Our Precarious 2024 Economy

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Inflation is not over. We all see that in our everyday lives. The next wave will be torturous and will last a long time. The U.S. cannot follow in Japan’s footsteps.

The Federal Reserve (Fed) is bankrupt, hemorrhaging annual operating losses of $244 billion. It should allow market forces to set fair prices for stocks and bonds.

The Fed should not pivot back to its zero-interest-rate policy (ZIRP). Instead, it should continue unwinding its unprecedented $8 trillion balance sheet.

It’s that time again to peer into the year ahead. Most see a rosy 2024, following a spectacular 2023 that delivered a 26% return on the S&P 500 and a whopping 45% return on the Nasdaq. Market observers expect the Fed to pivot in 2024, lowering interest rates, because inflation is under control.

This article is in stark contrast to those optimistic predictions for 2024. There are reasons to be concerned about the economy and financial markets.

The Fed is manipulating financial markets to buoy the economy. It rescued the economy in 2009 with quantitative easing (QE) that ultimately necessitated ZIRP to afford interest payments on the QE-generated skyrocketing debt. QE and ZIRP are very expensive!

Along the way, Japan has served as a model that justifies QE, but the U.S. can no longer run its economy like Japan with its “financial repression.” Efforts to fight inflation are bankrupting the Fed as it unwinds its balance sheet. It’s time to unravel QE and to take the consequences, whatever they may be.

The Fed “pivot” anticipated by most will defer and intensify the pain. It would be a mistake. The Fed should not pivot to ZIRP, even though inflation appears to be under control. There will be a second wave of inflation that is much worse.

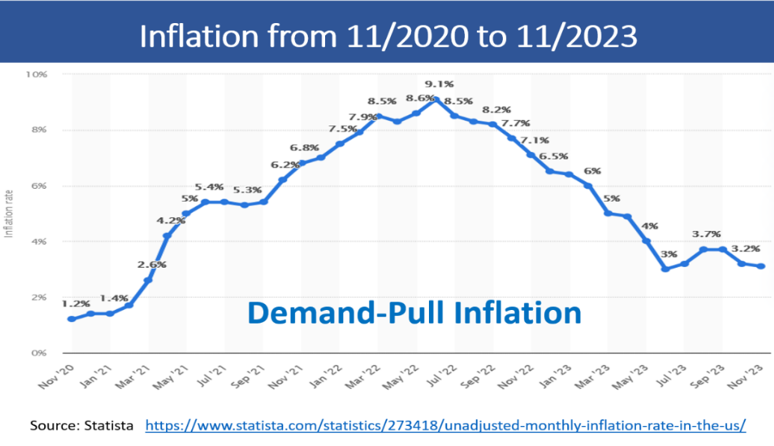

The first inflation wave is ending

Inflation has plummeted from its 9% high in June 2022 to 3%. It was transitory, lasting just three years. This decrease would have occurred without Federal Reserve actions because supply-chain disruptions caused by COVID were destined to get resolved as shipping containers were unloaded. This form of inflation is called “demand-pull.” It is caused by demand for goods and services exceeding supply.

Despite inflation, or perhaps because of it, the U.S. stock market soared in 2023, inflating the bubble beyond credibility. It could be that investors see stocks as an inflation hedge. Time will tell.

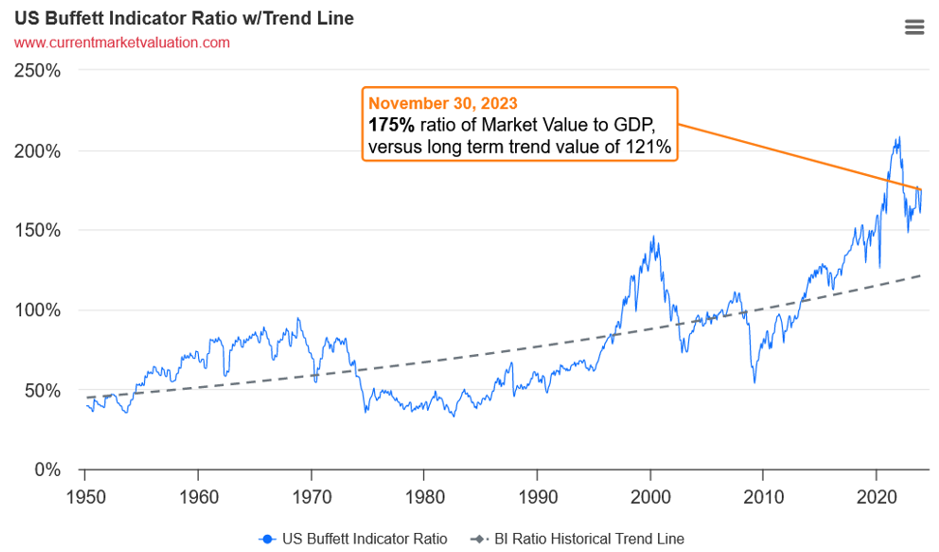

Many measures of valuation indicate that the market is very expensive and due for a correction. The Warren Buffett indicator is an example shown in the next graph. The 20% loss in 2022 was followed by a 26% gain in 2023, bringing the market back to its frothy January 2022 level.

The 2022 correction was a head fake, resetting the stage for the real deal.

Although it wasn’t needed to control this current wave of inflation, the Fed must permanently take its foot off the interest rate brake (ZIRP) because it has exploded its balance sheet holdings to $8 trillion, well above its $1 trillion long-run historic norm. It’s time to shrink the Fed’s balance sheet even though no one knows what the consequences will be, other than they will be huge.

The next inflation wave will challenge the economy and the Fed. It will not be transitory. A pivot to ZIRP will intensify the problem.

The next wave of inflation – the big wave

The other form of inflation, called “cost-push,” is not transitory. It is classic inflation caused by too many dollars chasing too few goods. It happens when a government prints too much money, as has happened globally over the past decade.

Argentina and Venezuela are resource-rich countries still suffering from hyperinflation, defined as inflation above 50%, because their governments made monetary mistakes that the U.S. is repeating.

The world is running on unprecedented levels of debt, to the tune of $200,000 per capita. The U.S. enjoys a special status as the “cleanest dirty shirt in the laundry basket” because the dollar is the world’s reserve currency. We enjoy a special privilege that provides insulation, but we are not immune to inflation. Also, China could be colluding with Rusia to make the Chinese yuan the world’s reserve currency, even though China’s economy has not yet recovered from COVID.

The U.S. printed more money for COVID than any other country, exposing it to cost-push inflation that will last a long time and will drive inflation above the current 3%. It’s the next wave.

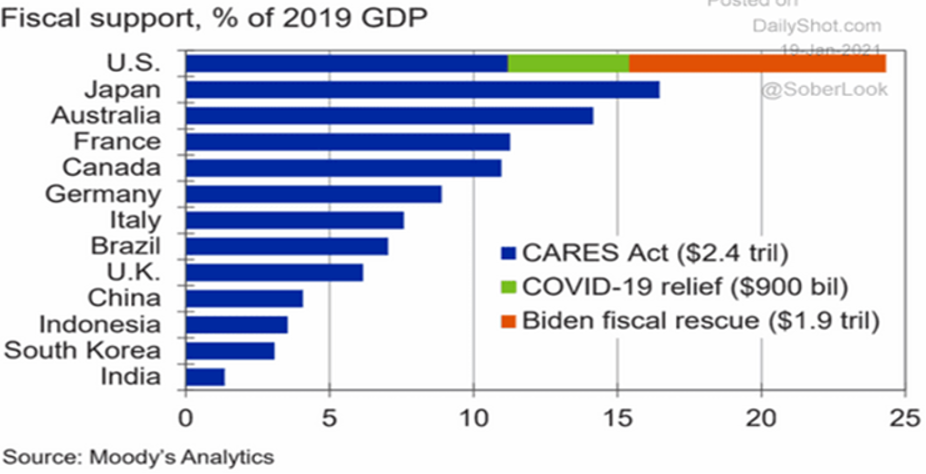

Who is paying for COVID? When was the last time you heard the words “balanced budget”? COVID relief has a colossal $5 trillion price tag.

Modern monetary theory (MMT) is the purported justification for the money the U.S. has “printed” since 2008. This theory says that governments who own the printing press can print all they want to solve economic crises, unless it causes inflation, in which case that money needs to be taken back with taxes.

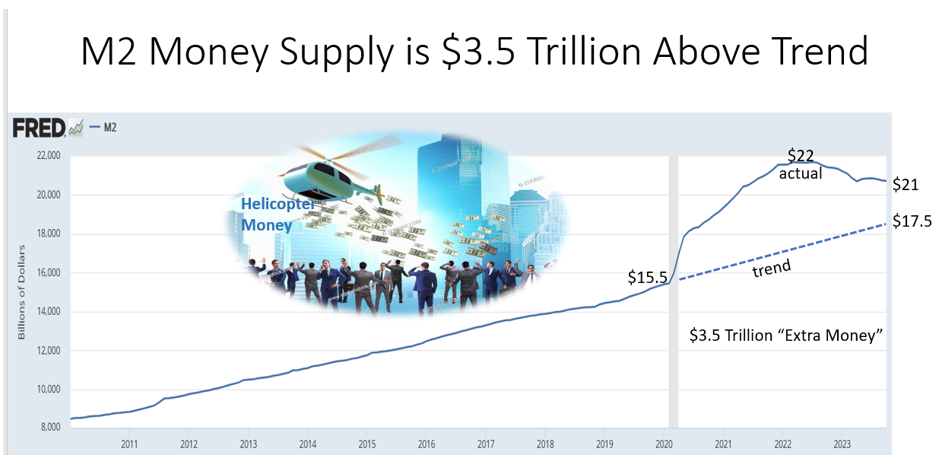

The money supply is currently $3.5 trillion above what is needed to support economic activity. Some of it was “helicopter money” distributed to taxpayers for COVID relief. “Excess money” will drive cost-push inflation in the next wave. The trend shown in the graph below is the money supply needed to keep the economy running smoothly. The actual shows the excess, also known as “too much money.”

There is little political will to suck that money out of the economy with taxes, so inflation will persist.

MMT appears to have “worked.” The recession in 2008 was short-lived, stock prices soared, and inflation remained near zero – until recently. We are experiencing a mix of demand-pull and cost-push inflation that is transitioning to mostly the latter.

A couple videos explain the craziness in a clear and humorous way. Debt limit – a guide to American federal debt made easy uses household debt to explain federal debt. Fred Thompson on the Economy explains the wisdom of QE.

Excess money of $3.5 trillion is a lot, but the multiplier effect amplifies this into $35 trillion, which is 150% of GDP and 100% of our total debt. One trillion is 1,000 billion or a million million – it’s a huge amount of money According to CNBC :

- If you paid out $1 per second, to settle a $1 million debt would take less than 12 days. To pay off $1 billion would take 32 years. Paying off $1 trillion at a dollar per second? 32,000 years. A trillion is a 1 followed by 12 zeros, like this: 1,000,000,000,000.

- A trillion square miles would cover the surface of 5,000 planet Earths.

- A trillion people would be 10 times more than have ever lived (based on the Population Reference Bureau’s very rough estimate of 108 billion humans ever).

- A trillion dollars is enough to give $3,195 to every man, woman and child in the United States. (We got this helicopter money in bigger checks.)

- For a typical U.S. household, making $50,000 per year, to earn enough to pay off a $1 trillion debt would take 20 million years.

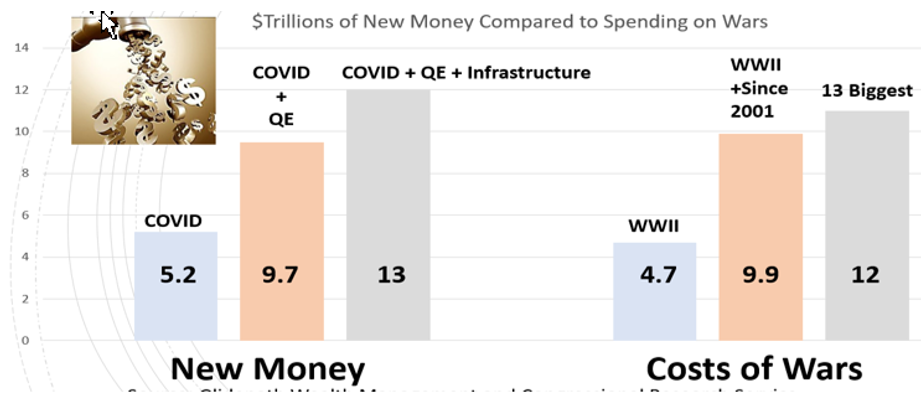

Piling on

The following graph shows the magnitude of recent money printing by comparing it to our most expensive wars:

But that’s not the entirety of the debt story. We (through our government) have made promises for Social Security and Medicare that are unlikely to be kept, and QE has widened the wealth divide beyond comprehension.

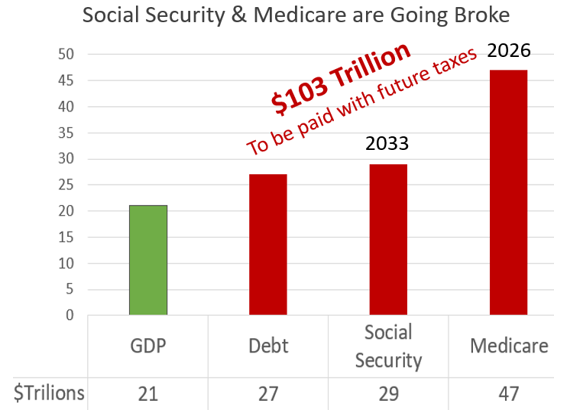

The following image shows that the total U.S. debt is more than five times GDP, including off-balance-sheet promises for Social Security and Medicare.

Tax receipts for Social Security have been insufficient to pay all the benefits since 2018. The Government Accountability Office (GAO) reports that Medicare will be bankrupt in 2026, followed by Social Security in 2033. Many say that owning the printing press means you can’t go bankrupt, but inflationary forces are already out of control.

Some argue that U.S. debt has been increasing for decades without causing appreciable inflation, but interest on $35 trillion breaks the bank when interest rates are above zero. MMT has begun to poke the inflationary bear, and it is infuriated. Cowboy wisdom instructs,“When you find yourself in a hole, stop digging.” That is the Fed’s current mission.

The Federal Reserve is the arsonist charged with putting out the inflation fire

It’s ironic that the Fed is coming to the rescue to control inflation when it is complicit in creating it.

“Printing” is not running the presses. The Treasury borrows money as Treasury bonds and bills. In ordinary times, there are plenty of buyers for those bonds, but recent times have not been ordinary, so the Federal Reserve buys them, manipulating bond prices to execute ZIRP. In this way, money is created out of thin air.

According to the Federal Reserve, its balance sheet has skyrocketed from normal levels under $1 trillion to $8 trillion, with most of the increase coming during the pandemic.

The plan is to unwind this $8 trillion and return to the $1 trillion typically held historically. The consequences of this shrinking of the Fed’s balance sheet are unknown. It’s an experiment of a magnitude that has never been run.

Buffett praised the Fed for saving the economy in 2009 with its QE, but cautioned that unwinding the huge buildup of the Fed’s holdings in bonds could have disastrous consequences. Also, at a press conference on May 4, 2022, following the Fed’s announcement that it would begin QT in June, Fed Chair Jerome Powell offered, “I would just stress how uncertain the effect is of shrinking the balance sheet.”

In other words, tightening is dangerous, and the greater the buildup, the greater the danger. The Fed is playing with fire, as shown in the following:

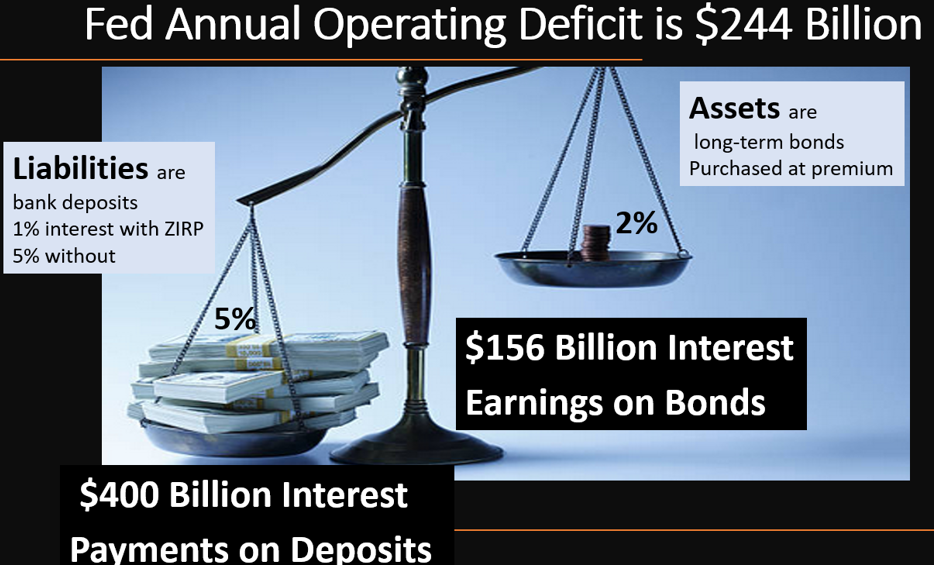

The Federal Reserve is bankrupt

Quantitative tightening (QT) has increased the payments on the Fed’s liabilities. Earnings on its assets are short of liability payments. According to this article, the Fed is hemorrhaging an annual operating loss of $244 billion, making it bankrupt:

Assuming, as a rough approximation, that the bonds it purchased pay an average rate of 1.75 percent, and the average rate paid on bank reserves and ONRRPs (overnight reverse repurchases) is 4.85 percent, then the Fed is paying about 3.1 percent per year more than it receives on its $7.88 trillion dollar securities portfolio. That’s a loss of $244 billion per year!

The most recent data show that the Fed owes the Treasury over $48 billion, which exceeds its total capital. The Fed, by common standards, is insolvent.

What does the Fed do when its liabilities exceed its assets? It doesn’t go into legal bankruptcy like a private company would. Instead, it creates fictitious accounts on the assets side of its balance sheet, known as “deferred assets,” to offset its increasing liabilities.

Deferred assets represent cash inflows the Fed expects in the future that will offset funds it owes to the Treasury. As the Fed describes, “The deferred asset is the amount of net earnings the Reserve Banks will need to realize before their remittances to the U.S. Treasury resume.” The Fed had already accrued $48 billion in deferred assets, and the amount is only getting larger.

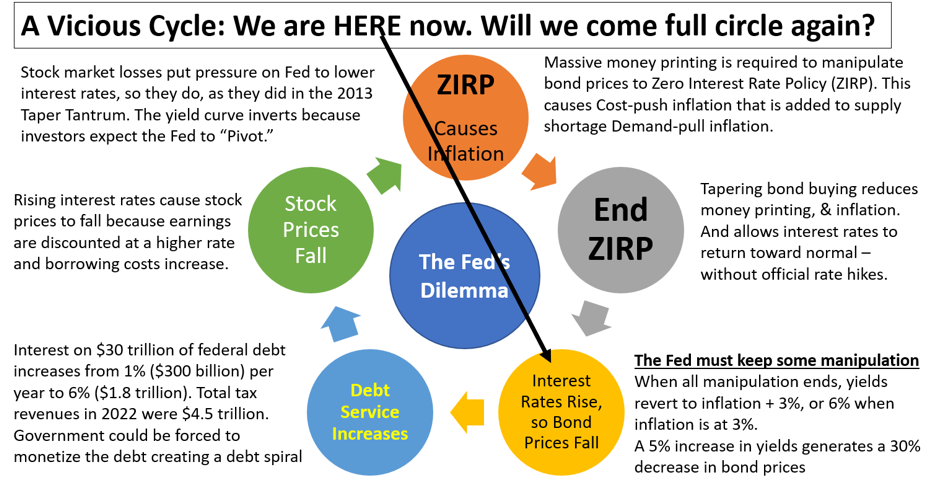

The Fed needs to lower short-term rates – pivot – to stop the bleeding. But this won’t stop cost-push inflation, because all that money is sloshing around the economy. Pivoting will drive real rates (net of inflation) well below zero, forcing investors to seek alternatives, as suggested in the conclusion of this article. It’s complicated, as Buffett and Powell agree.

Some say that Japan has pulled off QE for decades, so the U.S. can certainly do so too. But that’s not true for reasons explained in this article:

In short, as a way of supporting the large deficit caused by the aging population, Japan’s strategy involves a concept called financial repression, meaning the government uses regulatory methods to borrow cheaply and widen the returns gap on their balance sheet.

For this to hold, some economic agent must be willing or forced to lend to the government cheaply. In this case, the economic agent is Japanese households. When Japanese households—who hold a large amount of low-return demand deposits—deposit their savings into banks, the banks can then lend cheaply to other domestic borrowers such as the government. However, this is not the case in the U.S., where households’ largest portfolio share is equity. Therefore, opportunities for a cheap funding source are much more limited for the U.S.

Given differences in the level of net liability and in the revenue from returns between the U.S. and Japan, the aggressive fiscal and monetary policies adopted by Japan may not be appropriate or even feasible for the United States. Thus, we should not rely on the Japanese experience to predict the U.S. fiscal situation.

The Fed does not have a dial that it can turn to a desired level of interest rates, but it has managed to suppress long-term interest rates by buying bonds at premium prices. When the Fed lets its foot off the brake by tapering its bond buying, interest rates go up and bond prices go down and the Treasury must attract other buyers. This is called “shrinking the balance sheet.”

No special Fed meeting is required to “set” an interest rate – rates converge toward a fair market price when they are not being suppressed. A fair market price in a 3% inflationary environment is 6%. We should expect inflation to increase above the current 3%, causing interest rates to increase again.

Increased deficit spending

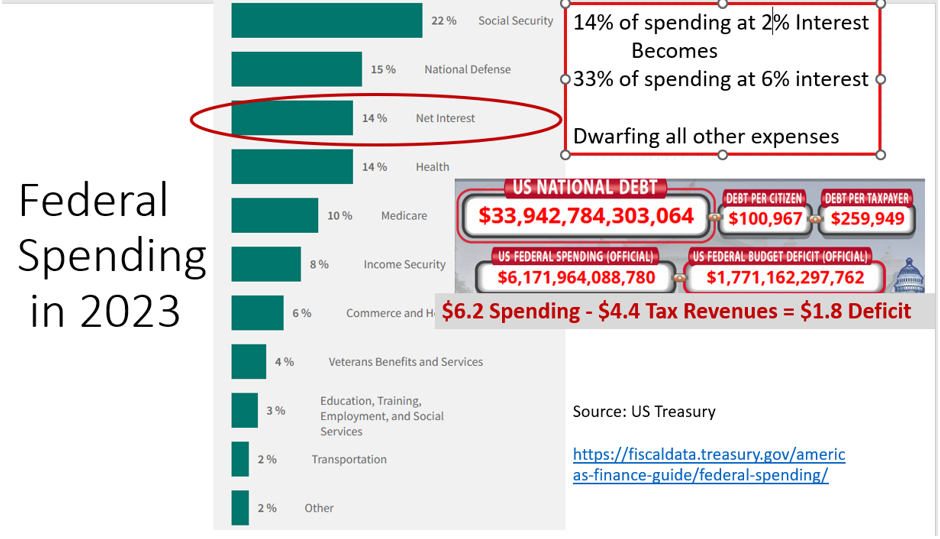

Increases in interest rates do a lot of damage, as we learned in the 2013 “taper tantrum.” Higher interest means greater payments on our $34 trillion government debt. Interest expense is 14% of total spending, which makes it the third largest expense behind Social Security and national defense. The interest rate on the debt is only 2% due to ZIRP. Tax receipts are about $4.5 trillion per year, which falls short of $6.2 trillion total spending, so the annual deficit is $1.7 trillion.

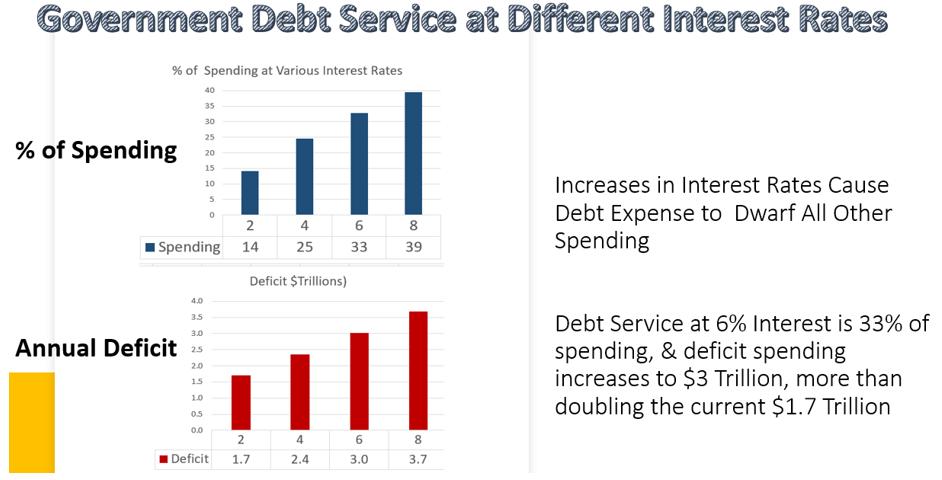

Higher interest rates increase spending on “net interest” as shown in the following chart. At 6% interest, spending for payments on the debt will expand to 33% of all spending, more than doubling the current 14%, and the annual deficit increases to $3 trillion, more than doubling the current $1.7 trillion annual deficit. The debt clock will spin out of control.

Ending ZIRP drives up interest expense beyond reason, but it needs to happen. What’s worse is the stock market will crash, as it almost did in the 2013 taper tantrum, because bonds become attractive alternatives, borrowing costs increase, and corporate earnings are discounted at a higher rate. At this stage in the cycle, the Fed will be encouraged to stop tapering, and resume its bond buying. The market expects this “pivot” to occur soon, again.

But this time is not like 2013, when inflation was near zero. This time Fed bond buying will fuel the very inflation fires that the Fed is trying to extinguish.

The Federal Reserve cannot simultaneously continue to manipulate interest rates under ZIRP while subduing inflation. It will have to choose. The better choice is to allow bonds to return to market-driven prices, increasing interest rates and driving down stock prices. Allowing market forces to work is the best choice even if it causes pain in the short term.

As proclaimed in a Chiffon margarine commercial, “It’s not nice to fool Mother Nature.” Markets are best left to establish fair prices on their own.

Demographic bubbles

Baby boomers (aged 58-77) are outnumbered by millennials (aged 27-42). Millennials are our largest generation. Some say that the answer to our inflation threats rests with millennials. I don’t see how, other than these commentators blame baby boomers for our problems and expect millennials to solve them somehow.

Baby boomers will suffer the immediate consequences of inflation and market crashes, then their heirs will feel the pain too, and then their heirs’ heirs – the millennials.

Conclusion

Market pundits have declared an end to the inflation that has launched a stock market rally – the Santa Rally – in anticipation of a Fed pivot. The markets are counting on renewed manipulation. But the Fed historically has lowered interest rates to buoy a falling stock market – to stimulate stock investing – rather than to fuel a rising stock market.

Professor Jeremy Siegel (Stocks for the Long Run) warns that the anticipated Fed pivot would be bad for stocks because it would mean that we have a recession. The Fed should only lower rates to alleviate a recession.

The Fed should let the market determine fair prices for stocks and bonds. It should continue its abandonment of ZIRP and shrink its balance sheet, even though the consequences are unknown – and possibly catastrophic.

The big question is how long the Fed can operate at a $244 billion annual deficit. Allowing market forces to work could exacerbate the Fed’s dilemma and create a very long market failure and economic recession. Forewarned is forearmed.

We’re ignoring lessons that should be learned from recent stock and bond market advances. Ignorance is not bliss. Ignoring a bankrupt Fed does not change facts.

Investors should prepare for the next wave of inflation by moving to inflation protection like TIPS and other assets that are not stocks or bonds.

We should worry about 2024. This article discusses many of the challenges we’ll face. There are others shown in the following table. For more information, please read The Rest of the Story.

In fairness, there are reasons to be optimistic in 2024 that most are embracing. Weigh them against this table. I’m in the minority, but I’m confident I’m right.

Please watch my video on this topic.

Ron Surz is president of Target Date Solutions, developer of the patented Safe Landing Glide Path and Soteria personalized target date accounts. He is also co-host of the Baby Boomer Investing Show.

His passion is helping his fellow baby boomers at this critical time in their lives when they are relying on their lifetime savings to support a retirement with dignity, so he wrote a book, Baby Boomer Investing in the Perilous 2020s, and he provides a financial educational curriculum.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Live Virtual Event: Join Now

Upcoming Virtual Events View All