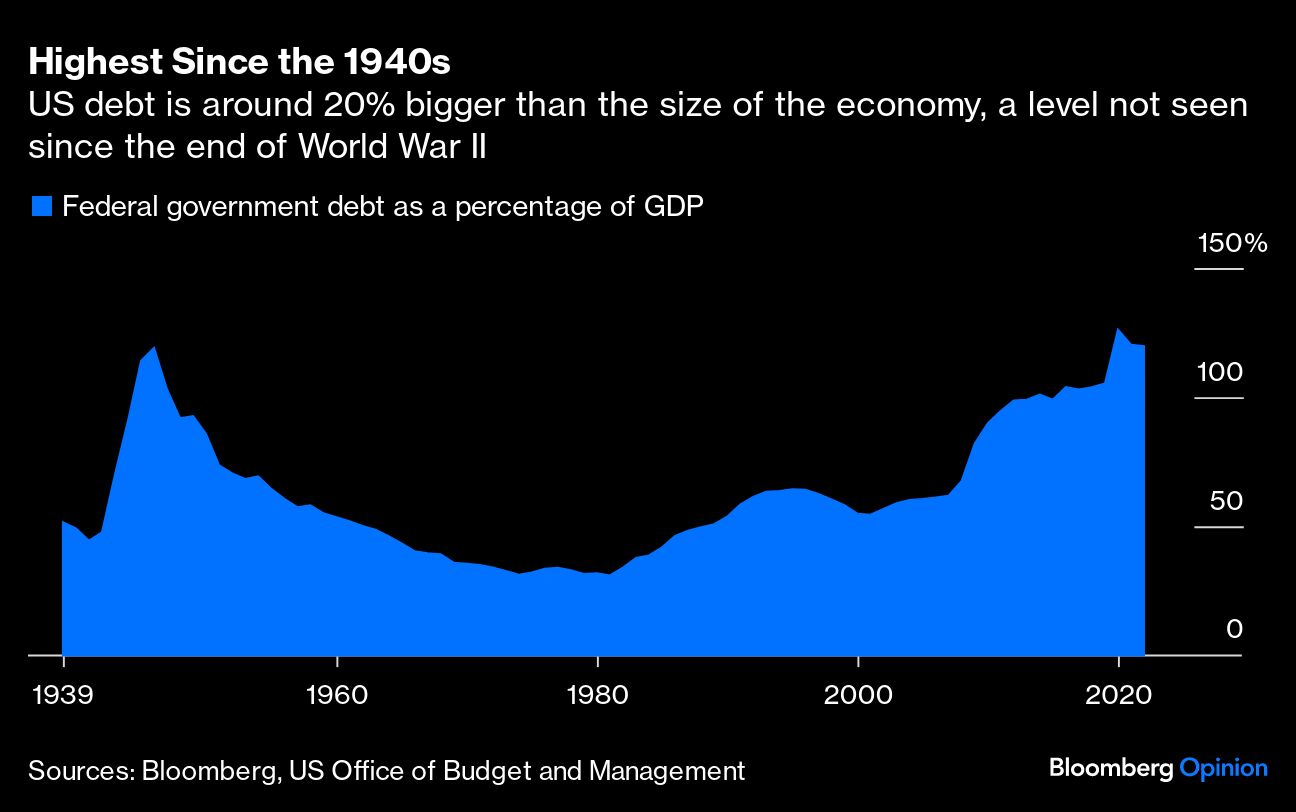

With its $33.7 trillion of debt and trillion-dollar budget deficit, the US’s deteriorating fiscal situation is impossible to ignore. To simply balance the budget, a 29% across-the-board cut in spending would be necessary, even if the tax cuts enacted by Trump administration are allowed to expire at the end of 2025.

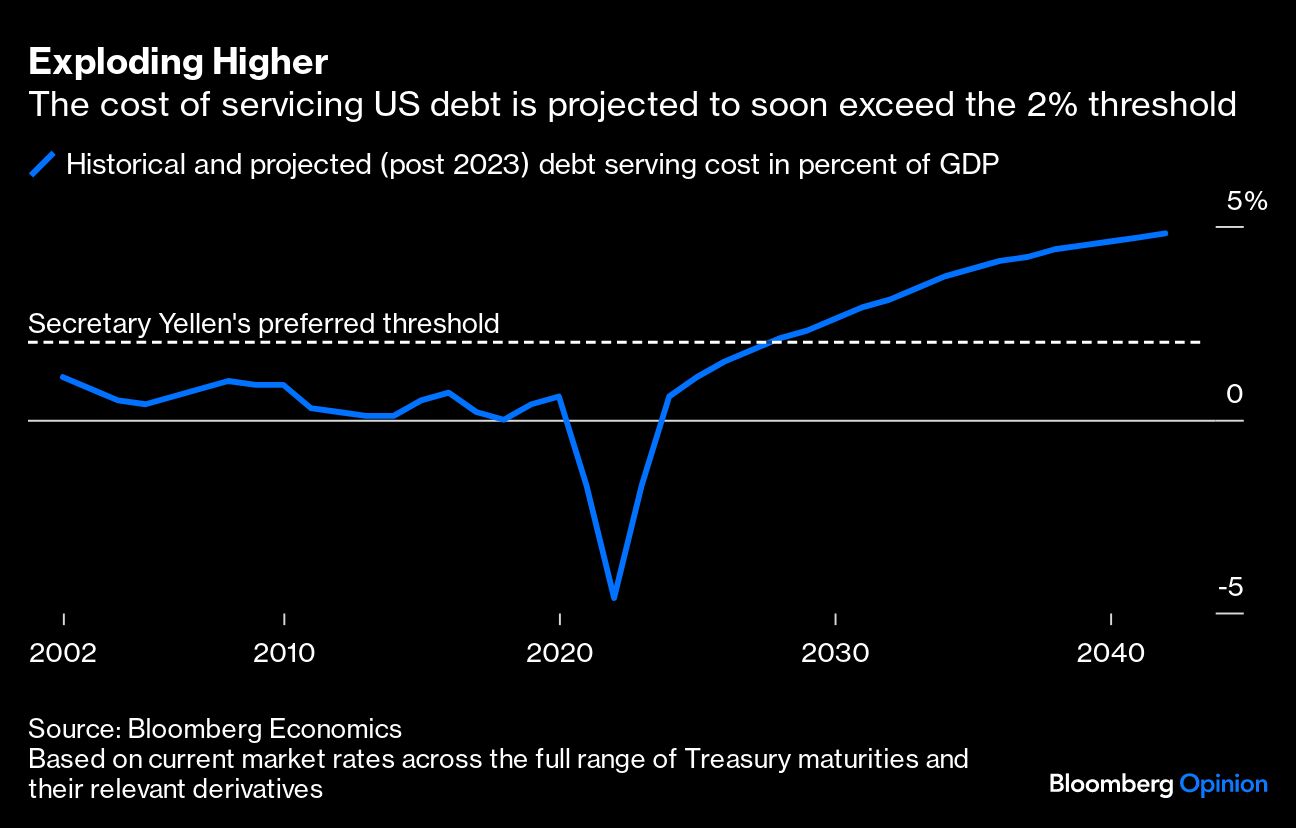

Rising interest rates have made the situation even worse. Analysis by Bloomberg Economics’ Maeva Cousin and David Wilcox shows that what appeared to be a sustainable debt situation just a few years ago has become thoroughly unsustainable. No wonder Fitch Ratings joined S&P Global Ratings in stripping the US of its AAA credit rating, and Moody’s Investors Service warned last week it may do the same.

But while everyone is focused on the spending side of the equation, perhaps the way out of this debt quagmire is on the economic side. In that sense, the years immediately following World War II offer some valuable lessons. Like now, America’s ratio of debt to gross domestic product stood at around 120%. But by 1951, it had dropped to a more comfortable 73%. The decline came not through massive spending cuts and forced debt reduction but rather with policies that fostered stronger and faster economic growth averaging 4.1% from 1947 to 1957.

In many ways, the economy today is in a better position to achieve above-trend growth than it was some 80 years ago. A quick back-of-the envelope calculation suggests that — all else being equal — the economy would need to grow at a sustained pace of 4.25% to get America’s debt-to-GDP ratio down to 97% over the next 10 years. That kind of growth may seem like a stretch, especially given the very sluggish recovery that followed the financial crisis, but it’s not out of the question even with the Congressional Budget Office forecasting 2.4% baseline growth per year over the next decade. How? For one, achieving the required performance would mostly require Washington to get out of the economy’s way. But more specifically, at least three areas have potential for massive growth.

The first is artificial intelligence, which consulting firm McKinsey estimates could add 0.6 percentage points to GDP annually. A Harvard Business School study randomly asked management consultants to either integrate OpenAI’s GPT4 into their workflow or continue with standard procedures. The group that integrated GPT4 finished 12% more tasks than the control group and finished them 25% faster. What makes this remarkable is that the consultants were given no guidance or instruction on how to use the AI, they were simply told to use it. Imagine what could have been accomplished if they were experts in AI.

Creative and open engagement with AI is key to maximizing its potential and economic productivity. The Biden administration, though, has already put in place sweeping executive orders that seek to regulate AI, not just for safety and national security reasons, but also to “advance civil rights, civil liberties, equity, and justice for all.” As noble as these goals sound, it’s impossible at this point to foresee all the implications — positive and negative — that AI will have on achieving such ideals. Just as during the nascent growth of Silicon Valley, a largely hands-off approach to the non-security dimensions of AI will allow it to fulfill its economic potential.

The energy sector is another area where excessive regulations threaten to restrain growth. Although transitioning to a clean energy future will require massive investment in new infrastructure, such investments have been stymied by an inordinate amount of permitting.

Sure, part of the deal to raise the debt ceiling that President Biden reached with House Republicans this year loosened some restrictions, but it failed to address the major issue of energy transmission through new powerlines and pipelines. Without an updated grid, the US will be unable to maximize the usage of all the clean energy resources coming online. Likewise, without the ability to supplement clean energy with natural gas, communities won’t be able to abandon coal. Full permitting reform for energy transmission can unlock this capability.

It’s hard to get an objective estimate of what all this might mean for growth, but just consider that the energy sector is a huge part of the economy, and small reforms can have an outsize impact. The Federal Reserve Bank of Dallas estimated that in its peak in the years 2010 to 2015, the shale boom added 0.2 percentage points to GDP growth annually.

The third area is the most powerful source of potential growth but also the most politically charged. There’s no question that America needs more workers. The issue is that the most obvious way of expanding the workforce doing so is by increasing the pool of skilled immigrants, and Americans have soured on increasing immigration. The reason seems related to the situation at the southern border, which 72% of Americans rate as either a major problem or a crisis.

At the same time, 68% believe immigration is a good thing for the country. So, by focusing policy on increasing the number of high-skilled immigrants no matter where they come from, the federal government could expand the workforce without ignoring popular concerns about immigration overall. Moody’s has estimated that every 1% increase in the population through immigration adds 1.15 percentage points to gross domestic product.

Add the benefits from AI, a new energy boom and immigration to the CBO’s baseline estimate and you get GDP growing at a 4.25% annual rate. Sure, this is all very simplistic, and tax increases and spending cuts will have to be part of any solution, but the big idea is that America’s historically high level of debt can be lowered over time in a practical manner without going down the route of painful financial austerity. At the same time, this growth cannot be conjured up with the whisk of a magic wand; it needs help from the government.

As daunting as the fiscal situation appears, the path forward is clear. America has done it before, and we can do it again.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Karl Smith