Now that there’s a growing consensus that the Federal Reserve is done raising interest rates — a shift I predicted last month — it’s time to ponder when policymakers will consider cutting rates and by how much.

It’s common to think that wouldn’t happen until inflation returns to the Fed’s 2% target or the risk of recession is elevated. The first rate cut should and will happen sooner than that and not because of a dramatic slowdown in the economy. Given how the labor market and inflation have evolved, cutting rates by 50 basis points in the first half of 2024 would serve to preserve the expansion while maintaining a policy stance that’s at least somewhat restrictive and continuing to put downward pressure on prices.

Fed policymakers are unlikely to discuss the possibility of a rate cut at least until their December meeting. But since their last set of economic projections in September, both the labor market and inflation have trended weaker than their estimates — one obvious reason for them to shift from a rate-hike to a rate-cut bias.

The unemployment rate is now at 3.9%, above their 3.8% year-end forecast. The inflation data we got this week and the trend in recent months point to a year-end number close to 3.5%, compared with a fourth-quarter projection of 3.7% for the Fed’s preferred measure of core inflation.

It’s reasonable to think unemployment will worsen and inflation will slow further given that Fed Chair Jerome Powell believes monetary policy is “probably significantly restrictive” right now.

Core inflation at 3.5% would still be well above the Fed’s 2% target, but that number alone doesn’t capture the whole story. Between June and September, core personal consumption expenditures inflation has only increased at a 2.4% annualized rate, and October is looking similar. A continued weakening in shelter, a big component here, is baked in (something that was apparent even in July) as the sluggish rental market is slowly reflected in the government data. With the labor market now back in balance, there’s no reason to think wages will push inflation higher.

Importantly, at a time when policy is restrictive, the Fed can’t afford to wait until inflation is all the way back at 2% or the labor market is showing signs of dramatic weakness — by then the economy would likely already be in recession, which the central bank wants to avoid. Policymakers will want to be somewhat proactive. That’s where the idea of surgical rate cuts comes in — a possibility I raised last week, piggybacking on Powell’s “significantly restrictive” language.

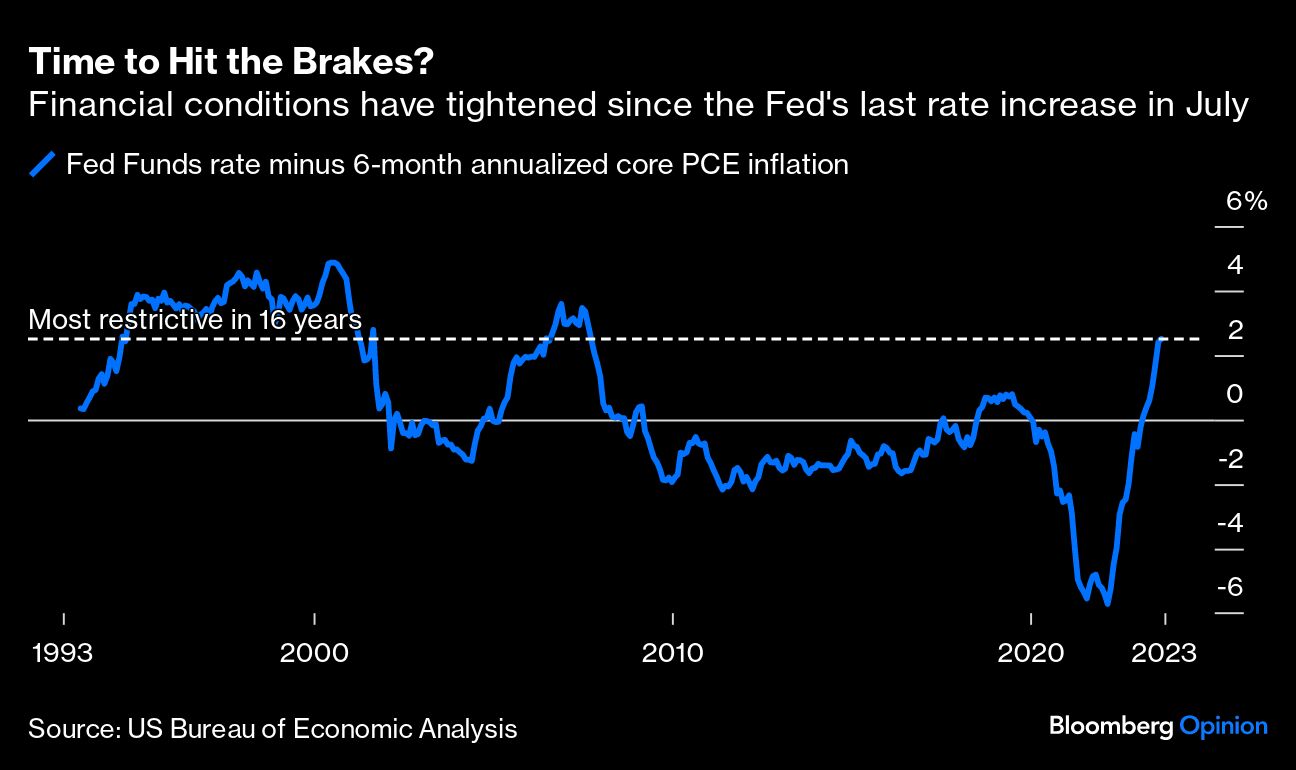

The belief that policy is highly restrictive stems from comparing the level of the fed funds rate to inflation. Using a six-month annualized measure of the Fed’s inflation gauge shows that monetary policy is more restrictive than it has been in 16 years and, importantly, has become tighter since July, even without further rate increases, because inflation has eased.

As price pressures continue to abate — the Fed projects more softening in 2024 — policy will get tighter and tighter if no rate cuts ensue. By lowering rates somewhat — I’d suggest a minimum of 50 basis points — the Fed can match some of the decline in inflation while hopefully being just moderately restrictive rather than “significantly restrictive.” This is arguably what the Fed did in 2019, when it lowered rates by 75 basis points even though the economy was not in recession.

It’s not uncommon to call for interest rate cuts, but there’s a significant division among economists about the magnitude, timing and reasons for policy easing. Goldman Sachs Group Inc. predicts the Fed will cut once in 2024, but not until the fourth quarter, while strategists at UBS Investment Bank anticipate sharp reductions as the economy slides into recession. The median forecast in a Bloomberg survey of economists is for the benchmark policy rate to be lowered 25 basis points in the second quarter.

My view, which markets are slowly coming around to, is that the central bank should and will cut sooner than that, perhaps as soon as March. The Fed should no longer have the kind of concern about overheating that it’s had for the past two years with the pace of core inflation arguably at 2.5% or lower, and more softness coming from shelter in the months ahead. The recent slowdown in the labor market also means that policymakers can’t rule out a much worse outcome in 2024. Policy is already tight and, in the Fed’s eyes, getting tighter as inflation slows.

If monetary policy were an automobile, better to “take your foot off the brake a bit now,” which is how the Fed would frame it, than to risk crashing by delaying the decision too long. The Fed’s March meeting — to which markets now assign around 35% odds of a rate cut — is still four months away, plenty of time to make sure the inflation data continues to cooperate and to prepare markets for the policy shift.

Recalibrating policy by proactively cutting rates is the best approach to sustain the expansion while continuing to be mindful of inflation concerns.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our full schedule of upcoming CE-approved virtual events.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.