It seems Federal Reserve policymakers have gone from zeroes to heroes. Early last year, critics — and there were many — said the Fed was woefully behind the curve on inflation, and that the only way it could win the battle was to push the economy into a damaging recession by raising interest rates very high, very fast.

Well, the Fed did just that, increasing its key rate from almost nothing to 5.50%. Inflation has now slowed to within sight of the central bank’s 2% target. But instead of contracting, the economy has gathered strength, expanding in the third quarter at an annualized rate of 5.2%, the fastest pace since 2014 if you exclude the wild gyrations during the pandemic years. And the unemployment rate has held below 4% for 21 straight months, the longest stretch since the 1960s. The Fed’s critics? Many now admit the economy may achieve what they said was impossible: a fabled “soft-landing.”

But before the Fed takes a victory lap, it’s worth asking just how much the Fed’s actions contributed to the slowdown in inflation. The answer may be not a whole lot. And if that’s the case, the Fed risks overestimating the benefits and underestimating the costs that high interest rates impose on the economy.

The way monetary policy is understood to work is that the central bank boosts rates to suppress demand throughout the economy and lowers them to achieve the opposite effect. And the latest data would suggest the Fed tightened policy precisely enough to temper demand and squeeze out excess inflation without sparking a massive rise in unemployment. Yet it’s difficult to identify any sector of the economy outside of housing in which monetary policy has been instrumental in curbing demand.

In theory, rising interest rates should discourage borrowing and, by extension, lower spending, especially for consumers, who account for about two-thirds of the economy. Instead, balances on things like credit cards and the amount of auto loans outstanding have increased at an accelerating pace. Some would say this is just a reflection of elevated inflation, and consumers are being forced to go into debt to make ends meet. The reality is that consumers are rational and have historically tended to only boost borrowing when they are feeling good about their incomes and jobs status, which makes sense now given the strength in the labor market.

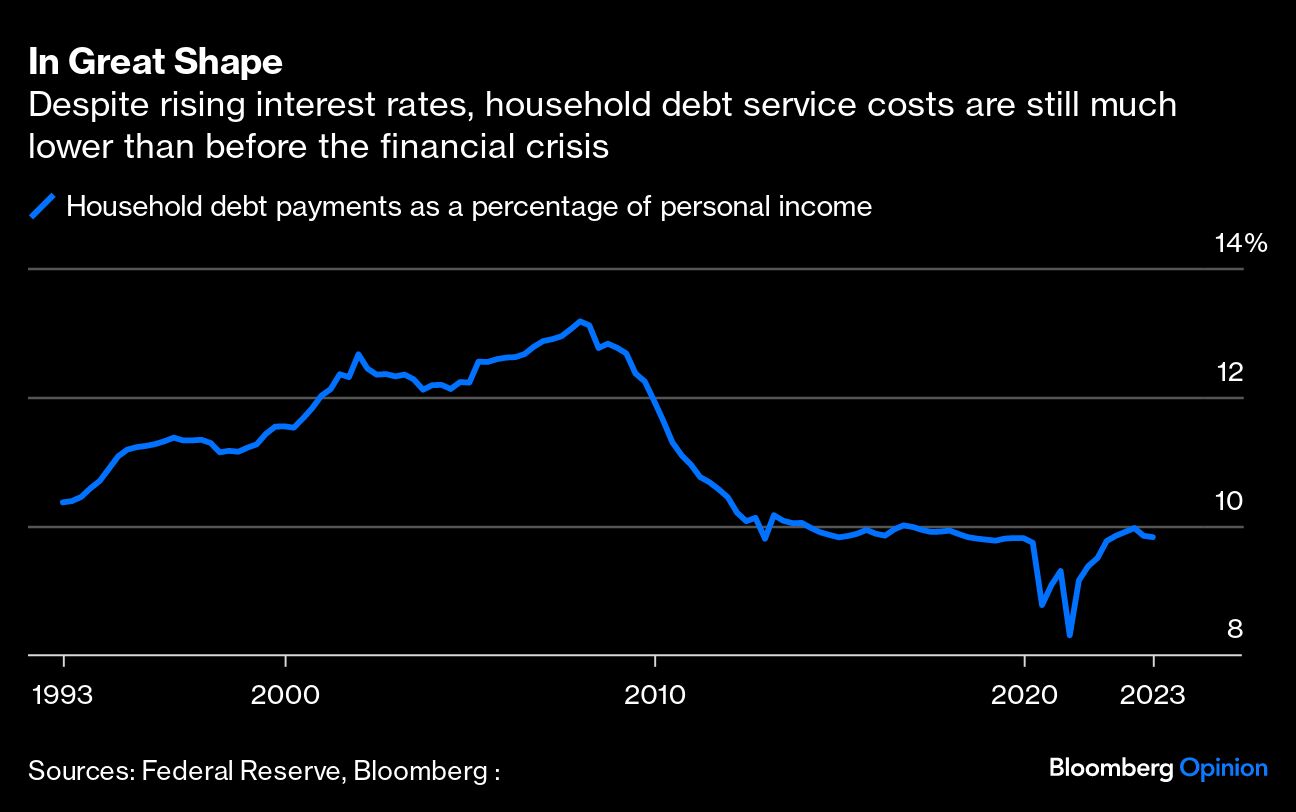

Perhaps it has something to do with the strength of household finances. By some measures, consumers still retain a large chunk of savings built up during the pandemic. In addition, tens of millions refinanced their mortgages at historically low rates, freeing up cash they would otherwise spend on servicing their home loans. Some of that extra cash, along with government stimulus payments, went to paying down debt. Overall household debt payments as a percentage of disposable income stands at 9.83%, unchanged from pre-pandemic levels and down from the peak this century of 13.2% in 2007.