Decades-high interest rates are poised to revive interest in a little-used corner of the municipal-bond market: variable rate deals.

That’s according to the public finance leaders at JPMorgan Chase & Co., the third-biggest underwriter in the $4 trillion market who say talks with US state and local government clients about short-term securities, typically tied to variable interest rates, are picking up.

The Federal Reserve’s tightening regime continues to ripple through the muni bond world with the talks signaling a shift away from years of bond sales being structured with fixed-interest rates as municipalities tried to lock in ultra-low borrowing costs.

Such discussions with issuers haven’t taken place in a long time, according to Jamison Feheley, head of public finance investment banking at the bank.

“It was really hard to argue against — why would you do anything but long, fixed-rate debt when 30-year paper was in the 2% range?” Feheley said in a Zoom interview on Nov. 29. “Why wouldn’t you lock that in?”

Now, he said issuers are thinking strategically about whether to incorporate short-term debt products into their portfolios. He said they may be reluctant to “lock in” their debt with longer, fixed-rate bonds while rates remain elevated.

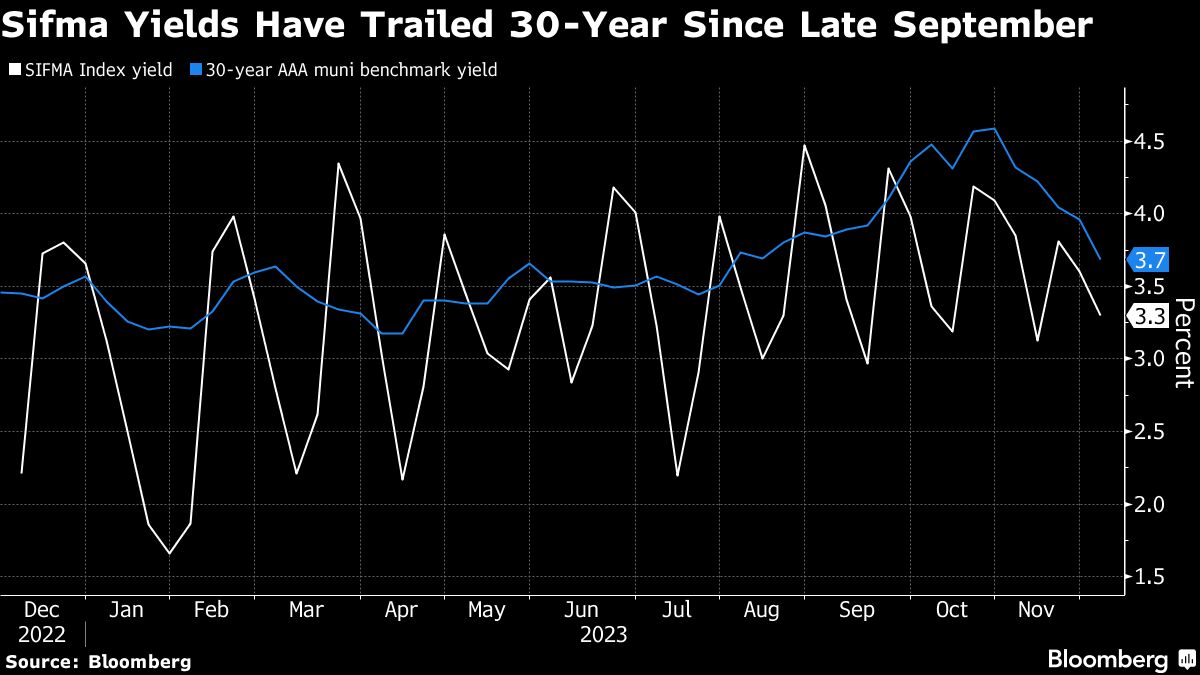

Floating-rate notes, for example, can be tied to the yield on the Sifma Index which is currently 3.3%. Yields on the gauge of short-term municipal borrowing costs that resets weekly have been below fixed-rate 30-year AAA benchmark debt, which currently sits at 3.7%, since September.