US company earnings are likely to weaken in the fourth quarter before a rebound in 2024, according to Morgan Stanley’s Michael Wilson.

The strategist highlighted a “steep downward revision” to consensus fourth-quarter estimates and added that he is less optimistic than other strategists about the magnitude of margin expansion next year. “We see earnings risk persisting in the near term before a broader recovery takes hold as next year evolves,” he wrote Monday in a note to clients.

The strategist has been negative on stocks for most of the year even as markets rallied alongside economic resilience and expectations that the Federal Reserve has completed its interest rate-hiking cycle. He said in October that a year-end rally was unlikely, but the S&P 500 Index has gained about 11% since then.

Wilson told Bloomberg Television on Monday that monetary policy and fiscal spending are likely to normalize in 2024, but not until the second half of the year. Until then, “it’s going to be very challenging for us to see an acceleration of growth,” he said.

Against that backdrop, Wilson said quality and large-cap defensive stocks are likely to continue to outperform until the current market cycle ends, either with a hard landing or “some new exogenous shock or driver for positive growth.”

Only then can investors expect a broader and more sustainable stock rally, according to Wilson, who called a no-landing scenario a “fantasy.”

“The status quo of decelerating growth and falling inflation typically is not good for equities,” he said.

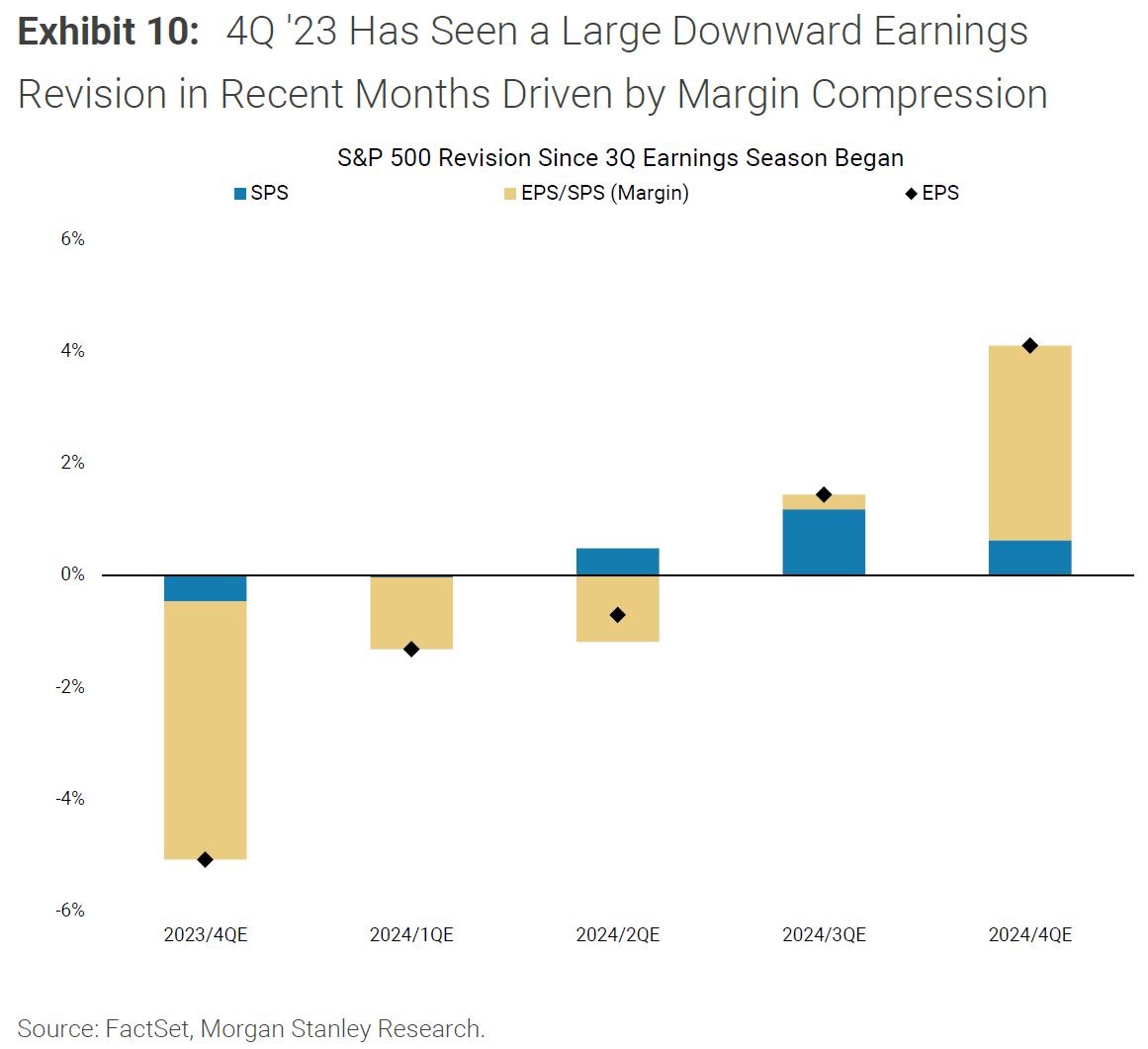

Estimates for fourth-quarter S&P 500 profits have fallen 5% since the previous reporting season began, Wilson said. Typically, consensus estimates for the current year’s earnings-per-share decline by nearly 5% through the course of the year and, if that precedent holds, US corporate EPS should fall to around Wilson’s estimate of $229 by the end of 2024, he added.

Data compiled by Bloomberg Intelligence show the same trend of falling estimates for the fourth quarter, with Wall Street now expecting year-over-year earnings growth of 1.5% in the period. Meanwhile, consensus estimates are for S&P 500 EPS to climb 11% to $246 next year, a more bullish outcome than predicted by Wilson. The strategist said, however, that he was “very bullish” on earnings in 2025.”

Wilson remains focused on pricing power and will be monitoring this week’s producer prices data for signs that pricing trends are either stabilizing or decelerating further, especially after NFIB business survey data indicated that companies are now planning to raise prices into 2024. “This optimism may be an early sign pricing power is set to stabilize, though the PPI data will be important to watch for confirmation,” he said.

Continued evidence of cooling producer prices would be welcome by US corporates to help bolster their pricing power and lift margins. The last earnings season marked the end of the first US profit recession since the pandemic and all eyes will be on whether the recovery can continue next year.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Farah Elbahrawy, Alexandra Semenova