The pandemic upended many of the things we thought we knew about the economy. Even now, economists struggle to answer such fundamental questions as whether Americans are better off financially. Answers vary significantly depending on the data source, sowing confusion. The end result is that business and households seem to be losing trust in the data and have become increasingly unwilling to participate in the surveys that underlie official statistics such as unemployment and inflation that, in turn, help inform decisions made by government officials and central bankers.

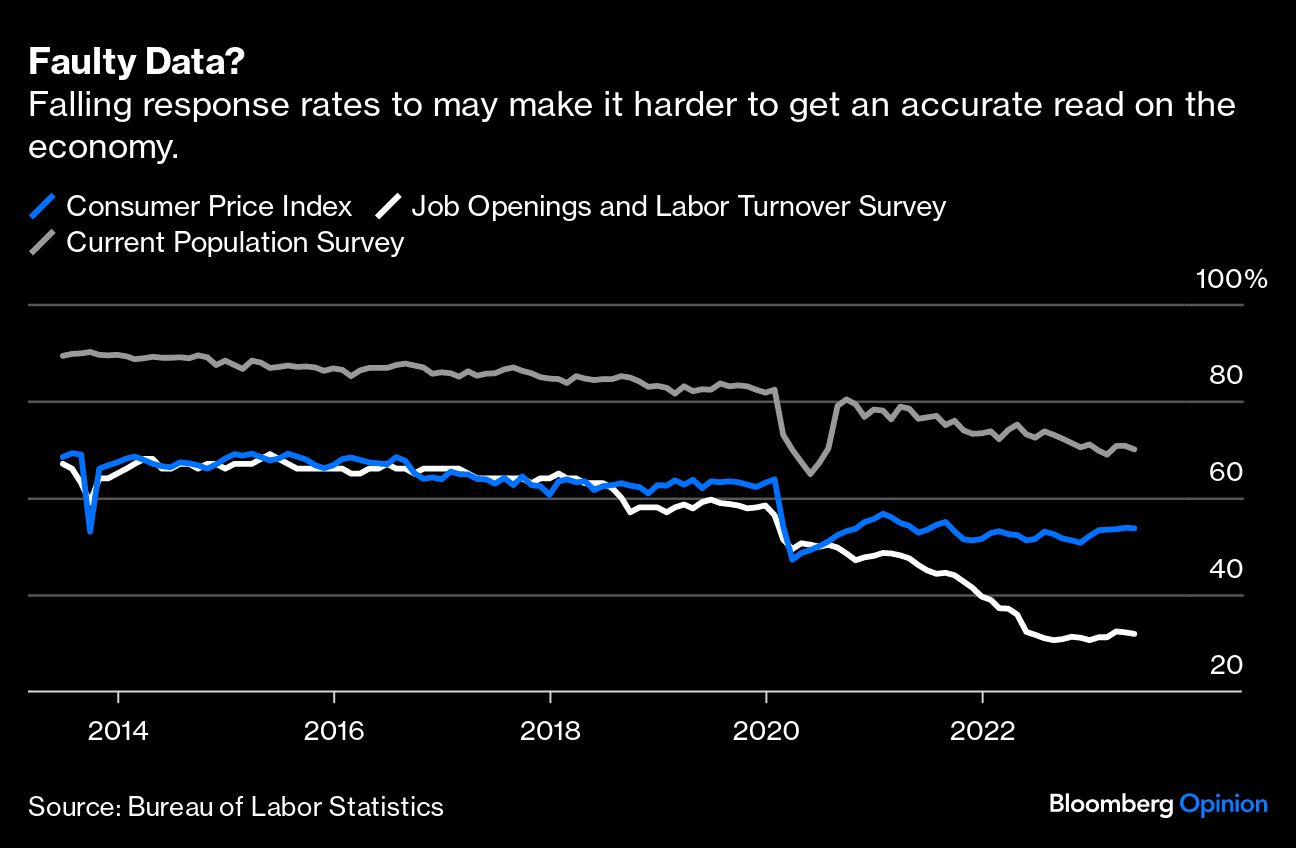

Sure, COVID-19 made conducting surveys extremely difficult, but the recovery still left response rates short of the pre-pandemic levels. Take the Job Openings and Labor Turnover Survey, or JOLTS. Bloomberg Businessweek reported earlier this year that the response rate to the survey had plunged by half to 31%. At the same time the response rate fell, the Federal Reserve drew increasing attention to the record high unfilled openings that the survey reported. What the Fed viewed as an “extremely tight labor market” was part of its rationale for raising interest rates so rapidly, boosting the cost of everything from mortgages to credit cards and student loans.

US Census Bureau survey director Carolyn Pickering says there is no indication that the decline in response rates in government surveys has degraded the data quality. And the rates are far higher than surveys done in the private sector or by non-profits, which also have declining participation rates. Nevertheless, even though official government statistics remain our best pulse of the economy, they are at risk of sending false signals.

Lower participation rates can mean that the data initially collected are not representative of the population, and statistical adjustments are required for estimates to accurately reflect conditions. There are limits to the adjustments, especially for smaller or hard-to-reach demographic groups — often ones we most want to study for policies — such as minorities, those with less than a high school degree or young adults. And it can make it harder to sort out disagreements across surveys.

So why is participation in surveys declining? The answer is complex. One reason is that distrust makes people less willing to share details of their lives, and distrust in government has risen steadily over the past several decades to eight in 10 individuals in 2022, according to the Pew Research Center. That undermines the collection of data. The first words people hear in the Census Bureau’s Current Population Survey is, “I'm calling … to obtain the governments statistics on employment and unemployment.”

Unsurprisingly, distrust extends to the data itself. A Marketplace-Edison Research poll in 2020 found that 40% of adults said they either “somewhat distrust” government economic data or “did not trust it at all.” As with pessimism about the economy in sentiment surveys, people’s distrust in economic data is higher when their party does not occupy the White House. In that sense, economic data are about more than economics.

There are ways to restore the connection and trust between Americans and government surveys. Most importantly, it helps people “see themselves” in government statistics when the data analysis elevates differences across groups and shows how that information rolls up to the macroeconomy. Given the inequalities across people and communities, it's essential.

The Distributional Financial Accounts the Fed created in 2019 are a good example of how to make that connection. It uses aggregate data on wealth from financial institutions and a household survey of wealth to merge the macro and micro. As such, we now know the top 0.1% of households by wealth have five times more wealth than the bottom 50%. How much wealth the country has and who has it are both facts that should inform policy. The first step is to know that such data exist, and economists must use the figures.

Another step is lowering the costs of and raising the benefits of participating in government surveys. According to Pew, two-thirds of adults see the risks of participating in surveys, such as privacy concerns, as greater than the benefits. One way to lower costs and raise participation is to shorten surveys and provide internet and mobile phone options. The Survey of Household Economics and Decisionmaking at the Fed undertook such efforts in 2018 and targeted monetary incentives to hard-to-reach groups. The result was a 10-percentage-point increase in the participation of those groups relative to the prior year. Another way to reduce the burdens is to use administrative or private-sector data when possible. Answering questions about data safety and how it will be shared is crucial.

Meanwhile, economists and policymakers who use government statistics must recognize the limits of the data. Government data are not “fake news” or part of a conspiracy, but they are not perfect either; the surveys require more funding to preserve the integrity and trust in surveys. Without facts we can agree on, we will be without agreement on policy.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Claudia Sahm