When private equity firms push into an industry, you know there are decent returns to be made. Just consider their enthusiasm for the arcane business of insuring corporate pensions.

A company’s retirement liabilities are a nightmare for the chief financial officer. They’re an imprecise long-term debt, introducing volatility to the company balance sheet. Regulation discourages investment in higher-returning assets like equities that would help pay the pension obligations when they come due. Hence CFOs are desperate to offload the burden to anyone who will take it on. The insurance industry is happy to oblige – for a fee.

The situation is exemplified in the plight of Walgreens Boots Alliance Inc. The US pharmacy chain has been struggling to sell its UK Boots subsidiary. The pension plan was likely deterring suitors. Last month, Walgreens transferred the liability to Legal & General Group Plc. The transaction valued the burden at £4.8 billion ($6 billion), making it a record deal for the UK insurer. L&G receives the plan's investment portfolio, but Walgreens also agreed to inject another £500 million and accelerate £170 million of top-up payments already committed. Think of Walgreens as paying a fat fee just to have the chance of turning one of its core operating businesses into cash.

The high price of such pension transfers had hitherto put them out of reach for most corporations. But deals are becoming more affordable. Rising interest rates reduce the accounting value of retirement liabilities, in many cases cutting pension deficits (a shortfall in assets matching the obligations). So insurers are now charging lower premiums to take on underfunded plans. The UK market is expected to see particularly strong growth, with deal flow set to exceed £50 billion annually in the coming years, potentially touching £70 billion, according to consultants Hymans Robertson.

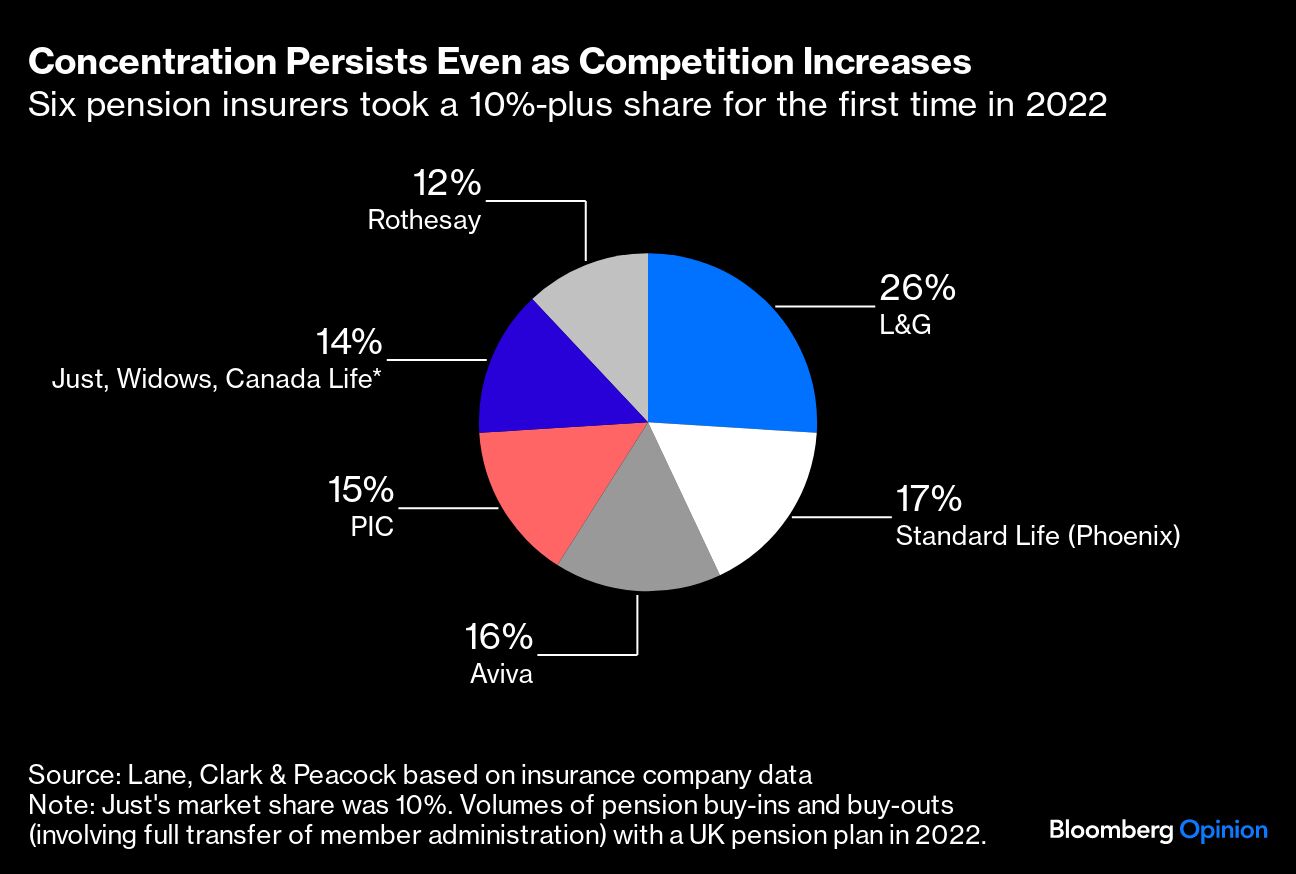

This surge in demand meets a small number of insurers capable of the underwriting. Regulation creates high barriers to entry in terms of capital and expertise. Just four players — L&G, Phoenix Group Holdings Plc, Aviva Plc and Pension Insurance Corp. — have 74% of the market, according to consultants Lane Clark & Peacock. It looks like an oligopoly.

Pricing power is strong. Valuing pension liabilities requires assumptions about, say, life expectancy and inflation. Insurers use ultra-conservative inputs and the resulting valuations are far larger than those produced by other methods. Given the pension plan’s assets typically won’t be as high as the liability so calculated, the company makes a top-up payment to the insurer to ensure reserves are sufficient to weather a storm.

Then the insurer puts up some of their own capital as a cushion. But L&G’s numbers here are striking. It calls its business “capital light,” saying it deployed just £270 million of capital while generating some £12 billion of so-called pension risk transfer business year-to-date.

The insurer’s profits are generated if the gains on the assets – typically low-risk debt and infrastructure investments – exceed the cost of paying the pensions, and capital is released as retirees pass away. The payback can take many years to come through. But over time it looks great: Analysts at UBS Group AG suggest internal rates of return can be as high as 20%.

Sure, there are long-term risks. The insurer is on the hook if life expectancy rises or the investments don’t perform. But since the corporate client stumps up such high reserves in the first place, a large margin for error is already built in.

There are obvious opportunities for private capital firms. But they may stop short of setting up in direct competition against the incumbents. One option is helping source investments that generate yield. Another is reinsurance. A traditional insurer may offload, say, 25% of a pension buyout to a reinsurer. This “funded reinsurance market” is growing fast. Resolution Life, backed by Blackstone Inc., recently announced its maiden deal. KKR & Co. last month moved to take full control of Global Atlantic Financial Group LLC, a major player in this area.

Meanwhile, Carlyle Group Inc. is mulling whether it should get involved, Bloomberg News reported. For already established firms like PIC, backed by billionaire Johann Rupert and CVC Capital Partners, now may seem an opportune time to bring in new investors — or sell up.

There are threats on the horizon. UK policymakers are keen to ensure companies have other options to free themselves from the pension shackle. They’re considering letting the Pension Protection Fund, which takes on the pension plans of failed companies, adopt those of solvent institutions too. The PPF doesn’t need to make a profit and its indefinite investment horizon means it can afford to invest in riskier assets like equities. It could potentially offer pension transfers far more cheaply than the insurance sector, while simultaneously supporting productive investment.

If private capital doesn’t disrupt this industry, the public sector looks more than capable of stepping up.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our full schedule of upcoming CE-approved virtual events.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Chris Hughes