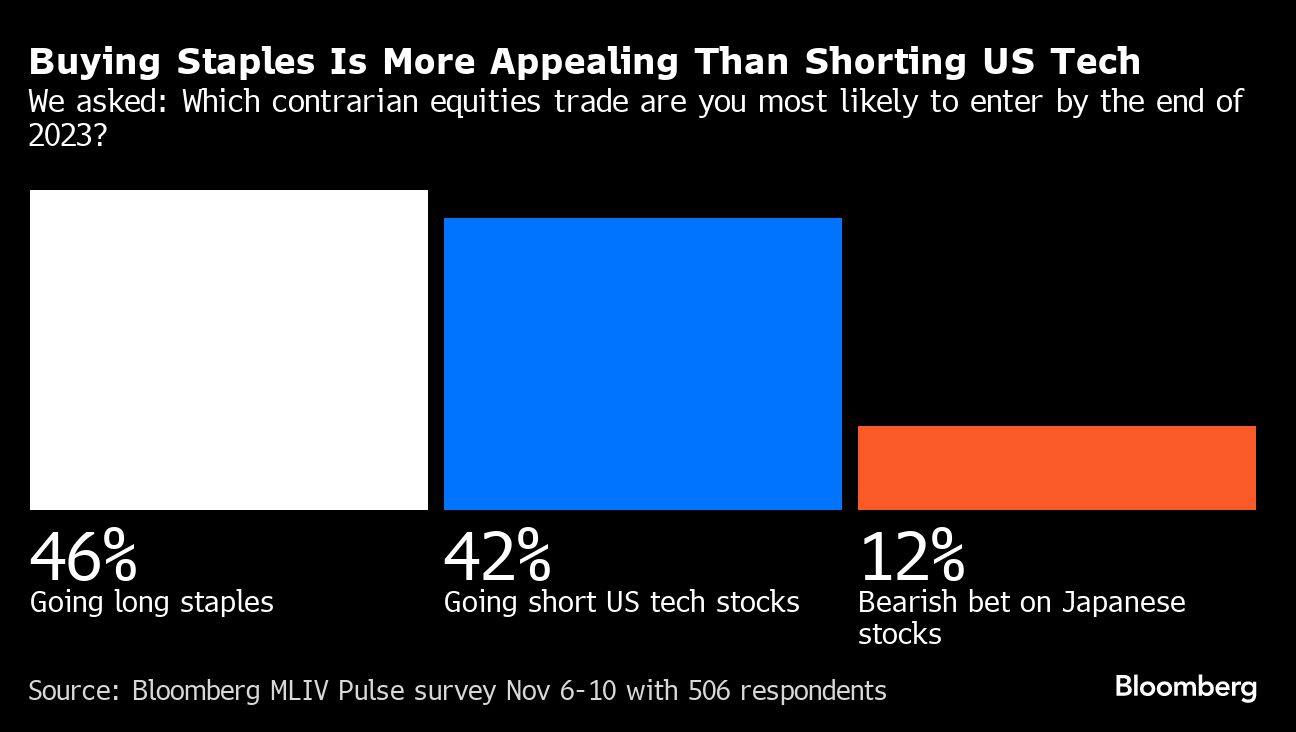

Going long staples such as Walmart Inc. or Costco Wholesale Corp, a relatively secure strategy, was the most popular contrarian stock trade. It came ahead of bearish bets on US tech stocks and Japanese shares. Both Nasdaq 100 and Nikkei generated double-digit gains so far this year.

“Investors were very defensively positioned heading into this year expecting a recession,” said Nelson Jantzen, an analyst at JPMorgan Chase & Co. “The resilience of the economy and earnings have been a positive surprise and in support of valuations.”

Big reversals in risk assets last year were closely correlated with changes in investors positioning — gains came after investors sharply reduced risky bets and declines occurred after buying sprees. While money managers fretted over an almost certain recession in 2023, a resilient global economy and robust corporate profits have shielded speculative-grade debt investors.

Junk bond exchange-traded funds have been seeing an influx of cash since the last Fed meeting, amid signals from Chair Jerome Powell and other officials that the hiking cycle may be at its end. High-yield funds have seen cash inflows of $7 billion in November, reversing months of heavy outflows.

Recessions have historically caused corporate spreads to widen, but bulls remain confident amid strong earnings. Additionally, some are betting that even if an economic contraction materializes, it will be a shallow one that doesn’t lead to a big spike in defaults.

That’s the case for Geof Marshall, portfolio manager at CI Global Asset Management in Toronto. He says junk-rated credits are in solid shape financially and loaded with less leverage, making them better prepared to weather a potential downturn.

“We’re getting a big flashing green light on yield and price in the high-yield market,” said Marshall. “Defaults in the next downturn might peak at 4%. The numbers suggest that the US will go through a shorter and shallower recession, and we’re coming into it with better quality now in the high-yield bond market than ever.”

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our full schedule of upcoming CE-approved virtual events.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

More Exchange-Traded Products Topics >