Citadel and Its Peers Are Piling Into the Same Trades. Regulators Are Taking Notice

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsEven Ken Griffin is a little worried.

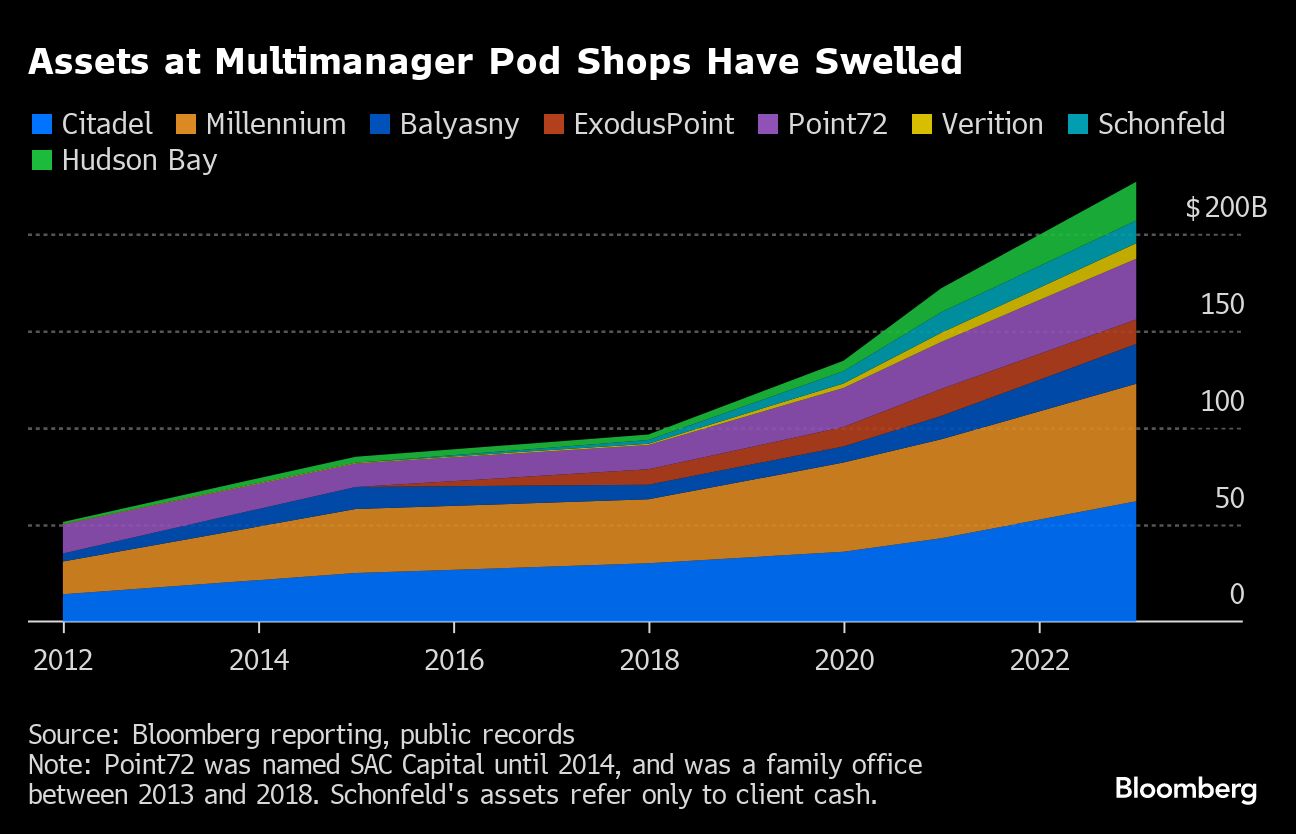

Multimanager funds like Griffin’s Citadel have come to dominate the hedge fund industry, riding a steady run of outperformance to oversee more than $1 trillion, including a healthy dose of leverage. But the explosive growth has led the industry giants to pile into many of the same trades.

That has built unease among regulators, investors and traders over these so-called pod shops. And while Citadel’s billionaire founder has vocally opposed any notion that his firm and rivals pose systemic risks and need more regulation, even he acknowledges that crowded trades could lead to widespread losses if all of them head for the exits at once.

“Could you see the multimanager hedge funds take a joint 10, 15, 20% hit to their equity? It’s possible,” Griffin said during a Nov. 9 interview at a Bloomberg conference in Singapore, calling such a drop “painful, but not systemic.”

Citadel, Millennium Management and Balyasny Asset Management are the leaders in a strategy that divvies up money across dozens or even hundreds of teams that operate somewhat independently across a range of markets and strategies.

Their success in the past several years has drawn new investors and competitors. Yet overcrowding in some bets, increased market volatility, an expensive talent war and lower returns this year have prompted market participants to question whether the world of high finance is approaching peak pod.

Officials at the Securities and Exchange Commission and US Treasury Department have warned that the firms’ favored basis trade could destabilize Treasury markets. At least one large bank is approaching the limit of how much it’s willing to lend to them, and some investors are growing more wary.

“There’s some overcrowding and concern about the amount of leverage at individual firms and collectively,” John Jackson, head of hedge fund research at investment consultant Mercer, said during a recent Capital Allocators podcast. And because they typically cut risk very quickly “we are worried about the potential snowball effect.”

Some investors are capping the amount of money they allocate to these funds, fearing blowups. Others are avoiding newer entrants, saying they could be hurt the most by a big unwinding. Smaller hedge funds, meanwhile, are looking for ways to profit from the market dislocations these larger competitors create.

It all amounts to a fault line in what has been a largely envied corner of the hedge fund universe — where pod shops have attracted more assets and star talent, driven up compensation and generated years of steady returns for investors.

Tight risk controls helped them deliver those gains. If portfolio managers lose even a few percent, they’re generally forced to reduce or even liquidate positions. And because the pod shops traffic in so many markets — and not in big directional bets — no single investment will make all of the money, or sink a firm.

As of midyear, there were 55 pod shops — multistrats and single strategy — overseeing $368 billion, with about half that amount controlled by the five biggest firms, according to a September Goldman Sachs Group Inc. report. That’s up from 29 firms running a combined $149 billion in 2018.

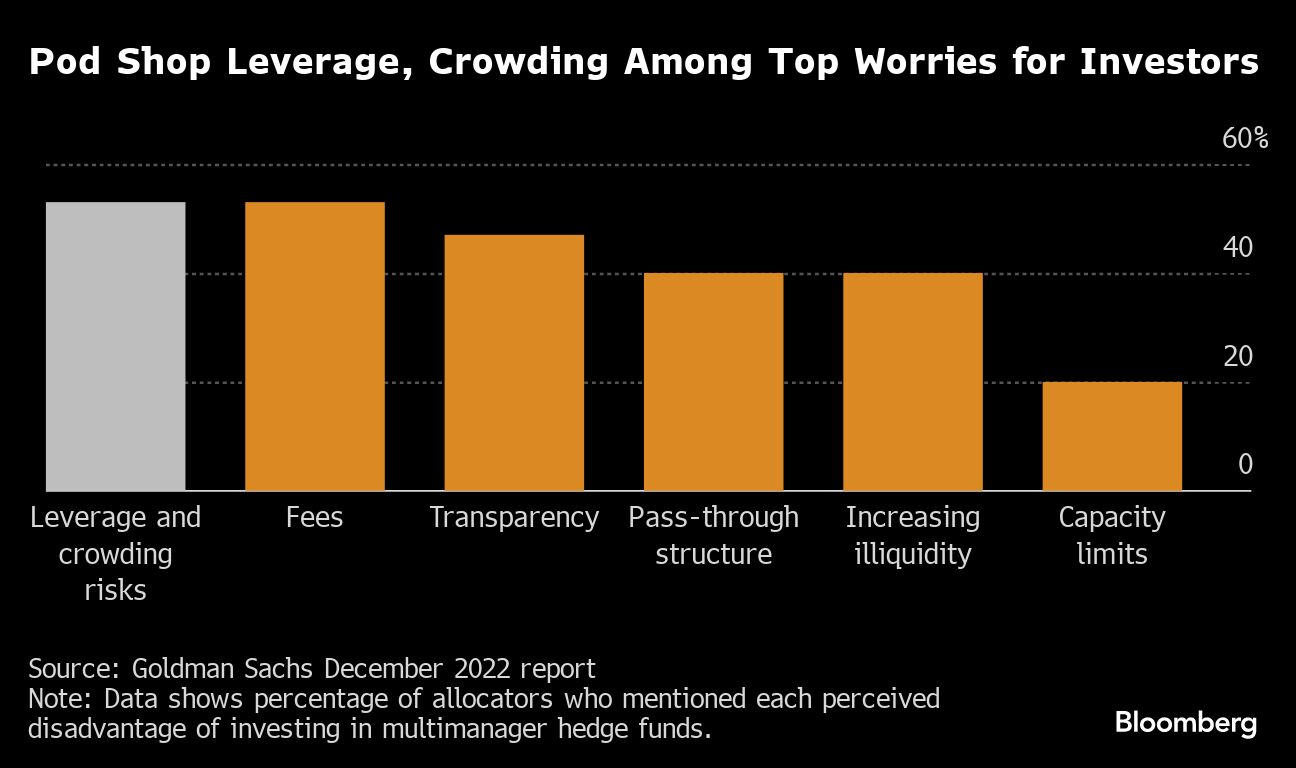

Investor interest, though, may have peaked. Clients are now fixated on leverage and the risk of “platform de-grossing” — or stampede selling — Goldman Sachs said in an earlier report. And 8% of those interviewed in June said they planned to pull money from multistrat funds in the second half of the year, up from 4% six months earlier.

Some smaller firms are struggling amid the increased competition. Schonfeld Strategic Advisors has barely made money this year and investors have pulled $2.3 billion from its funds. It almost partnered with Izzy Englander’s Millennium, a much larger rival, but instead found new and current clients who said they’d be willing to invest up to $3 billion.

Even with more assets and stiffer competition, Citadel continues to be among the most aggressive risk-takers.

While Griffin’s firm gets high marks from S&P Global Ratings for sound risk management, healthy cash levels and sticking to liquid investments, the credit-grading company called Citadel’s appetite for opportunistic, concentrated bets a negative, highlighting its big wagers on natural gas and power — sectors prone to large price swings — in 2021 and 2022.

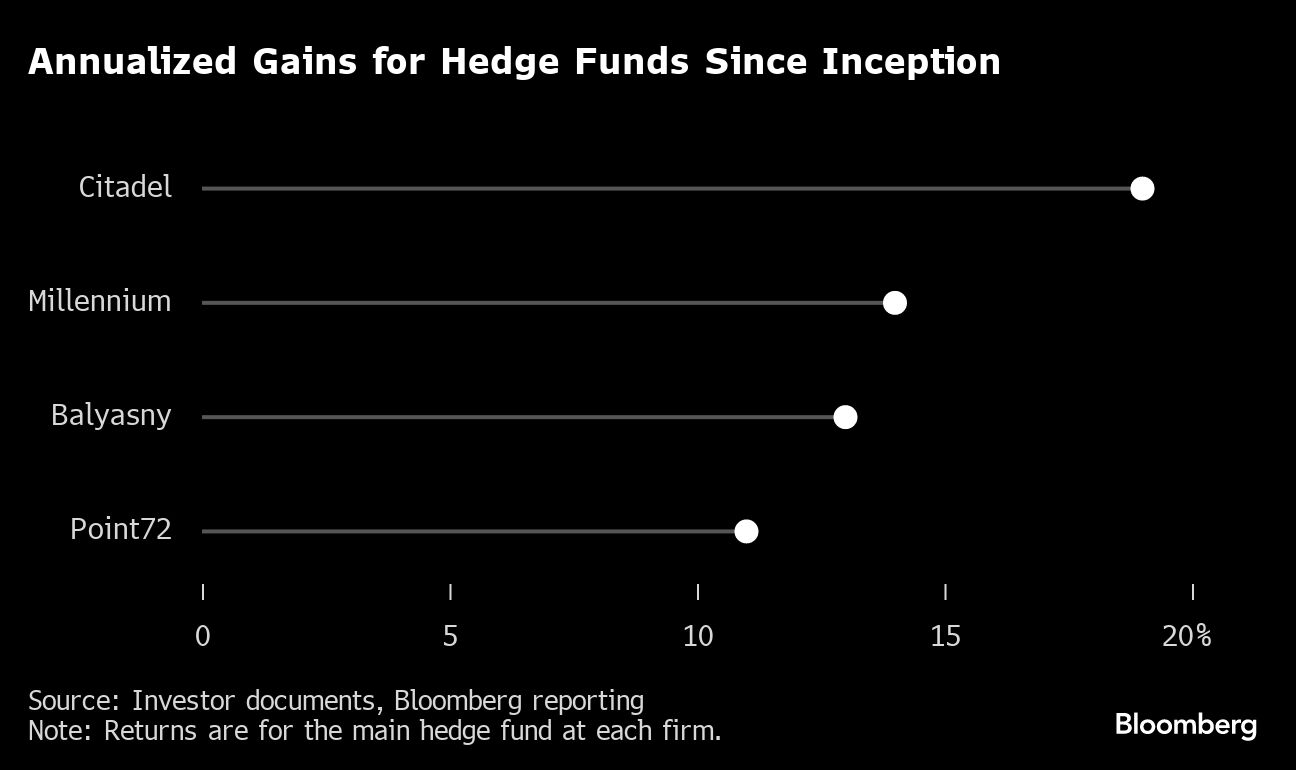

Citadel gained 38% last year, with about $8 billion — half the profits of its main hedge fund — coming from commodities, according to people familiar with the matter.

With $62 billion of assets under management, Citadel is so big that its trades “could at times represent a high multiple of average daily trading volumes,” potentially limiting its ability to sell quickly without sending prices tumbling, S&P analyst Thierry Grunspan wrote in an April report.

“We are in the risk-taking business,” Citadel spokesman Matt Scully said in a statement. “Our investors expect us to deploy their capital against the most attractive opportunities we see in the market.”

The fund gained 13.7% this year through October, while many other multistrats posted returns in the single digits.

“Our performance is driven by the extraordinarily talented people at Citadel,” Scully said. “We have the best investment team in the industry.”

Yet Citadel is the only one of its main competitors that has almost imploded. In 2008, its main fund lost 55%, or roughly $9 billion — mostly in convertible, high-yield and investment-grade bonds and bank loans. At the time, Citadel was managing less than a third of the assets it oversees today. Since then, Citadel has said it learned from the episode and avoids illiquid investments.

Millennium, Citadel’s closest competitor, produces steadier returns. Its annualized swings in performance are less than 4%, according to a Bloomberg analysis. Englander’s firm, which manages about $60.6 billion, has generated annualized returns of 14% since its founding in 1989. Dmitry Balyasny’s hedge fund has a similar profile.

Much of the increased regulatory focus has been in Treasury markets, where leverage tends to be the highest. Hedge funds in aggregate had estimated leverage of 56-to-1 on $553 billion of Treasury repo borrowing as of December 2022, according to a September research note by Federal Reserve staffers Ayelen Banegas and Phillip Monin.

That’s why many of the big firms incurred larger-than-expected losses during the early days of the Covid-19 pandemic. They were caught in the so-called basis trade, which is designed to profit from small differences between Treasury futures and the cash market. Considered a safe arbitrage bet if held to maturity, it can occasionally go haywire, as it did in March 2020. The Fed was forced to step in to calm markets, pledging $5 trillion of stimulus.

A succession of mini quakes — including March 2020 — prompted the Bank of England to include Citadel, Millennium, LMR Partners and Steve Cohen’s Point72 Asset Management, as well as other hedge funds, in its stress tests.

LMR, an $11 billion pod shop with no down years until then, was among the biggest casualties that month. It had made highly leveraged trades, wagering around volatility arbitrage, dividend arbitrage and the basis trade. As bets across the industry imploded, its main LMR Multi-Strategy hedge fund plunged by a record 24% — mostly hit by vol arb — according to investor letters seen by Bloomberg. Meanwhile, the LMR Alpha Rates Trading Fund, which counts the basis trade as a key strategy, lost 4%, also its worst month ever, the letters show.

In response, the firm exited strategies including relative value trading in credit, equity index and cross asset. It shut the LMR Long Horizon Fund after its bets on volatility backfired. The firm also bolstered its risk-management team, appointed product heads and embarked on a more rigorous monitoring of its portfolio managers. The multistrategy fund ended the year down 6%, its only annual loss since its debut. The rates fund fully recovered.

Losses rippled through almost every big multistrat shop, and at least one trader likened the panic to the 2008 financial crisis.

While interviewing Griffin last month at an event in New York, fellow billionaire Paul Tudor Jones said his hedge fund’s basis-trade book was in “extreme duress” in March 2020 and that the Fed’s action bailed him out. Griffin replied that Citadel was down as well, but that “it wasn’t meaningful,” relative to the firm’s capital base.

Griffin, 55, called the recent hand-wringing over the trade by the SEC, Treasury Department and BoE “a regulatory jihad,” instead arguing that hedge funds are actually forces for good, providing liquidity and saving taxpayer money.

Should another Treasury market hiccup occur, the Fed — having learned from the early days of the pandemic — will probably act faster and in a more targeted way, said Rob Robis, chief strategist for BCA Research’s global fixed income strategy.

But further central bank action may embolden traders to be more aggressive.

“It incentivizes them to double-down on trades” because they assume the Fed will backstop them, said Medley Global Advisors economist Michael Redmond, who previously worked at the Treasury Department. Risk-taking could get so out of hand that intervention might not be enough or come too late, he said.

At least one large prime broker has set limits on how much more leverage it will provide to multistrats and macro hedge funds, a person with knowledge of the matter said. Other lenders are watching the borrowing of these money managers more closely.

The basis trade isn’t the only highly leveraged wager to cause trouble. Wagers on stocks being added to or removed from equity indexes —- known as index rebalancing — fueled losses for hedge funds in 2020 and 2022 because of crowding. One fund manager estimated that a dozen firms were doing the trade in 1998, compared with at least 50 in recent years — including various pods at the big multimanagers — before deteriorating returns drove traders away.

‘Crowded Theater’

There’s more crowding across equities, too.

Multimanager firms now hold 30% of the gross market value in US stocks, up from 27% last year, largely because of more leverage, Goldman Sachs said in its September report, adding that they now have “a larger market footprint” than traditional stock-picking hedge funds.

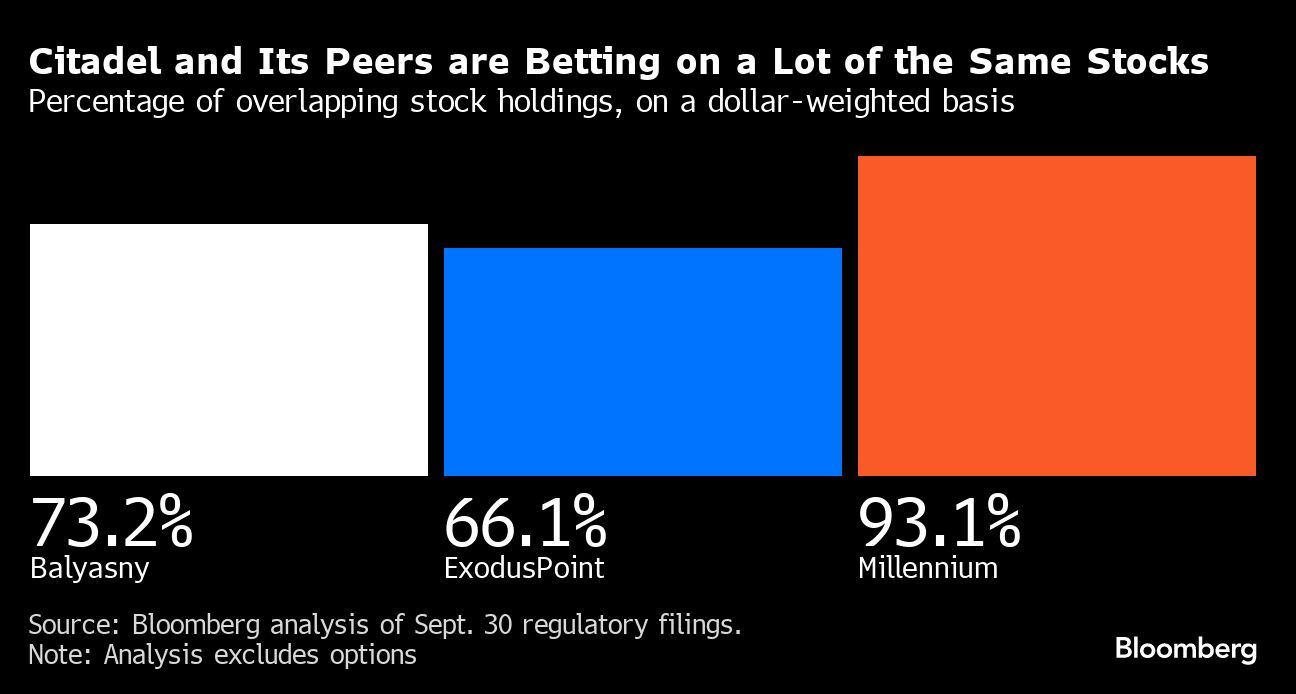

Of the $90.7 billion that Citadel held in US stocks at the end of September, 93% was in shares Millennium also holds, according to a Bloomberg analysis of regulatory filings.

Firms are locking up capital for longer — in some cases as many as five years — something investors fear is incentivizing traders to acquire securities that are harder to value and unload in a crisis. Clients point to the high demand for distressed-debt teams at multistrats as proof of this migration toward harder-to-sell assets.

Some of the industry’s most prominent investors, who asked not to be identified discussing individual managers, said they entrust their money only to the largest hedge funds, worried that smaller multimanagers won’t be able to withstand an unwinding that comes from overcrowding. Those firms may be less diversified, have less robust risk systems and less money to compete for top talent.

Other firms are trying to profit from the increased market volatility. Magnetar Capital, co-founded by ex-Citadel trader Alec Litowitz, implemented a short-term strategy to its quant funds several years ago that tends to make money after multistrats cut their crowded equity positions en-masse.

There’s also a new generation of multistrats, including ClearAlpha Technologies and New Holland Capital, that are shunning the most common trades to minimize risk and boost returns.

Freestone Grove Partners, a new multimanager specializing in stocks, is limiting the number of pods it will use to as many as 20, telling investors any more reduces returns.

“Everyone says ‘We are going to be the one that is able to run out of the crowded theater,”’ said New Holland Chief Executive Officer Scott Radke, whose firm manages about $6 billion. “But it works less well as the theater gets more crowded, and maybe you are less nimble than you thought.”

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Bloomberg News provided this article. For more articles like this please visit bloomberg.com.

Read more articles by Katherine Burton, Hema Parmar, Madeline Campbell, Nishant Kumar

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All