Spotting a recession in real-time, instead of months after the fact, is among the holy grails of forecasting. Two economists at Amazon.com Inc. say they’ve figured out a new way to do it.

The measure developed by Francesco Furno and Domenico Giannone is based on two inputs, one of them focused on real-economy activity and the other on financial conditions, according to a paper by the authors.

They say it works with a minimal lag — able to deliver a reading for a given month on the first business day of the next one — and they’ve designed separate versions for the US and Europe. Their paper doesn’t say whether either economy looks like it’s in recession right now — though the underlying data, especially for the US, doesn’t point that way.

It’s the latest contribution to the quest for recession indicators more timely than the official ones — which typically only deliver a verdict after many months. In the US case, for example, the pandemic downturn that began in early 2020 was only declared as a recession more than a year later by the experts at the National Bureau of Economic Research.

One reason for delays is that some of the data on which recession calls are based only arrives with a lag itself. So-called nowcasters tend to hone in on numbers that come out faster.

Furno and Giannone say that measures of financial conditions, often seen as guides to future recession risks, also offer important information about what’s happening in the economy right now — picking up early signals of distress encoded in asset prices.

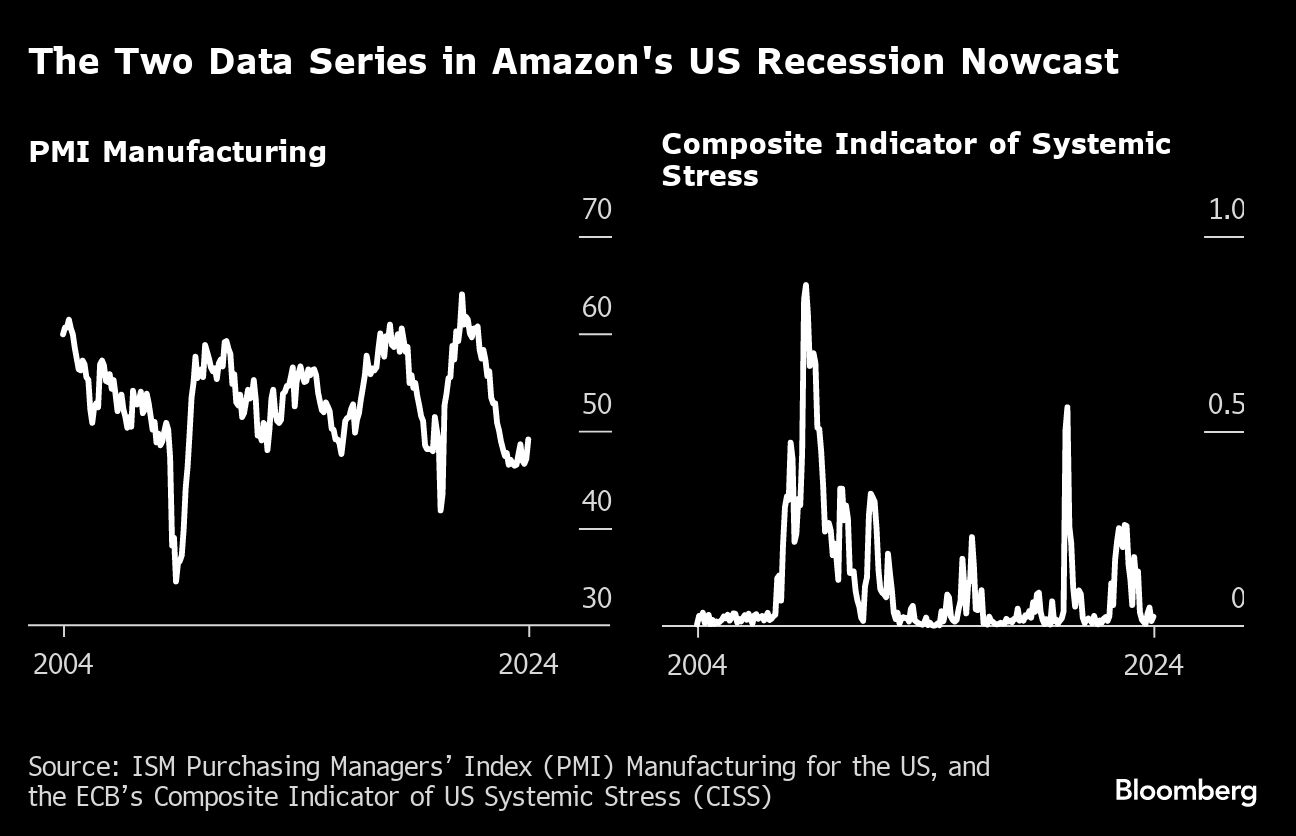

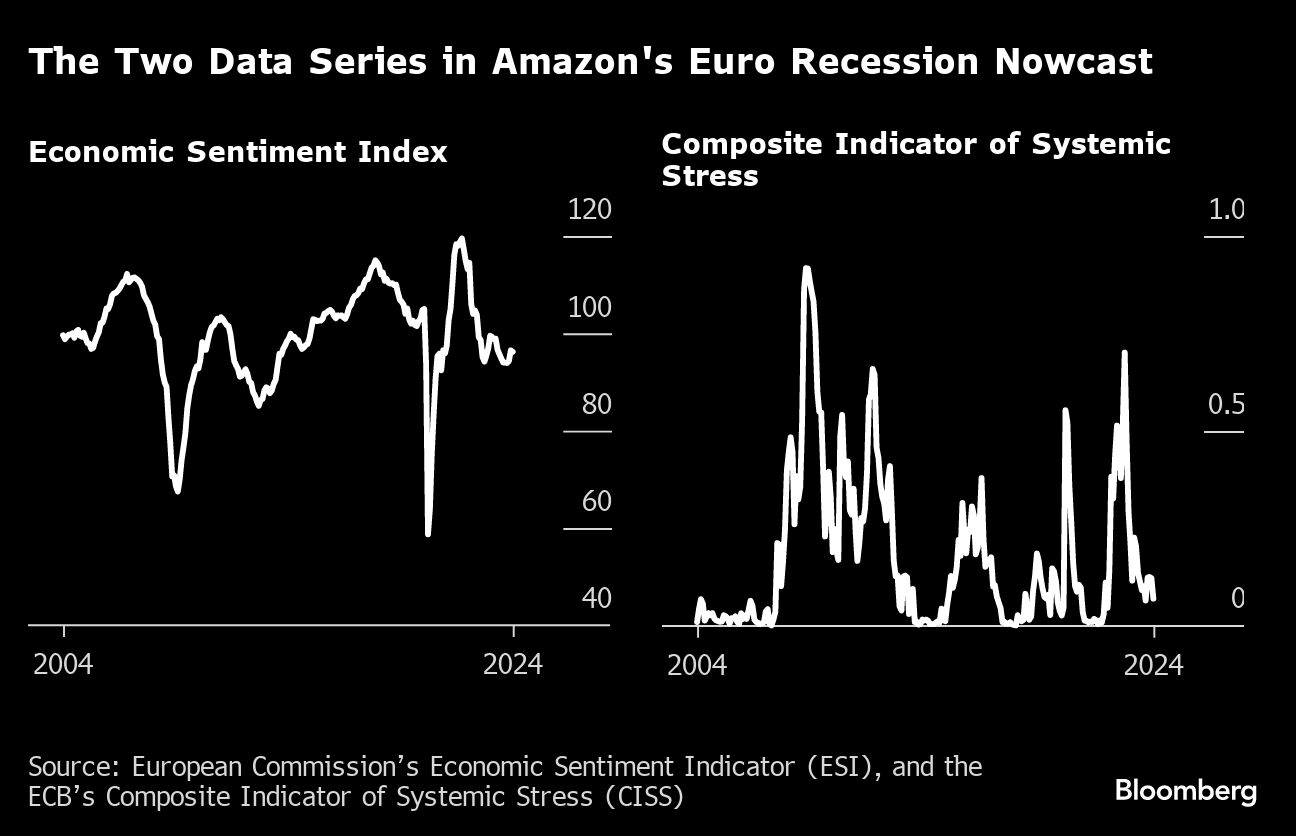

For the financial side of their US and euro-area nowcasts, the researchers use the Composite Indicator of Systemic Stress that’s published for both economies by the European Central Bank. For the real-economy side, they adopt the Purchasing Managers Index for manufacturing in the US — arguing that factory data still punches above its weight, even as services become more dominant — while in the euro area they opt for the European Commission’s Economic Sentiment Indicator.

Many efforts at recession nowcasting — like the Sahm Rule, named after former Federal Reserve economist Claudia Sahm — focus on increases in unemployment. One argument made by analysts who favor job-based measures over financial ones is that the latter are volatile and therefore more likely to give false alarms — predicting downturns that don’t happen.

Furno and Giannone say one advantage of their method is that the financial conditions measures, unlike jobless rates, aren’t subject to revisions.

While both approaches are similarly effective at identifying the start of a downturn, their own gauge is “more useful at detecting the end of a recession and the beginning of a recovery,” they write. “This is probably due to the lagging dynamics of the labor market, which tends to improve only after the recovery is already underway.”

Furno is an economist in the forecasting team at Amazon Web Services, while Giannone was senior principal economist at Amazon before joining the International Monetary Fund this year.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Alex Tanzi