In the past five years, US ETF market assets have more than doubled, over 1,000 new funds launched, and annual trading volumes jumped by around $11 trillion. Yet there has been one exception to the explosive growth: The ranks of firms responsible for steering cash in and out of every product.

This cohort — known as authorized participants, or APs — are a type of broker-dealer indispensable to the smooth functioning of every exchange-traded fund in North America. But as the industry has swollen, their numbers have barely changed. In fact, the most active APs have been increasing their market share, strengthening a remarkable concentration in the underbelly of the now-$8 trillion arena.

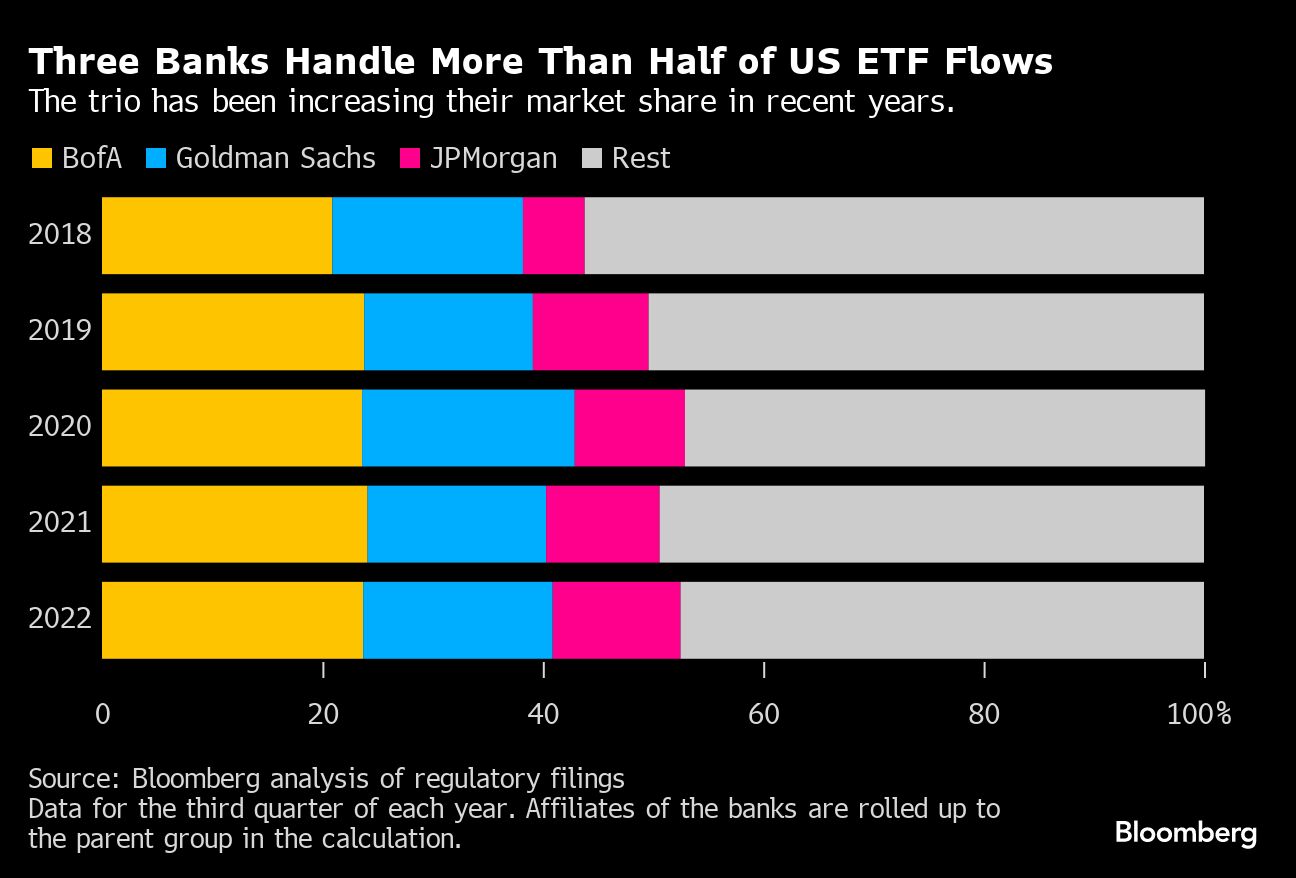

Bloomberg News analyzed filings for more than 3,400 funds to show that, despite the industry’s breakneck expansion, more than half of all US ETF flows are handled by just three firms. For a majority of funds, more than 90% of all money entering or exiting funnels through three APs or fewer. Hundreds of ETFs reported only one active AP in the latest quarter for which full data is available, meaning they depended on a single firm to keep cash moving.

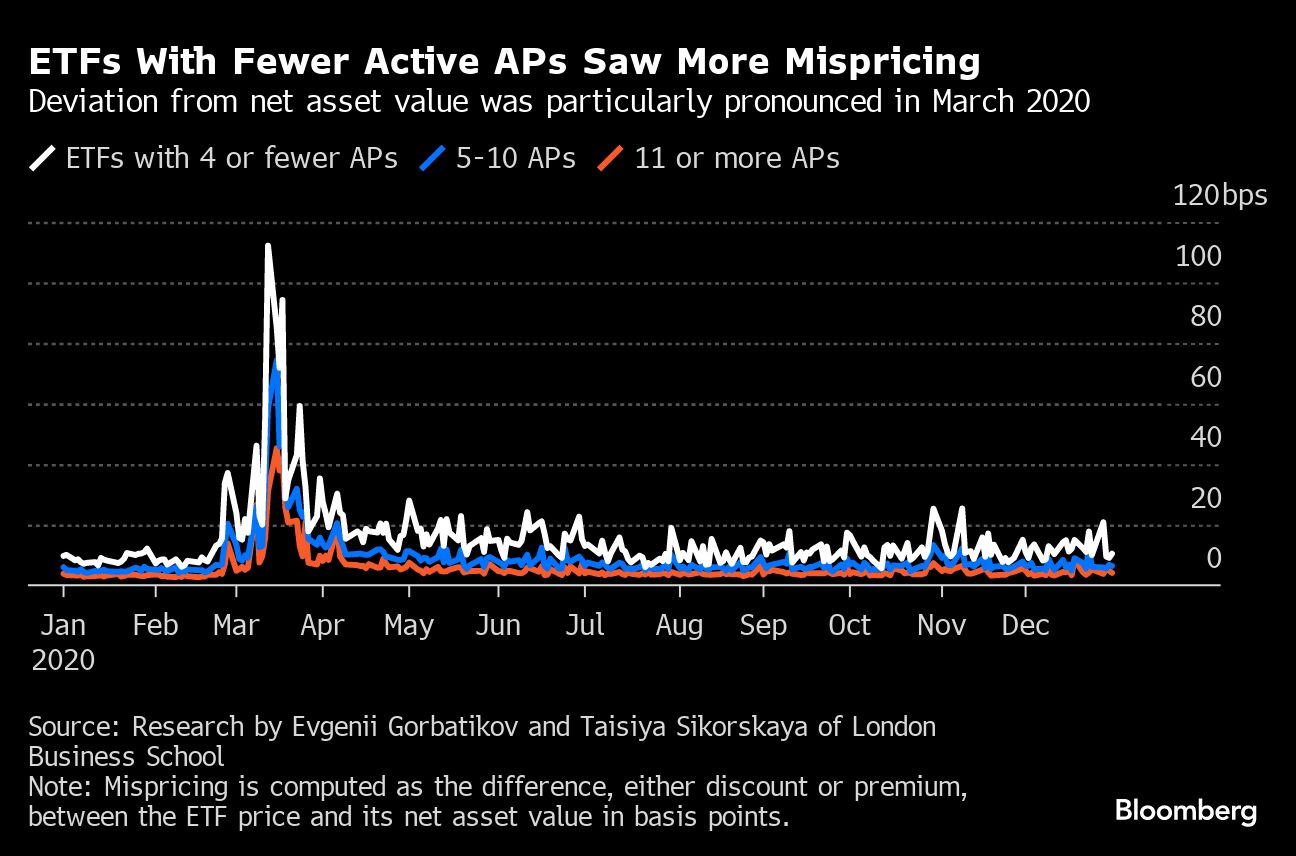

Funds with fewer active APs are prone to greater mispricing in stress scenarios, research shows. Mispricing — when an ETF trades at a premium or a discount to the value of the assets it holds — creates extra risk and potentially higher costs for investors. It also undermines the reliable functioning of one of Wall Street’s most popular investment vehicles.

“Our message is that investors and retail traders have to be aware of this,” said Taisiya Sikorskaya, a PhD candidate at London Business School who co-authored Two APs Are Better Than One: ETF Mispricing and Primary Market Participation. “This mispricing that we find exists exactly in times when investors would like to rebalance, would like to fly to safety.”

For most retail traders, the mispricing may not be immediately apparent since AP activity and a fund’s deviations from its assets often happen out of most investors’ sight. ETFs have become popular in part because they’re considered low-cost and efficient, yet in a market meltdown these attributes can fade — and a lack of APs exacerbates the problem.

The Big Three

APs close price dislocations by either giving the ETF more assets in exchange for newly created shares, or by buying existing shares in the market and redeeming them in return for assets from the fund.

A trio of major banks have emerged as dominant players in the AP business, Bloomberg’s analysis of Securities and Exchange Commission filings shows. Bank of America Corp. leads the pack, reigning as the most-active AP in every period since the data was first reported. As of the third quarter of 2022 — the last for which full data is available — it commanded 24% of the entire market. Goldman Sachs Group Inc. is second with about 17%, while JPMorgan Chase & Co. is in third place with nearly 12%.

“They have the ease and expertise: being able to move cash, being able to settle trades, and getting it all done in a certain amount of time,” said David Graichen, head of capital markets at WisdomTree. “That enables them to continue to thrive in this business.”

Representatives for Goldman Sachs and JPMorgan declined to comment. BofA didn’t respond to requests for comment.

A typical ETF had 22 APs registered as of 2022, while the average number of active APs was just 4.3, the analysis showed. In the entire five-year period, a total of 62 firms registered as APs at one time or another; 28 of them didn’t conduct creations or redemptions at all.

To stay efficient, funds contract multiple APs, and if any step away the assumption is another will take its place when the economics look right. Since APs aren’t obliged to fulfill the arbitrage role, many funds rely on the willingness of just a few firms to keep performing the function.

The filings span a period that featured multiple bull and bear markets, including the Covid crash and the stimulus-fueled recovery. The SEC introduced these annual disclosures a few years ago because it was concerned about limited information regarding ETFs’ reliance on APs. A representative for the SEC declined to comment.

True Depth

The disclosures don’t necessarily present a complete picture of the inner workings of the ETF ecosystem. Major banks often act as prime brokers, meaning they can create and redeem shares on behalf of other liquidity providers like market makers for a fee.

To Samara Cohen of BlackRock Inc., the efficiency of an ETF and how tightly it prices to its underlying assets is a function of the effective arbitrage of these unseen liquidity providers, rather than that of the AP. “We have a much more diverse ecosystem today than we did five years ago as a result of those larger banks really integrating ETF capabilities in their dealing desks,” said Cohen, chief investment officer of ETF and index investments at the world’s largest asset manager.

While the data showed the big three APs handle a majority of fund flows, in reality, dozens of other firms may be moving assets with a registered AP’s help. The Vanguard Total Bond Market ETF (BND) is the largest US fixed-income ETF with around $103 billion in assets, yet the data suggest just three APs handled 98% of its flows. Vanguard declined to confirm whether some APs act as prime brokers for BND, but said “many market makers in Vanguard ETFs do not serve as Authorized Participants.”

Even though bigger APs continue to dominate, nontraditional players are making strides in the arena. Firms like Virtu Financial Inc., Citadel Securities LLC, Hudson River Trading and Jane Street have made significant gains in AP market share in recent years, the data show, including by stepping in as liquidity providers during the Covid crash.

Several of these firms have always had a strong presence market-making and trading ETFs, but they frequently manage positions through other channels such as borrowing or lending securities. They use creation and redemption when the costs make sense.

Representatives for Virtu and Citadel declined to comment. Hudson River and Jane Street didn’t respond to emails requesting comment.

Remembering how ETFs fared during the throes of the pandemic in 2020 may also alleviate some worries about mispricing. When underlying fixed-income markets froze, ETF shares kept trading — providing vehicles of price discovery and a mechanism for transferring bond risk despite the seizure.

Nevertheless, these caveats don’t dispel all concentration concerns. Sikorskaya, formerly of Deutsche Bank AG’s ETF arm, and co-author Evgenii Gorbatikov, a London Business School PhD, argue even the largest banks can face regulatory constraints or liquidity challenges at a time of turmoil. Under regulations introduced in the wake of the financial crisis, big banks haven’t been able to take much risk, raising the chances they could scale down their AP role when their services are needed most.

The researchers studied when the prices of equity ETFs diverged from the value of their assets and related it to each product’s AP connections. When they compared the average mispricing of the third of funds with the fewest APs against the third with the most during the Covid selloff, they recorded a more than 50 basis-point bigger deviation in the former.

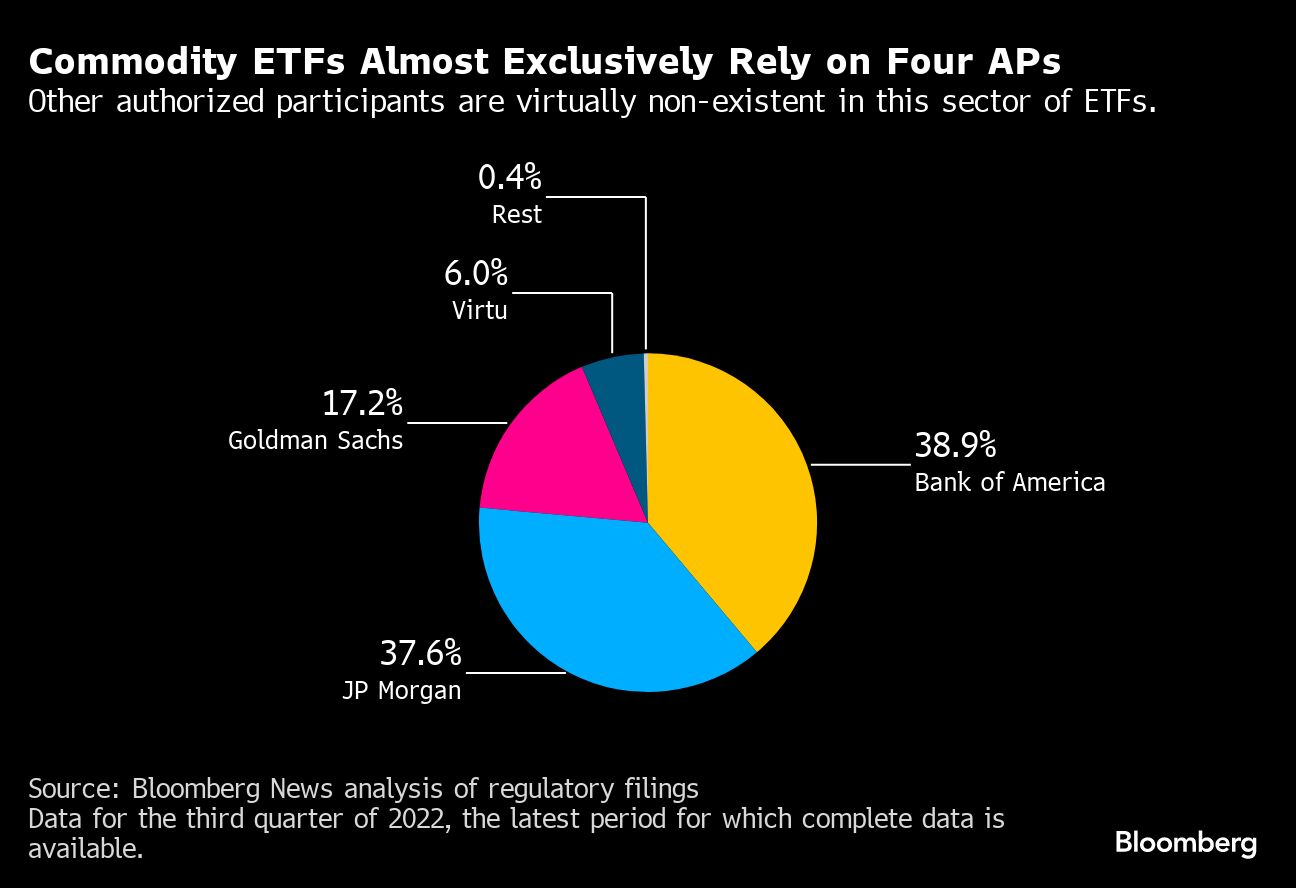

The AP-concentration effect was evident even when controlling for general turnover or liquidity of a fund, meaning the mispricing wasn’t bigger because of other characteristics of the ETFs. The duo expect dislocations of “much larger magnitudes” for fixed-income or commodity ETFs because these are less liquid and more concentrated parts of the market, Sikorskaya said.

Bloomberg’s analysis showed that commodity ETFs display some of the highest levels of AP concentration. Four firms handled almost all the flows in and out of these products during the third quarter of 2022, with Virtu edging in to join the three banks. The narrow participation is likely a reflection of the challenges of working in an asset class prone to heightened volatility and liquidity mismatches between ETFs and their physical holdings. Futures-based trading adds complexity.

Overall, more than 280 ETFs recorded just a single active AP in the third quarter of 2022. For the most part, these are newer funds with extremely low trading activity — there’s not much need for creation and redemption if there are no flows. But the largest was the $2 billion JPMorgan BetaBuilders U.S. Aggregate Bond ETF (BBAG), underscoring that even established products can be heavily dependent on as few as just one name.

“If something does happen again, are other APs going to step in?” said Bloomberg Intelligence ETF Analyst Athanasios Psarofagis, referring to the next market crisis. “You know, we like to think that they will, and hopefully that they will. But I don’t know if we have enough data to say, ‘Oh yeah, this will definitely happen.’”

Methodology:

Bloomberg News analyzed bulk data of N-CEN filings released by the Securities and Exchange Commission, updated on Sept. 30, 2023. This type of regulatory filing, on which details of ETF funds are disclosed, is submitted annually by registered investment companies in the US.

As fiscal calendars vary across different ETF operators, this analysis converted the annual data into quarterly to better display trends over time.

Financial firms may have numerous affiliates working as separately reported authorized-participant entities. They have been matched back to their parent entity so that the activity levels of the groups can be measured.

When filings are amended, the most recent versions are included in the analysis.

When discussing AP activities, this analysis combined the ETF share creation and redemption flows to track the combined volumes. An AP that has handled at least $1 worth of transactions is considered an active AP for that ETF during the fiscal year. The investment strategy and AUM details of ETFs were sourced from data compiled by Bloomberg.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our full schedule of upcoming CE-approved virtual events.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

More ETF Topics >