Trading in bonds these days means having to put up with more frequent market gyrations — and that’s just fine with big investors like Pimco and BlackRock Inc.

Increased volatility has been a feature in the Treasury market for the past two years, as spiraling inflation, Federal Reserve interest-rate increases, mixed economic signals and stepped-up government borrowing all combined to keep investors on edge. This contrasts with the numbing conditions that prevailed for much of the prior decade amid the heavy hand of central-bank support.

Now, even as some of that turbulence subsides with Fed rate cuts on the horizon, volatility remains elevated. The uncertainty around the timing of reductions and path for the economy leaves plenty of room for big market swings and opportunities to profit from them.

“We really like this environment,” said Daniel Ivascyn, chief investment officer at Pacific Investment Management Co. “The tendency for some overshooting in rates in both directions allows us to express tactical views.”

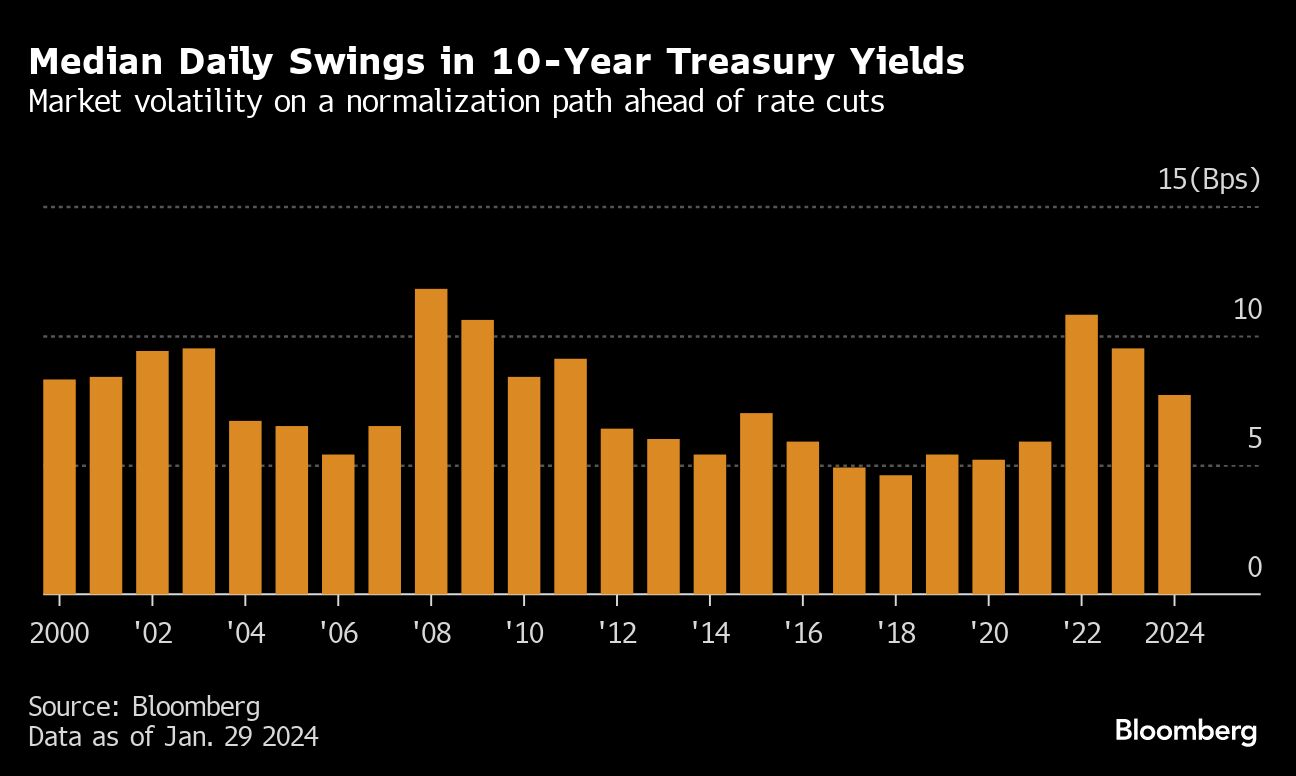

The average and median daily swing in the US 10-year yield has drifted downward this year, to less than 0.08 percentage point, according to Bloomberg calculations. While that is more muted than the activity during the prior two years, the overall trend remains the highest since 2011, the calculations show, and marks an important shift.

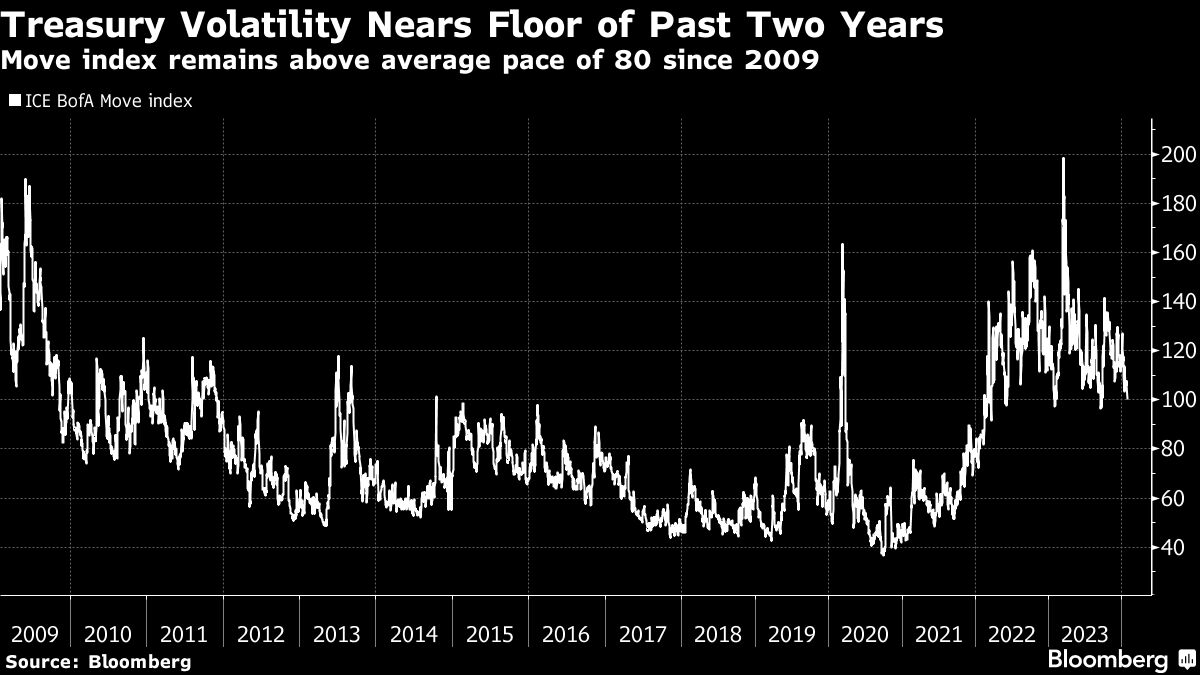

The ICE BofA MOVE Index — a key gauge of bond volatility that tracks anticipated swings in Treasury yields based on options — remains above a reading of 100, a ceiling only briefly surpassed between the end of 2011 and early 2022.

Bond investors are working this shift into their trading calculus. The general view is that a healthy market requires a reasonable level of volatility that can allow prices to respond to new information. It also stands to reward active investors selecting specific asset classes of bonds — such as mortgage-backed securities or corporate bonds — as opposed to the passive approach of owning a broad index.

Marilyn Watson, head of global fundamental fixed-income strategy at BlackRock, said rate volatility is welcome after central banks suppressed markets for so many years.

“Given the repricing that we’ve seen over the past 18 months or more, we can now actually get the underlying fundamentals of individual bonds,” she said on Bloomberg TV.

Rate-Cut Debate

Incessant market speculation over when the Fed will start easing rate policy, and how aggressive it may need to be, has been at the heart of recent market swings. Resilient data has compelled traders to reduce the odds of a quarter-point rate cut in March from a near certainty to less than 40%, and that’s weighed on the bond market this month.

Now, they await Fed Chair Jerome Powell’s press conference after the wrap Wednesday of the central bank’s two-day policy meeting to hear how he assesses recent progress on the inflation battle and what that entails for future rate decisions.

“Our strongest view is that central banks aren’t probably going to cut as quickly early in the year as markets anticipate,” and the extent of easing may be less than what traders now expect, said Ivascyn. That suggests a volatile course for rates and further opportunities for “making a little bit of money off this volatility,” said the Pimco chief, whose flagship $137 billion Pimco Income Fund has returned 5.9% in the past 12 months, well ahead of the 1.6% gain in the Bloomberg US Aggregate bond index during the same period.

A choppier trading environment also has other drivers such as the trajectory of Treasury government debt sales and how quickly the central bank adjusts the shrinking of its vast balance sheet, a process known as quantitative tightening. And in a world with little shortage of political flash points, the outcome of the US presidential and congressional elections in November may well prove another banana skin for investors.

All of these factors — as well as the possibility of an unforeseen market shock — help explain why US interest rate volatility remains elevated even after a notable slide from its peaks of the past two years.

“What’s interesting about 2023 and now is that bond volatility is running at about 6%,” said Kathryn Kaminski, chief research strategist at AlphaSimplex Group, referencing her firm’s in-house annualized measure of intraday sovereign rate volatility via futures. “So it’s still like 50% more than the vol we had prior to all the changes since 2020.”

While yields have climbed this year as traders ratcheted back the odds of a March rate cut, a buy signal for bonds is still intact, said Kaminski. “I’m more concerned now about longer-term bonds as there is so much more variability with them now. Short-term bonds are better now.”

What Bloomberg Intelligence Says ...

“The recent selloff in rates has seen implied volatility decline, which may reflect expectations of more constrained moves ahead. A bigger decline in volatility could need a reduction in the dispersion of forecasts.”

- Tanvir Sandhu, chief global derivatives strategist

As are US mortgage securities. These type of bonds improve markedly in value when yields settle down into narrowing trading ranges.

That has been a popular stance among asset managers. Just like the Treasury market in January, mortgages have been ceding ground after a monster rally late last year. With mortgage valuations cheap relative to US bonds, Pimco’s Ivascyn sees buying mortgage-backed debt as “one of the most efficient ways” to bet on a lessening in the intensity of market swings.

Greg Whiteley, a portfolio manager at DoubleLine, says volatility will persist “at least until the Fed gets on an identifiable rate cutting pace.” With opinion so divided about how things will play out, and given the underlying economic uncertainties, the bond market may be vulnerable to swings as large players adjust their positions based on the latest information.

“It puts a floor under the volatility market,” Whiteley said. “Choppy is my favorite word now. That describes almost everything — rates, spreads, and liquidity. It’s all choppy.”

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our full schedule of upcoming CE-approved virtual events.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Michael Mackenzie, Liz Capo McCormick