The broader industrial economy is set to enter 2024 on shaky footing as an inventory hangover from the supply-chain crisis starts to look more and more like a prelude to underlying demand weakness and the reality of the reshoring boom proves much more nebulous and in flux than the prevailing narrative. What was a perception of rising tides is increasingly becoming more about which specific boats float or sink when the economic waters become choppier. So as 2023 draws to a close, it’s a good time to take stock and reflect on this past year’s industrial winners and losers.

Winners

General Electric Co. took an early lead as the top performing industrial stock on the S&P 500 Index and never let it go, with the shares on track for the best annual return of the millennium. Under the leadership of Chief Executive Officer Larry Culp, the onetime quintessential industrial conglomerate is speeding toward a much more simplified future. GE spun off its health-care business in January and is on track to carve out its gas and wind power operations by April. That will leave GE focused on its premier aerospace business with a few legacy liability stragglers — namely the long-term care insurance business. After decades of chasing fads with expensive deals and unearthing unwelcome surprises in the folds of its corporate sprawl, it finally seems as if GE’s businesses are in the right place at the right time.

While some US airlines, particularly lower-cost carriers, are having to discount tickets to fill up domestic seats, the world is still short airplanes overall. Vertical Research analyst Rob Stallard estimates airlines globally will need 600 more jets over the 2023-to-2028 period than aircraft makers are currently set to produce as supply-chain challenges continue to foil plans to bolster output. This will force carriers to defer retirements of older planes and pack more people into them. The extra wear and tear should be a boon to GE Aerospace’s maintenance and services business. GE and Safran SA, partners in the CFM International engine joint venture, raised prices on spare engines by a high-single digit percentage in August, four months earlier than normal.

Orders for equipment and services in the aerospace division jumped 34% in the three months ended in September, while the unit’s profit margin swelled to more than 20%, more than double the return on sales at RTX Corp.’s rival Pratt & Whitney unit even after adjusting for a charge from a significant recall of its geared turbofan engine. RTX expects that an average of 350 planes from the GTF-powered Airbus SE A320 fleet will be grounded annually from 2024 through 2026, with a peak of as many as 650 aircraft out of commission in the first half of next year, according to a September update. While the Leap engine that GE produces through the CFM venture has had its own durability hiccups, including fuel-nozzle coking and distressed blades, the resulting disruptions to the in-service fleet have been comparatively minimal. And that’s the other reason GE shares have soared in 2023: After years of being the industrial problem child, the company has left the mushrooming nightmares to its peers.

Costly equipment defects in onshore wind turbines resulted in a €4.6 billion ($5 billion) loss at Siemens Energy AG for the fiscal year ended in September and forced the company to secure a €15 billion financial backstop from the German government, a consortium of banks and its former parent Siemens AG. While GE expects its offshore wind operations to lose about $1 billion both this year and next, its grid and onshore wind units clawed their way to profitability in the third quarter and are expected to make money next year. The company hasn’t had to top off a $500 million warranty provision taken in 2022 for wind turbine performance issues. And soon that business will be someone else’s problem anyway.

Eaton Corp. and the electrical equipment industry more broadly had a moment this year amid a surge in spending on data centers and a gush of government funds intended to grease the wheels of the energy transition. Eaton shares have jumped about 50%, while those of Vertiv Holdings Co. have more than tripled. Artificial intelligence can’t exist without electrical equipment. The technology works best with graphics processing units, or GPUs, which are capable of processing huge streams of data in parallel but require twice the power of traditional central processing units and more sophisticated electrical distribution. The US is on track to build a new data center every month, Siemens AG CEO Roland Busch told me in an interview last month. Beyond that, “whatever you want to power with renewables, it will be electrified,” he said. This means electric vehicles, charging stations and batteries but also semiconductor plants and other kinds of energy-intensive manufacturing. Siemens’ North American electrical products business has already booked enough orders to cover the investment for a $150 million switchgear plant it’s building in Fort Worth, Texas.

The risk is that this boom in electrical-equipment spending isn’t as immune to economic shifts as the companies argue. Factory automation investments were meant to be on the path of unwavering growth, but orders for this business took a sharp U-turn in the most recent quarter at companies including ABB Ltd., Emerson Electric Co. and Rockwell Automation Inc. Barclays Plc analyst Julian Mitchell points out that demand for electrical equipment has been more sluggish in recent months outside of data centers. Technology companies including Meta Platforms Inc. are also rejiggering their capital spending plans to pivot to a new more cost-efficient data-center architecture that can support both AI and non-AI workloads. “It is debatable if having fewer units as a result of greater efficiencies would result in a greater amount of content in the data center for” electrical-equipment suppliers, Mitchell wrote in a June 9 report. The industry’s aggressive manufacturing capacity expansion increases the risk of whiplash if demand doesn’t turn out to be as robust as expected, says Melius Research analyst Scott Davis. He estimates that the $735 million worth of investments that Eaton has announced in North America electrical equipment production is equivalent to what the company has spent in the previous five years combined.

Losers

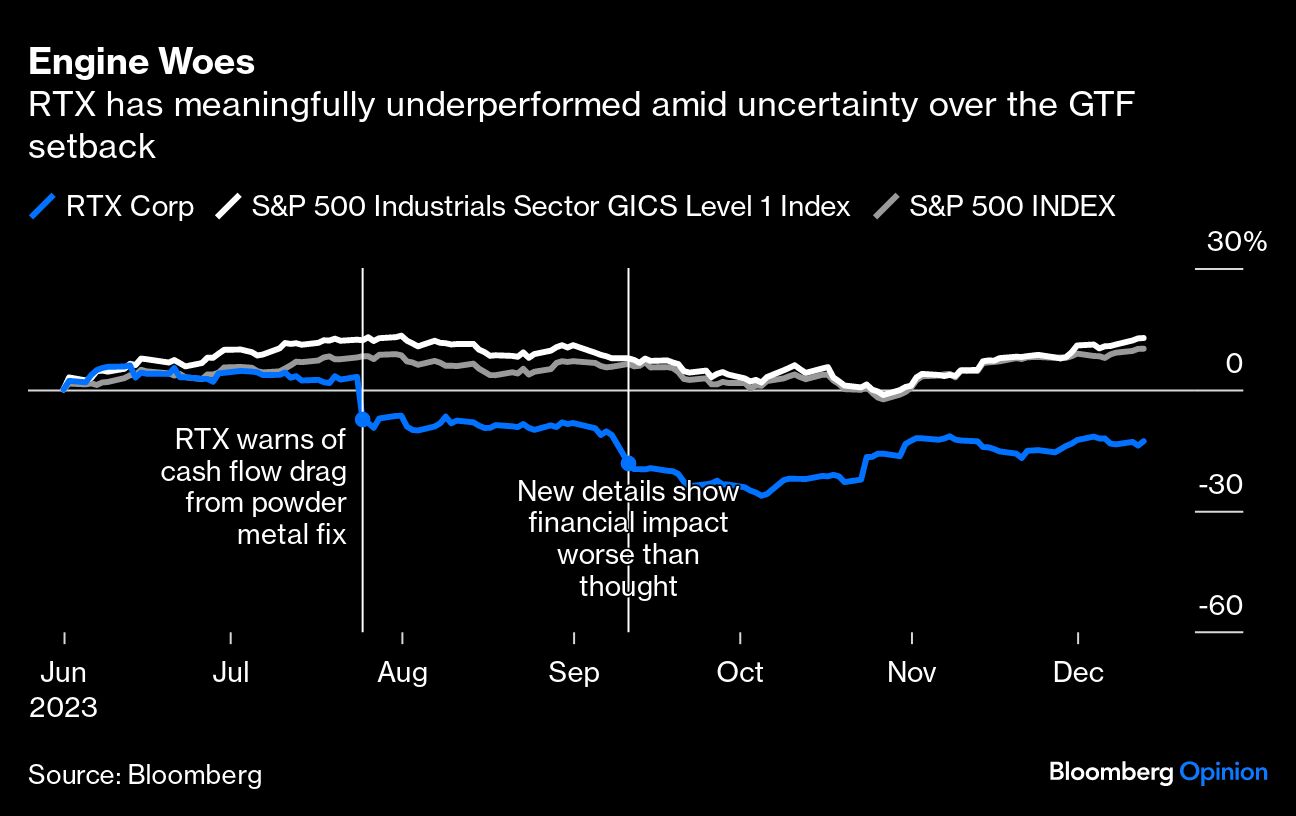

RTX Corp.’s recall of its GTF engine could widen the market share advantage for the Leap model produced by CFM. Even before this latest uqality control blunder came to a head, some 10% of the GTF fleet was grounded as of June amid supply-chain constraints and other durability issues that affect the engine’s time on the wing, particularly in hot and dusty climates. That number is ballooning as more and more engines are hauled in for accelerated and enhanced inspections. The GTF engines affected by the most recent glitch were made between late 2015 and the third quarter of 2021, when the company rooted out the source of microscopic contaminants that can shorten the lifespan of discs on the high-pressure turbine, one of the most important and expensive parts of the engine. RTX has pegged the total cost of the recall at $6 billion to $7 billion, the majority of which represents compensation to affected airlines and some of which it intends to pawn off on its GTF partners, including MTU Aero Engines AG. The recall has proved particularly disruptive to Spirit Airlines Inc., the largest operator of GTF-powered Airbus jets in the US, and Hawaiian Holdings Inc., which relies on the engine for a third of its fleet.

Airlines purchasing 737 Max jets from Boeing Co. have only one engine option: the Leap. But those purchasing Airbus’s A320neo models can choose between the Leap or the GTF. Even before the GTF’s latest problem, the Leap had a more than 70% win rate on new orders for the A320neo placed since the beginning of 2021, Melius Research analyst Robert Spingarn has said. RTX announced a $10 billion accelerated buyback in October in a bid to prop up its faltering share price. That helped, but the stock is still down nearly 20% for the year when other aerospace stocks are in high demand. No news is good news as far as the GTF is concerned, but it will take a while for investors — and airline customers — to be fully convinced there aren’t yet more “teething issues” yet to come for the engine.

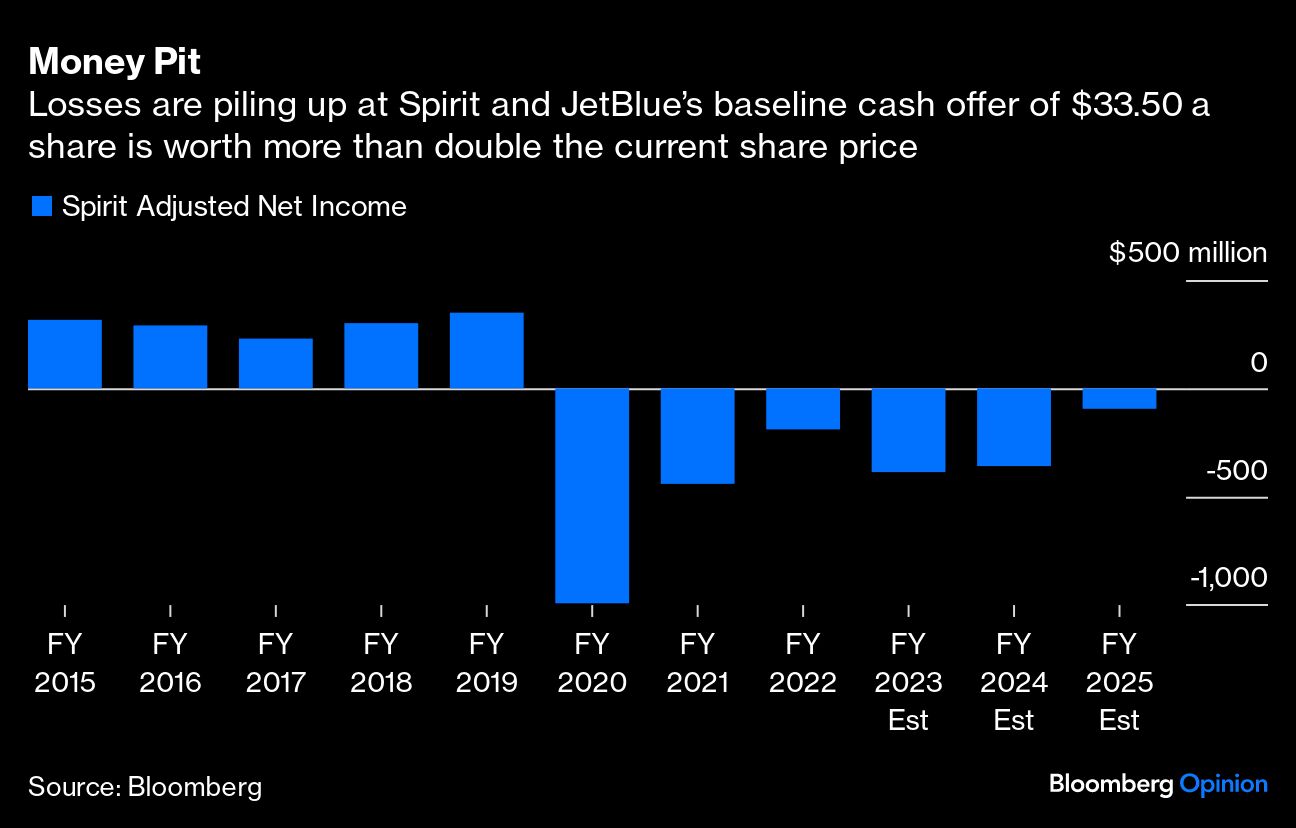

JetBlue Airways Corp. is still waiting to find out whether a US district judge in Boston will side with the Justice Department’s attempt to block its $7.6 billion takeover of Spirit Airlines or allow the deal to go through. The airline remains committed to the transaction, so theoretically a ruling in its favor would be a victory. It might not feel that way to shareholders, however. JetBlue rallied last week after the airline boosted its financial outlook for 2023 because of better-than-expected booking activity, but what this means in practice is that the carrier will lose slightly less money this year than it had previously thought. Spirit, meanwhile, is on track for its fourth consecutive annual loss this year, and analysts don’t expect it to turn a profit again before 2026 at the earliest. The travel recovery is running out of momentum domestically, and fares have been under pressure even as weather and air-traffic control disruptions, stubborn supply-chain logjams and higher fuel and labor expenses push up operating costs.

Airlines are cutting back on flights, particularly in the already seasonally weak first quarter, to try to better match supply with demand. Southwest Airlines Co. said on Friday that it’s now aiming for a low- to mid-single-digit capacity increase in 2024, compared with a previous target of mid-single-digit growth. In short, the accelerated growth that JetBlue was chasing when it first announced an offer for Spirit in April 2022 makes a lot less strategic sense today — particularly at the kind of price tag the airline had to dangle to wrest Spirit away from Frontier Group Holdings Inc. and with the kind of debt load it has to take on to pull off the purchase.

Most Improved

3M Co. started the year as a black box of liabilities, and it’s ending the year as more of a gray box of liabilities. In June, the company announced a deal to pay as much as $12.5 billion over 13 years to test and treat drinking water supplies that have been polluted with any level of per- and polyfluoroalkyl substances (PFAS), which are known as “forever chemicals” because they break down slowly in the environment and can accumulate in the body and cause health problems. The company in August announced a separate $6 billion cash and stock settlement to resolve claims that it knowingly sold defective earplugs that left US military service members with hearing loss and tinnitus.

It will likely take additional multibillion-dollar settlements before 3M can truly put its legal woes behind it. The pending PFAS settlement is specific to drinking water claims by public US water systems. Other remaining outstanding items could include claims from state attorneys general, the federal Environmental Protection Agency and US military, foreign governments such as Belgium and the Netherlands, personal injury and property lawsuits from the broader population, the cost of cleaning up areas near 3M’s legacy PFAS manufacturing sites and legal action from commercial and industrial customers that the company supplied with PFAS. Wastewater utilities may also require a separate payout. All told, Barclays’ Mitchell estimates there are an additional $16 billion of potential PFAS liabilities for 3M that are yet to be resolved. 3M is a so-called dividend aristocrat — it has paid dividends without interruption for more than a century and has raised the shareholder payout annually for more than 60 consecutive years. Resolving its myriad legal sideshows may cost the company that status. But that may be a price worth paying if 3M can get back to focusing on its actual business of making adhesives, roofing granules, electronic components and other industrial goods.

The company is also tackling the lackluster operational performance that made the legal uncertainty all the more painful. 3M in April announced a sweeping restructuring program that will save the company as much as $900 million annually and result in 8,500 job cuts. This is the latest in a long string of restructuring programs at 3M, but for once the cost cuts appear to be showing up in the bottom line. 3M reported better-than-expected earnings in the third quarter and raised its full year guidance even as sales fell 3.1% on an adjusted and organic basis in the period.

Chart of the Week

Dave Calhoun’s reign at Boeing may be nearing its final stretch. The planemaker this week announced that Stephanie Pope, the head of its services arm, will become chief operating officer. The position is often considered a steppingstone and sets Pope up to eventually succeed Calhoun when he retires. The last person to officially hold the COO job at Boeing was former CEO Dennis Muilenburg, who was ousted in late 2019 after two fatal crashes prompted a prolonged global grounding of the best-selling 737 Max jet and tough questions about the company’s culture. Calhoun, a longtime Boeing board member and a former GE executive, succeeded Muilenburg in early 2020 and helped stabilize a company that was soon reeling from not one but two crises as the pandemic obliterated demand for air travel. Calhoun is 66, and Boeing’s board has already tweaked its retirement policy to allow him to stay in the role longer. Calhoun intends to run the company for at least one more year, the Wall Street Journal reported.

Pope has worked at Boeing for nearly three decades, including serving as chief financial officer for the commercial airplanes division. She’s immensely qualified for the top job. If appointed, Pope would also be the first female CEO at Boeing and only the eighth among companies on the S&P 500 Industrial Index. Still, it’s surprising that Boeing again looks set to tap a veteran insider for the CEO role. Boeing has gone from dumpster fire to the occasional smoldering embers under Calhoun’s watch, but it hasn’t been the smoothest journey. Supply-chain logjams and quality-control issues have stymied jet deliveries, and charges continue to pile up in the defense division. Airbus has notably widened its market share advantage in the narrow-body jet market — a competitive dynamic that Boeing’s next CEO will have to find a way to address while managing a debt load that now sits at more than $50 billion. There’s something to be said for fresh eyes.

Deals, Activists and Corporate Governance

EQT AB, the Swedish investment firm, agreed to purchase a majority position in industrial waste-management company Heritage Environmental Services. Just about every manufacturing process, from steelmaking to semiconductor and electric vehicle production, involves waste that’s hazardous to the environment or to human health. It’s Heritage’s job to process this waste properly and safely. Terms of the deal weren’t disclosed. The company is based in Indianapolis and operates 37 facilities in the US that handle about 660,000 tons of waste a year. The amount of regulated specialty and hazardous waste coming out of US factories and other industrial sites exceeds the sector’s current processing capacity by several hundred thousand tons each year — and that’s before accounting for a revitalization of domestic supply chains or stimulus-backed investments in chips and the energy transition, Juan Diego Vargas, a partner within the EQT infrastructure advisory team, said in an interview. Should the Environmental Protection Agency officially designate certain per- and polyfluoroalkyl substances, or PFAS, as hazardous materials under the federal Superfund law, then the cleanup work for industrial sites that used these chemicals in legacy manufacturing would also fall to companies like Heritage.

No company has attempted to build a facility like those run by Heritage in 30 years because the permitting process is so challenging, he said. Communities aren’t exactly falling all over themselves to welcome investments for plants that manage hazardous waste, either. EQT plans to expand Heritage’s capacity by increasing the throughput at its existing facilities and then buying other plants to help fill out a national network, Vargas said. Heritage currently recycles and recaptures about 20% of the waste it processes to create an engineered fuel that can be used by cement and lime kilns in place of coal or natural gas, and EQT plans to “supercharge” this part of the business, Vargas said.

L3Harris Technologies Inc. struck a deal with activist investor D.E. Shaw to refresh its board, tweak its executive compensation formulas and review the company’s “operational performance, cost structure, portfolio composition and all available value creation levers.” Kirk Hachigian, the former CEO of door manufacturer Jeld-Wen Holding Inc., and Bill Swanson, a former CEO of Raytheon Co., will join the L3Harris board effective immediately and then the directors and D.E. Shaw will agree on a third, independent candidate to join the ranks in 2024. Former L3Harris CEO Bill Brown will serve as a special adviser for the business review process. Separately this week, Kenneth Bedingfield, the former CFO of Northrop Grumman Corp., officially took on that job at L3Harris. He succeeded Michelle Turner, who stepped down after less than two years in the role. Turner’s departure was not prompted by any disagreement with the company’s financial reporting or accounting practices, procedures or decisions, L3Harris said.

Terran Orbital Corp., the satellite maker that went public in 2021 through a merger with a blank-check firm and whose shares have languished ever since, said it’s exploring strategic alternatives including a possible sale. Terran is seeking bids by the end of the month and has attracted interest from potential strategic and financial buyers in the US and Europe, the Wall Street Journal reported, citing people involved in the process. Lockheed Martin Corp. has a stake in the company and partners with it on satellite manufacturing but isn’t expected to bid. Separately, Terran Orbital’s CEO Marc Bell reportedly told employees that the company is looking for strategic investors, not a buyer, and that he would be involved in any take-private deal.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Brooke Sutherland