Seismic Bond Shift Has Traders Watching Yield Curve’s Moves

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsBond traders are growing convinced that US Treasury yields are on the brink of returning to the way they’ve traded for most of their existence — it’s the how, why and when of the normalization that keeps financial markets bouncing around.

The shift many investors bet is now underway would see the interest rate on 10-year Treasuries rise above those on US two-year notes, a steepening of the so-called yield curve that would mean banks and investors get rewarded for the risk of lending money for longer periods as is typical.

That’s a world away from last July, when two-year Treasury yields exceeded 10-year ones by more than a full percentage point. It was the sort of deeply inverted yield curve last seen in the early 1980s, a side effect of the Federal Reserve’s series of rate hikes aimed at fighting inflation. The campaign, it was feared, risked tipping the economy into recession.

Veteran investor Bill Gross, the co-founder of Pacific Investment Management Co., and Harley Bassman, a long-time bond expert who invented the MOVE Index of Treasury market volatility, are among those predicting that chapter will soon end.

What is the subject of fierce debate is what propels the pivot, and the answer means money for some and losses for others. If rate-cuts emerge as the economy slows then yields will shrink on the short-end, but if inflation remains a concern and the Fed stays on hold then 10-year yields will rise more in a higher-for-longer scenario.

“The question we are asking – given the wide range of outcomes – is what is that steeper yield curve?,” Kathryn Kaminski, chief research strategist at AlphaSimplex Group, said on Bloomberg Radio on Tuesday. “Is that going to be cuts on the short end or could it possibly be, unexpectedly, that we see weakness in long-term bonds and we have a longer time to wait for cuts – and we actually see a steepening from the long end.”

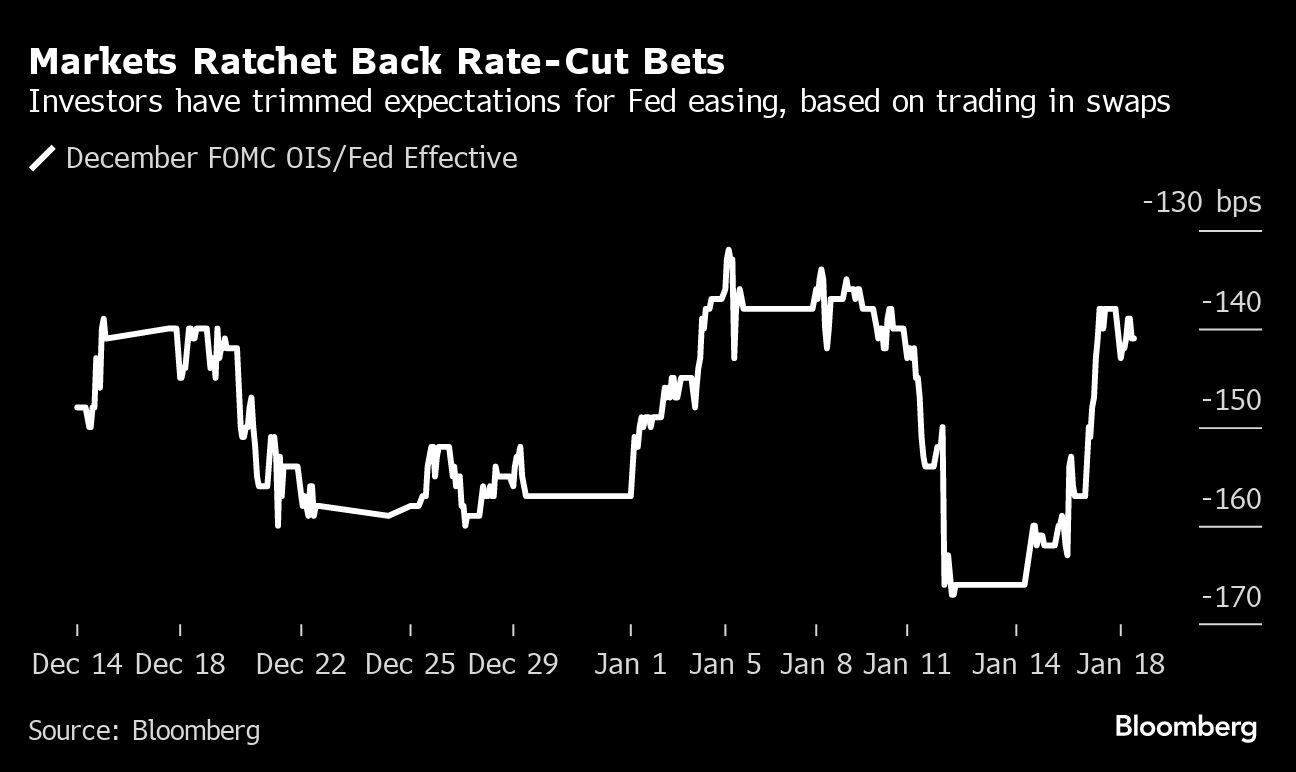

Key to how any steepening unfolds is the timing of Fed rate cuts. After central bankers signaled a shift toward easing late last year, investors ramped up rate-cut bets and piled into Fed-policy-sensitive two-year notes, driving yields to the lowest since May earlier this month and below yields on US 30-year bonds. Traders have since tempered their wagers as US economic data continued to show resilience and Fed officials emphasized they want to ensure inflation is tamed before embarking on any cuts.

“The Fed doesn’t need to embark on a big easing campaign to steepen the curve further,” said Gregory Faranello, head of US rates trading and strategy for AmeriVet Securities. “A little will go a long way like we learned in the last two months of 2023,” when bond markets rallied sharply just on the speculation of a Fed pivot toward easing.

Yield curves are rapidly normalizing. Yields on 10-year notes are now solidly above those on 5-year notes after more than a year of inversion. pic.twitter.com/FApGJW1qEd

— Lisa Abramowicz (@lisaabramowicz1) January 18, 2024

Two-year yields about matched those on 30-year bonds as of Friday morning in New York. As for Fed cuts, markets are now pricing in about 1.4 percentage points of reductions this year, compared with expectations of as much as 1.7 percentage points of easing as recently as last week. Meanwhile, March rate cuts that were largely baked into the market are now seen as more of a toss-up.

Kellie Wood, deputy head of fixed income at Schroders Plc in Sydney, is sticking with bets on a steeper curve even after closing out straight duration bets. She is positioned for two-year US notes to outperform 30-year bonds, and sees the potential for longer-dated yields to exceed shorter peers by more than a full percentage point.

“We’ve been positioned in steepeners for a while,” Wood said. She was initially expecting to see long-end yields to rise amid higher term premium, and now she is betting on a drop in front-end yields due to rate cuts.

Investors anticipating a faster pace of curve steepening, one that sends short-term rates decisively below those with longer maturities, need to see compelling evidence of a much weaker economy that would force the Fed’s hand. Instead, the current trajectory points to a gradual easing cycle stemming from a slowdown in inflation and moderating growth. The US central bank itself envisions only three-quarters of a point of cuts this year.

“In normal times it’s the short rate that comes down sharply given a recession is coming, and that causes the dis-inverting,” said Tobias Adrian, director of the International Monetary Fund’s monetary and capital markets department. “But now the US is likely to have a soft landing and so basically the curve could just flatten.”

What Bloomberg Intelligence Says...

“If the market eventually prices for slower rate cuts in line with Waller’s ‘methodical’ path, two-year yields could move 40 basis points higher and yield-curve steepening could slow.”

— Ira F. Jersey and Will Hoffman, BI strategists

Of course, conditions may shift quickly. Roger Hallam, global head of rates at Vanguard, sees two potential catalysts for a steeper curve. “One is a recession or a financial accident that causes the Fed to ease more quickly and significantly than expected. That’s a bull steepening case in an adverse outcome,” he said, referring to a situation where yields across the curve fall, with short-term yields leading the decline.

A more problematic outcome would be if longer-dated yields push higher, as seen last year when a surging US deficit raised concerns about financing for the US Treasury. “The deficit challenge in the US remains very material,” and one cause of steeper curve would be a “Fed easing before inflation is truly slain,” as the market seeks more of a term premium for holding longer-dated bonds, Hallam said.

Across the entire Treasury market, yields on three-month bills aren’t far from the lower end of the current policy band, 5.25% to 5.5%, so this part of the curve still remains heavily inverted.

‘Happy’ Steepener

Bills sit more than 1 percentage point above a 10-year yield of 4.16%, a negative relationship that has existed for at least 14 months from October 2022. That period does mark the average lead time of inversion before the previous four recessions, according to Campbell Harvey, the Duke University professor who first established the predictive qualities of an inverted curve back in the 1980s as regards economic downturns.

“How this is going to play out is largely to do with the Fed cutting rates,” Harvey said in an interview. “The Fed has to cut fairly substantially to get to the point that we don’t have an inversion.” Campbell doesn’t rule out a far longer period of inversion between bills and longer-dated Treasuries. “The curve could stay inverted for all of 2024.”

Stephen Bartolini, a fixed-income portfolio manager at T. Rowe Price, warns of another scenario for curve watchers. “If we have a re-acceleration in the economy, the long end of the curve could give up a lot,” he said. After the bond market’s late-year rally helped to drive down benchmark borrowing costs, “we’ve had substantial easing of financial conditions.”

Put another way, “There is the happy steepener, which is what everybody wants, which is when you get cuts,” AlphaSimplex’s Kaminski said. “Then there’s the not-so-happy steepener, which would be a situation where long-term yields go higher.”

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our full schedule of upcoming CE-approved virtual events.

Bloomberg News provided this article. For more articles like this please visit bloomberg.com.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All