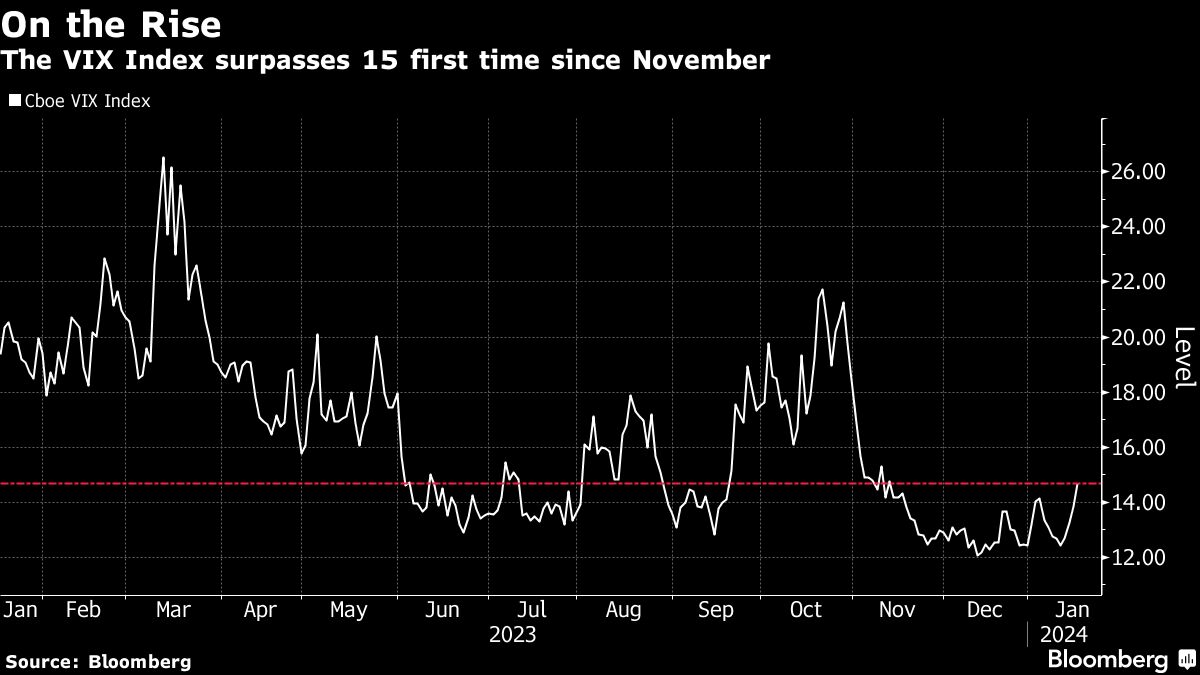

A sense of torpor that’s descended on Wall Street’s chief fear gauge since the fall is starting to disappear.

A drop in the S&P 500 Index on Wednesday pushed the Cboe Volatility Index briefly above its 200-day moving average, the line it hasn’t closed above since October. The VIX — measure of the 30-day implied volatility of the S&P 500 based on out-of-the-money options prices — edged toward 16 in the morning, a level that implies daily swings of 1% could be in the offing, before slipping back.

Options traders are paying a bit more for protection amid geopolitical concerns, uncertainty over the Federal Reserve’s interest-rate path, an earnings season that’s off to a mixed start and a non-stop rally in US stocks in late 2023 that made positioning elevated and valuations somewhat stretched. It doesn’t help that the 10-year Treasury yields are back to hovering above 4% after trading below that level in the second part of December.

But even as the “fear gauge” edges higher, there’s hardly a sense of panic. A measure of projected correlations between the S&P 500 stocks in the next 30 days is hovering at 17, not far from the lowest level since 2018, as traders expect the companies to dance more to their own tune as they report earnings. But should profits underwhelm the already modest expectations, that could be a recipe for widening price swings, according to Matt Maley, chief market strategist at Miller Tabak + Co.