It sounded quixotic, and so it proved. Activist investor Jeff Ubben is winding down his social and environmental impact funds, a project that sought to harness capitalism for the simultaneous benefit of society and shareholders.

The failure points to some uncomfortable truths about the modern stock market and the staying power of even well-meaning investors.

Ubben came to prominence through ValueAct Capital, an investment firm that takes large, long-term stakes in companies and tries to work alongside management rather than getting into bitter public fights. His most recent venture, Inclusive Capital Partners, took that approach and added an environmental mission. It was born from the conviction that conventional environmental, social and governance (ESG) investing is flawed and requires a new strategy.

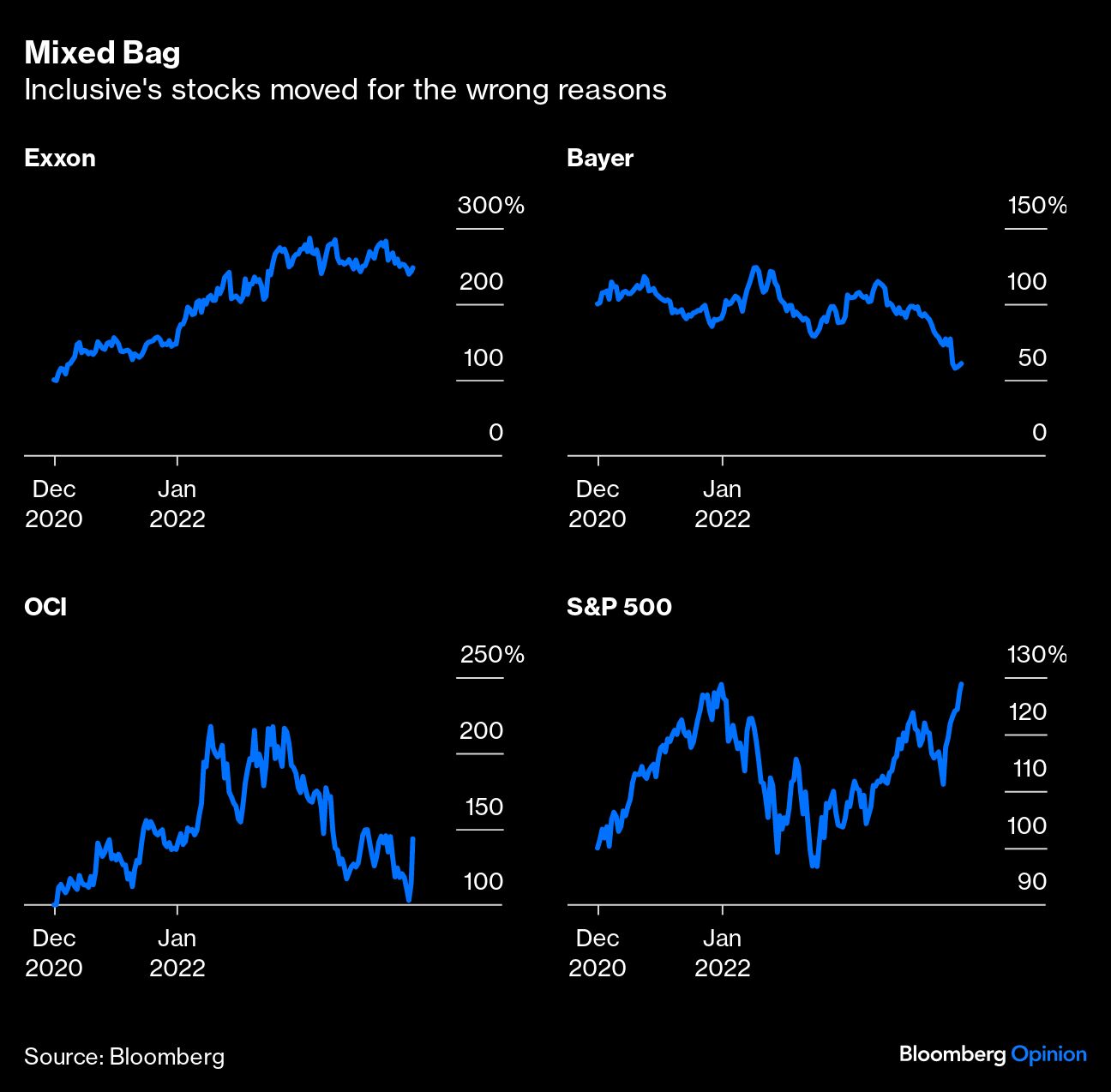

The Inclusive portfolio included companies that don’t look very ESG at all — oil major Exxon Mobil Corp. and Bayer AG, the purveyor of pesticides and genetically modified seeds, as well as Dutch chemicals firm OCI NV.

There was a pragmatic ethical and financial thesis underpinning the choices. A growing population will demand more energy, more food and more materials. Rather than pretend this isn’t the case, Ubben focused on companies that could meet the need while also working to reduce the environmental side effects. So Exxon is investing in carbon capture and storage. Genetic engineering can help lower the need for toxic chemicals in agriculture and make farming more efficient. OCI specializes in fertilizers and low-carbon fuel alternatives. And so on.

Where such companies were excluded from ESG funds, the resulting valuation discount just reinforced their appeal. “Canceled” firms might yet command premium stock-market valuations if the market eventually applauds emissions-busting work, so the argument went. Inclusive aimed to push the management teams to invest further and faster and make the inherent value of their assets visible through spinoffs or asset sales.

The thinking was that the market would push up the shares and therefore lower these firms’ cost of capital. And by making the raw material of finance cheaper, capitalism would positively reinforce investment in carbon-bashing technologies.

It’s hard to fault Ubben for trying a radical break with conventional ESG. If you simply avoid investments in dirty companies, you lose the ability to influence strategy. Moreover, it’s possible to construct a portfolio of stocks with high ESG scores that aren’t in the business of cutting carbon. The tech firms dominating the S&P 500 are also often core holdings of ESG funds — never mind the carbon footprint of the data centers storing all those undeleted emails and duplicate photos in the cloud. An ESG-branded fund that mirrors the market’s sector weightings with a few adjustments for individual companies isn’t doing much to push hard dollars into energy-transition technologies.

But Inclusive’s alternative approach was flawed too. The stock market is generally skeptical of corporate capital expenditure until the investment is on the verge of producing certain cash flow. That applies across all sectors, from high-speed broadband networks to blue-skies drug development. True, some clean-energy businesses like electric-vehicle makers have attracted legions of investors. But that looks more herd behavior than a calculated attempt to support the energy transition.

The market is cold-blooded, short-termist and faddist. Where companies generate value for society, there needs to be a clear link to earnings for this to become a financial benefit for shareholders. Tax or regulation may be required for a corporation to profit from environmental technologies. As Victoria Kalb, head of ESG and sustainability research at UBS Group AG, says, markets aren’t necessarily designed — or able — to solve critical sustainability issues in isolation.

It could be years before Exxon’s low-carbon business is priced into its market capitalization. Meanwhile, no listed firm gets a pass on the things that put off investors. Bayer is facing ongoing lawsuits around its glyphosate herbicides — a hard-to-value risk. OCI is a complex business, and it’s historically struggled to get investors to understand its moving parts. And the rise in interest rates over the past two years makes distant earnings less valuable in today’s money — whether from carbon capture or anything else.

Exxon has outperformed lately simply because of demand for oil. Bayer has nearly halved in value since April on disappointments in its pharma pipeline and continued bad news on litigation. This month, OCI is up more than 30% after it agreed to some $7.2 billion of disposals, but that's merely brought the stock back to its level just before Ubben's engagement emerged in March. There were more serious misadventures too — like EV maker Nikola Corp., whose founder was convicted of fraud.

Which brings us to the truths about fund management. You may be able to pull investors in with an unconventional investment strategy based on a mission to save the planet. But to keep them on board, you still need to deliver returns. Inclusive wrote to clients acknowledging that many would "have likely lost confidence.”

Real ESG should be about allocating capital to companies that will develop solutions to cutting carbon emissions — that is true. But it’s sadly naive to imagine that a market dominated by passive funds, computer-generated flows and active funds worried about quarterly performance will on its own solve knotty real-world problems.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.