The number of studies showing the success of universal basic income programs continues to mount. The latest comes from the Federal Reserve Bank of Minneapolis, which recently released its initial report on a pilot project designed to test the feasibility of so-called UBI. Just like the almost two dozen other local government experiments with paying struggling households a set stipend so they have the resources to improve their situations, the initial results are very promising. And yet, implementing UBI as policy would be premature.

In the Minneapolis experiment, 500 low-to-moderate income households were picked in mid-2022 to participate. Researchers randomly selected 200 households to receive a cash payment of $500 for 24 months starting in 2023. The other 300 households constituted the control group. After just 12 months, the group that received money saw a statistically significantly higher percentage of food-secure households, or 48%, than the control group, 32%. On the Kessler measure of psychological distress, where a reading below 20 represents well-being, the group receiving payments averaged 21, versus 25 for the control group.

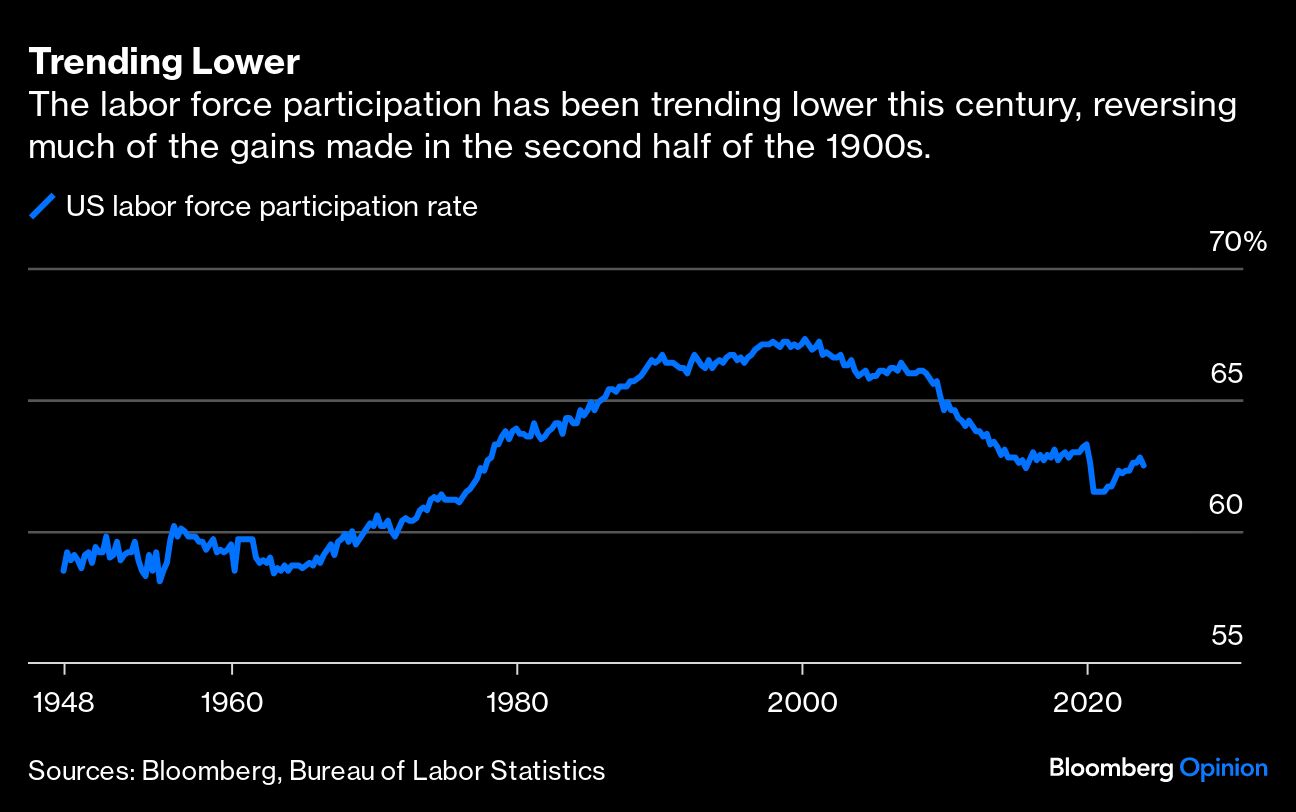

The major flaw in this and all such UBI experiments to date is that they are temporary and involved small groups. We don’t know, for example, what the effects of UBI would be in terms of labor force participation if payments were made over a much longer period. Would recipients be inclined to stay out of the workforce if they knew they would have a steady stream of payments coming for many years? And what would be the effects of being out of the workforce for an extended period? And would they even be able to get back into the workforce?

To make their case that UBI is a real solution, its proponents need to turn their efforts toward much larger, state-wide experiments that last for five to 10 years. It would be foolish for participants to make potentially life-altering decisions, such as dropping out of the labor force, based on some short-term payments. But with a permanent, national-level program the incentives change dramatically.

Knowing that a stipend will be coming month-after-month, year-after-year, participants might choose to make lifestyle changes that lower their cost of living. One of those changes might be moving to a remote location that’s less conducive to employment opportunities and where there is less reliable transportation. Such choices distance participants from the workforce, which is opposite of UBI’s intent.

Research shows that acquaintances are an especially powerful source of information about and access to new job opportunities. As labor force participation declines, the networks of acquaintances within a community become a less rich source of job opportunities and the cost of finding employment for members of that community rises.

Then there are the knock-on effects of being out of the workforce for a long period and not having the contacts to easily get back in. For starters, children growing up in a community with little income mobility experience lasting negative effects. A series of papers by Harvard economist Raj Chetty demonstrates that children who move from low income-mobility communities to higher income-mobility communities experience greater income and educational attainment as adults than those who don’t.

To be clear, none of these potential downsides mean we should give up on exploring UBI, given the evidence of the potential benefits. If applied at the national level, a more generous UBI could perhaps replace the alphabet soup of anti-poverty programs with a single check delivered monthly to all households. In doing so, UBI proponents rightly argue that it would lower administrative costs while eliminating a difficult-to-navigate bureaucracy — one that leaves many families often unable to determine what assistance they’re eligible to receive or even how to apply for assistance.

Going one step further, making all Americans eligible to receive UBI payments regardless of need is a feature, not a bug for many economists. It would streamline both the tax system and social services by integrating them into a simpler and more economically efficient process. In this system, households that paid less in income taxes than they received in UBI would be net beneficiaries. For those facing higher tax burdens, UBI would simply replace the standard deduction.

We would be remiss to give up on UBI. The local-level experiments have established that such programs can produce positive effects in the short-term, and any negative impacts may only build slowly over time. It’s thus prudent to move on to state-level studies, which should last from five to 10 years and would come as many state governments are still flush with cash from pandemic-era federal stimulus and have the resources to try more ambitious projects.

A five- to 10-year time frame is also long enough to understand the life changes recipients may make and the lasting impact on poverty rates. At the same time, it’s a short enough horizon to mitigate the effects on children that might grow up in low income-mobility communities. Although serious questions surrounding UBI remain, proponents should not be disheartened.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Karl Smith