Equity Market Concentration and the AI Revolution

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

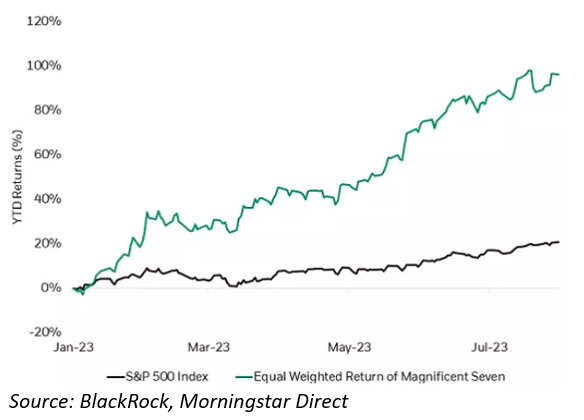

The rise of market giants

Equity-market concentration has been a topic of growing concern. The seven mega-cap tech giants, Apple, Microsoft, Amazon, Nvidia, Alphabet, Meta Platforms, and Tesla, have dominated the performance of the global stock market. There has been so much hype around those companies that they have commonly been referred to as the “magnificent seven,” the largest U.S. companies by market capitalization.

The performance of those stocks has been predominant, contributing nearly 65% of S&P 500 returns, through July, from just ~28% of the S&P 500 Index. This means that most of the other 493 stocks in the index are underperforming. A driving factor of strong performance in 2023 has been the latest boom in artificial intelligence (AI), bolstering the success of those high-growth stocks.

Impact on diversification

Why does this matter and why should investors care if the market is concentrated? Many indices are market-capitalization weighted, meaning that the larger a stock’s size, the larger its share of the overall index. As these companies become a larger portion of the global stock market, they have a bigger impact on overall returns, which could lead to greater portfolio risk. The concentration of market returns in just a few mega-cap stocks, dominated by the information technology and communication services sectors, could lead to heightened volatility, reduced diversification, and increased systematic risk for investors.

Those companies are more alike than different and are, in various ways, exposed to the same secular trends. Consider AI, cloud technology, augmented/virtual reality, and autonomous vehicles as examples. This overlap increases the systematic risk of owning these stocks within an index or portfolio, as these companies generate a large portion of their revenues and future expected returns from similar risk factors, diminishing diversification and its related benefits.

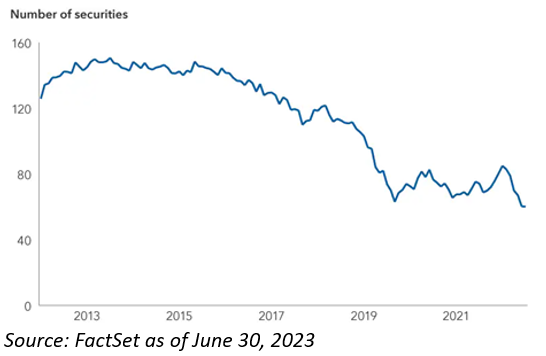

We have seen a significant decrease in the effective number of securities in the S&P 500 index, as measured by the Herfindahl-Hirschman Index (HHI). The HHI measures how many securities it would take to create an equally weighted portfolio with the same level of diversification as the S&P 500 index. This figure is at its lowest level in recent history, which means the index is at its lowest level of diversification.

An overly concentrated market can also have a significant impact on active management and stock selection, as narrow leadership can be challenging for managers and strategies that favor greater breadth. When considering the magnificent seven, there is significant factor exposure to quality and momentum and negative exposure to size (small companies) and value (inexpensive companies), which has a big impact on the overall index.

Influence of AI on future returns

AI hype hit an all-time high in 2023. A lot of this can be attributed to the belief that it is more than just a new market and, rather, is a foundational technology by which other markets will be created. Investors are expecting that the productivity increase realized from AI could drive macroeconomic growth for years to come.

AI will likely have a sustained, significant impact on market returns over the next decade and beyond, as economic growth is primarily driven by three main factors: capital, labor, and technological advancement. Many countries and geographic regions are experiencing decreased labor and capital growth. A growing portion of future economic growth will come from technological advancement, and specifically AI. According to a recent study by McKinsey & Company, generative AI can deliver significant economic benefits, adding between $2.6 and $4.4 trillion in global corporate profits annually1.

At a micro level, we are approaching AI-based investments with cautious optimism, as it often takes time to see meaningful adoption when it comes to disruptive technology. This is likely a major competitive advantage for early adopters, primarily the magnificent seven, who have spent billions of dollars building out their technology and have expansive customer bases to tap. While there will be several new entrants and disruptors over time, it will likely take years to see meaningful market penetration.

How to mitigate concentration risks

Investors can reduce the inherent, overall risks in their portfolio by incorporating key best practices. Within the overall equity allocation, exposure to different investment styles (value and growth) as well as different-sized companies (large cap, mid cap, and small cap) can reduce portfolio volatility by achieving broader diversification away from the largest names in the stock market. Beyond style and size, diversification outside of the United States provides exposure to investment trends and the economics in other growing parts of the world. Additionally, employing a prudent rebalancing process helps ensure that investors do not get overly concentrated in any particular asset class or style box.

Because of the robust performance of the magnificent seven, portfolios have generally become overweight to large-cap stocks, resulting in an underweight to small- and mid-cap stocks, as well as international equities. Rebalancing portfolios back to target weights reduces risk and prevents overexposure to high-performing assets, ensuring the portfolio remains consistent with the investors long-term risk and return objective.

Steven Fraley, CFA, MBA, is principal and director at Innovest, and provides consulting services to families. Steven is a member of the investment committee, which drives the firm’s investment-related research. He is a member of the due diligence group, responsible for independently sourcing investment managers. Steven is also the director of capital markets research group, responsible for monitoring the global macro-economic environment. https://www.innovestinc.com/steven-fraley

Brett Minnick, CFA, is a vice president and consultant at Innovest. Brett provides consulting services to Innovest’s retirement plan, nonprofit, and family clients. Brett is a member of the capital markets research group, responsible for monitoring the global macro-economic environment, asset allocation modeling, and portfolio construction. Brett leads the due diligence group, responsible for sourcing investment managers, conducting qualitative analysis regarding performance, understanding return attribution, and meeting management teams both at Innovest and at their offices. The group works in conjunction with Innovest’s investment committee, of which Brett is also a member. The investment committee drives the firm’s related research and due diligence. Brett holds the Chartered Financial Analyst (CFA) designation. https://www.innovestinc.com/brett-minnick

Innovest Portfolio Solutions LLC is a Denver-based investment consulting firm. More information on Innovest can be found at www.innovestinc.com.

1 McKinsey & Company. (2023, August 25). What is the future of generative AI? An early view in 15 charts. Retrieved from https://www.mckinsey.com/featured-insights/mckinsey-explainers/whats-the-future-of-generative-ai-an-early-view-in-15-charts

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All