It’s a seller’s market for infrastructure asset managers. Conventional and alternative investment firms are falling over themselves to expand in this lucrative area, and M&A is the easiest way for them to leapfrog the competition. Don’t expect high deal prices to act as a break. Consolidation into scale players just creates more pressure on smaller infrastructure managers to bulk up.

BlackRock Inc.’s agreement to buy Global Infrastructure Partners (GIP) for $12.5 billion earlier this month is the latest and most eye-catching transaction in the sector and follows recent smaller deals by CVC Capital Partners and others.

Infrastructure isn’t a new asset class by any means but it’s the flavor of the month. The business accesses private capital to support core needs like roads, airports, data centers, power grids and telecoms networks. Governments save money while investors gain exposure to predictable, long-term cash flows which — to varying degrees — rise with inflation. That makes infrastructure a good match for pension liabilities.

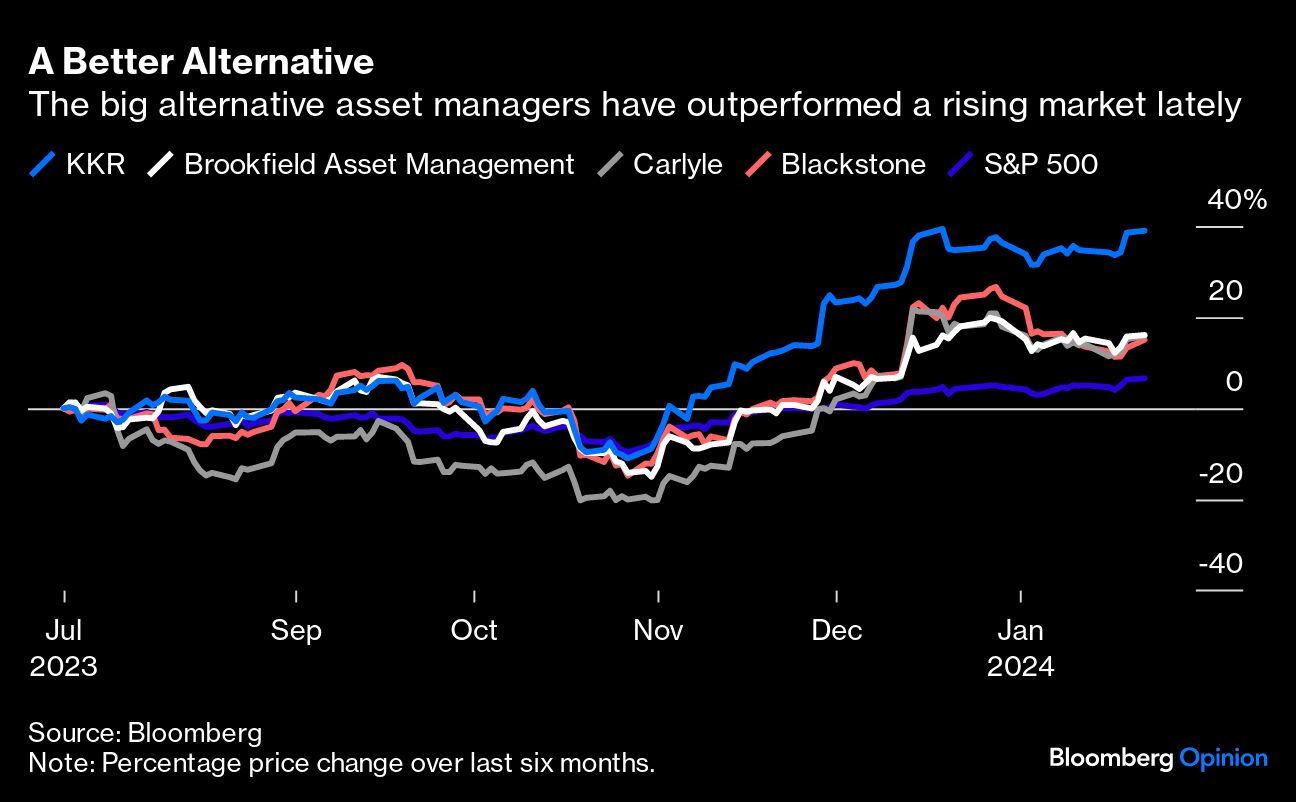

You can see the attraction for investment management firms sitting in the middle of the money flows. Infrastructure offers a fee stream that’s durable, growing and nicely profitable. For regular firms like BlackRock, the business is more rewarding than active and passive fund management and makes you look a bit more like the alternative investment firms that enjoy high stock-market valuations. For private equity, infrastructure offers diversification from leveraged buyouts — a needed strategic shift now that the cheap debt that fueled past returns is history.

Of course, BlackRock’s deal is easily digestible for an investment behemoth with a $120 billion market value. Only around one-quarter of the purchase price is cash, and that’s being borrowed. The rest will be delivered in BlackRock shares, and a chunk of these are subject to GIP performance targets.

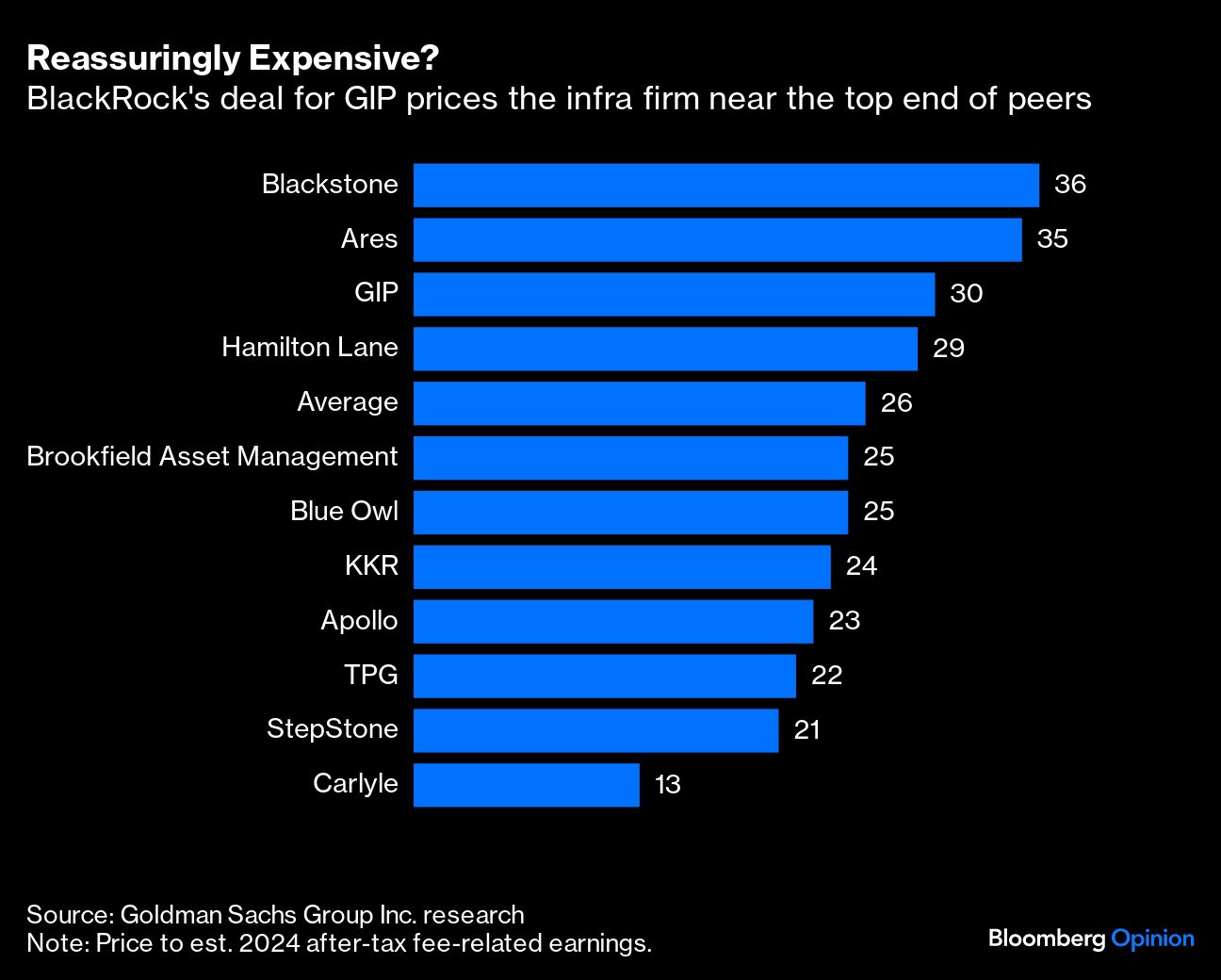

Still, the economics of the BlackRock deal show the market power of those with quality infrastructure businesses to sell. The price is some 13% of the $100 billion managed assets being taken on. OK, that’s a crude measure. But the valuation is still generous relative to where the alternative investment managers trade. A multiple of around 30 times this year’s estimated after-tax fee-related earnings (a measure of management-fee income) is higher than the listed alternative investment peers bar Blackstone and Ares Management Corp., says Goldman Sachs Group Inc. research.

What does BlackRock get for the outlay?

First, status and clout. Its infrastructure business trebles in size, catapulting the company to be one of the industry’s leaders. The deal is also even bigger than it looks: GIP is on the road raising a fund that analysts reckon could close at $25 billion.

Second, a new income stream, whose margins BlackRock says are at least 50%. As things stand, only $60 billion of GIP’s assets are generating fees (the bulk of the rest is waiting to be put to work). GIP generated $760 million of management-fee revenue in 2023. Analysts reckon that could rise to around $1 billion this year. The Goldman researchers then look to 2025 and estimate fee-paying managed assets could hit as much as $96 billion in an upside scenario, generating management fees of nearly $1.2 billion.

Apply those tasty margins and lob off tax, and fee-related earnings would be $481 million. As an initial return on the total acquisition price here, that’s still pretty modest.

The real payback will have to come further out. On a 10-year view, analysts at TD Cowen see strong growth in fee income — and performance fees from year five — delivering a 14% internal rate of return. That’s a bit shy of BlackRock’s own estimates. But shareholders would doubtless be pleased if that materializes.

All this will encourage more deals. As Morgan Stanley analysts point out, scale in this business means your funds can participate in auctions for even bigger infrastructure assets. That puts your firm at a competitive advantage. With BlackRock creating a more formidable player in the market, rivals will want to bulk up too. Deals often beget deals, and that surely applies here. If you have an infrastructure manager to sell right now, you shouldn’t find it hard to get an auction going.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Chris Hughes