Professional traders entered November wagering Jerome Powell’s campaign to tame inflation was a long way from being won. Now they’re being forced into risky bets that the battle is over.

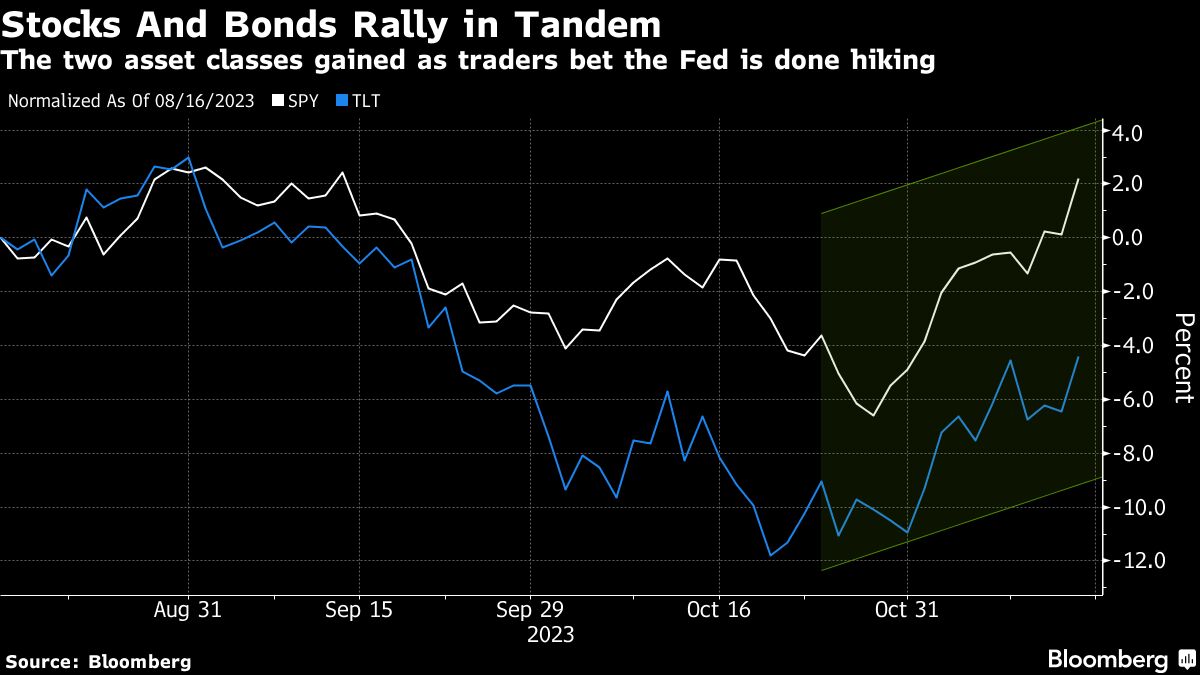

First, it was the Federal Reserve chair’s dovish turn on Nov. 1, when Powell conceded predictions for future interest-rate hikes weren’t written in stone. Then, an unexpected cooling in consumer-price increases Tuesday added fuel to the biggest three-week rally this year, judging by cumulative gains in a pair of popular ETFs tracking US stocks and long-dated Treasuries.

In one example of investor capitulation: Fast-money quants have snapped up around $100 billion of global equities and bonds combined over the past week and may need to keep buying, according to data by Goldman Sachs Group Inc.

While the speed of inflation’s drop was a recipe for pain among bearish pros, their tentative shift toward a more bullish posture sits uneasily in an economy that has shown itself capable of what Powell has termed data “head fakes.”

Still, conviction that the Fed’s hawkish turn is over sparked a big bond rally Tuesday with five-year yields plunging more than 20 basis points to around 4.4%. Yet equity investors are embracing signs of economic cooling — an outcome that would put this year’s 17% gain in the S&P 500 on a shaky footing.

“Shifting narratives are swinging financial markets from opposite extremes that greatly overshoot the actual changes in fundamentals,” said Dan Suzuki, deputy chief investment officer at Richard Bernstein Advisors. “It probably makes sense to fade the extremes unless there’s a meaningful shift.”

The S&P 500 jumped 1.9% Tuesday for its best day since April, while an exchange-traded fund tracking long-dated Treasuries surged more than 2%. Data showed consumer prices rose at a slower-than-expected pace, marking a milestone for the central bank’s fight against inflation.

Speculation the release sets the stage for a soft landing may be the basis for the gains, but the unwinding of bearish positions is adding fuel. As of October, active equity managers were defensively positioned, while net short bets on Treasuries held by professional speculators hovered close to the highest level on record, Commodity Futures Trading Commission data showed.

“November has seen one of the largest equity and bond demand that I can ever recall,” said Scott Rubner, a managing director at Goldman, who has studied the flow of funds for two decades. “We model further demand from systematic, corporate, and discretionary hedge funds until the end of the month. Today is a significant change in tone and shift in sentiment is now in favor of a year-end rally.”

Commodity trading advisers — which take long and short positions in the futures market — were sitting on a record-short bond bet and may snap up around $91 billion over the next week, if this month’s advance continues, per Goldman. The cohort also has the capacity to add as much as $430 billion if the moves extend over the next month. Meanwhile, CTAs could be buyers of an additional $100 billion of global stocks over the next week and $212 billion over the next month if the upside momentum holds, says Goldman.

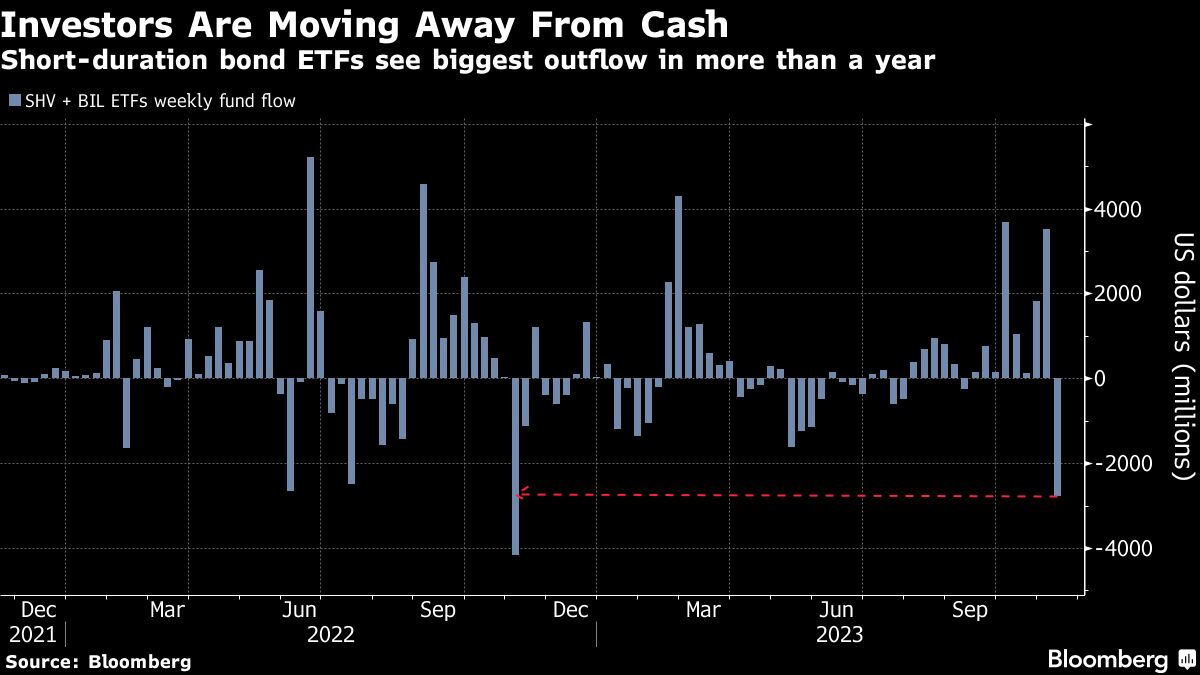

At the same time two big cash-like ETFs last week saw the biggest outflow since November 2022 with investors pulling nearly $3 billion — another sign that some money managers may be ready to deploy funds. Sentiment and risk exposure have also been improving over the past few weeks with investors turning more optimistic on both stocks and bonds in the latest Bank of America Corp. fund manager survey.

“This rally is driven by people being underweight risk in every form - duration, credit, stocks,” said Priya Misra, a portfolio manager at JPMorgan Asset Management. “All that money hiding out in money market funds felt good when inflation was high, the Fed was hiking and there were recession fears. Now there is a sense at least that the Fed is done.”

The sentiment was on full display on Tuesday, with a popular junk bond ETF rallying while the Russell 2000 index of small caps added more than 5%.

For Max Kettner, chief multi-asset strategist at HSBC Holdings Plc, there is still enough buying power among big investors to support a rally across risk assets.

“We are still some way off to pull the plug on that rally,” he said. “By our measures, shorter-term sentiment and positioning indicators are just neutral and real money investors continue to be underweight equities and high-yield credit on aggregate.”

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

More Exchange-Traded Products Topics >