I wrote last week about how interest rate cuts in 2024 should boost cyclical areas of the economy that were already set to rebound, lifting economic growth. The bond market’s subsequent response to some noisy labor market data shows it’s worth considering how the Federal Reserve would respond if a different scenario played out.

Regardless of which outcome we end up getting, the slow-and-steady pace of policy easing currently priced by markets is likely to be wrong. The world in which the fed funds rate is more than 100 basis points lower by the end of the year is one where we can expect at least one outsized 50 basis-point cut, and probably relatively early in the cycle.

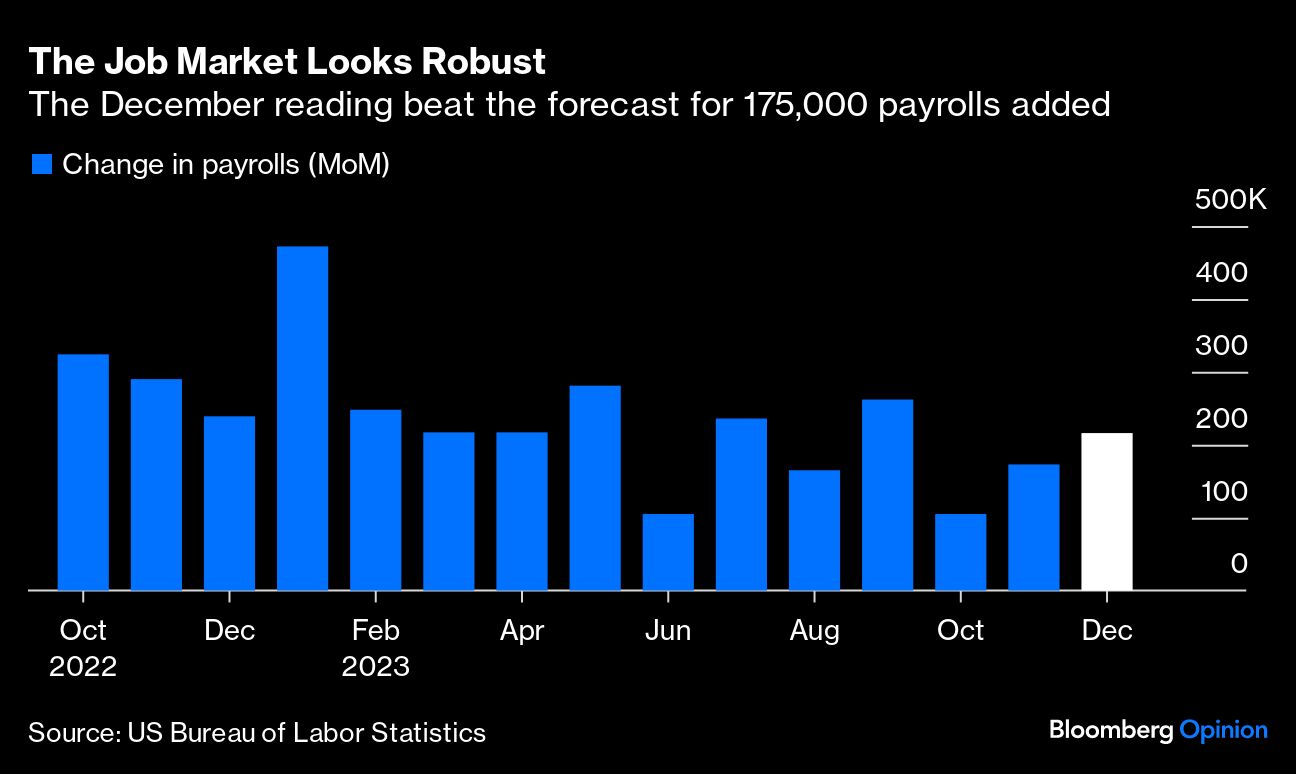

The glass-half-full interpretation of last week’s labor market data is straightforward. Jobless claims remain benign, perhaps even suggesting modest improvement with the number of people currently collecting unemployment benefits stabilizing after a concerning rise in the first half of 2023. And Friday’s payrolls report showed 216,000 jobs were created in December, with the unemployment rate remaining steady at 3.7%.

But there were some ominous signals as well. The rate at which companies hired workers, which has been trending lower through 2023, fell again in November. The total hours that Americans worked declined between November and December. And the employment component of a closely followed survey of the service sector was surprisingly weak, coming in at levels that we haven’t seen outside of the pandemic and the financial crisis.

Every little wiggle in the labor market matters because of how much price pressures have abated. Year-over-year inflation remains somewhat high because of a few elevated monthly readings from early 2023 that haven’t fallen out of the calculation yet. On a six-month annualized basis, the central bank’s preferred measure of inflation is now at a below-target 1.9%. This data alone supports rate cuts this year, which the Fed has already acknowledged.

But how much and how soon are now the big questions. Policymakers continue to say that they expect the fed funds rate will be around 2.5% in an unspecified longer run, assuming a balanced labor market and inflation at their 2% goal. That implies an inflation-adjusted, or real, interest rate of 0.5%.

If we assume inflation has sustainably returned to the Fed’s target, the real policy rate is currently north of 3%, far above its pre-pandemic level in 2019 and the central bank’s longer-run forecast. That no longer makes sense given the state of inflation and the labor market, both of which continue to slow.

It’s possible the Fed cuts a few times — the median estimate from policymakers is for three moves this year — spurring activity in areas such as housing, and we continue along this merry soft-landing path.

Clear signs of a bigger hiccup in the job market — hints of which were in last week’s data — and the Fed’s mentality would shift rapidly from a few tactical cuts to a more aggressive defense of the economy.

Chair Jerome Powell has shown that he’s not afraid to be bold when he has felt it was warranted. At the Fed’s December 2018 meeting, officials signaled 50 basis points of interest rate increases the following year; they ended up lowering by 75 basis points even with the unemployment rate continuing to fall. In March 2020, easing came at light speed. And once the Fed was convinced it had an inflation problem, rates shot up in 2022.

It’s that context we should keep in mind when thinking about the prospect of rate cuts this year. Markets are currently priced for roughly 150 basis points of reductions, beginning in March and fairly evenly distributed over seven meetings.

That type of gradual approach makes sense in a benign, tactical easing scenario (though it probably implies fewer than half-a-dozen cuts). It’s far too conservative in a more aggressive cycle, where the Fed feels it needs to defend the labor market based on the economic data, financial market volatility, or anecdotes from business contacts. Nothing in Powell’s tenure suggests that this is a central bank that would make small adjustments over the course of 10 months. If they’re worried about a deterioration in the economy, even if it’s not yet conclusive in the data, I’d look for 100 basis points of cuts by the July meeting, with at least one half-percentage-point reduction.

It would be unprecedented to get such a forceful easing without the economy already tipping into recession, but the Fed’s 2022 response to a surge in inflation was unprecedented, too. There’s no longer a need for real interest rates above 3%, policymakers just haven’t yet decided to pivot to a more normalized level. Once they do, look for the adjustment to be relatively speedy. Ignoring this scenario is where the greatest risk lies.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

More ETF Topics >