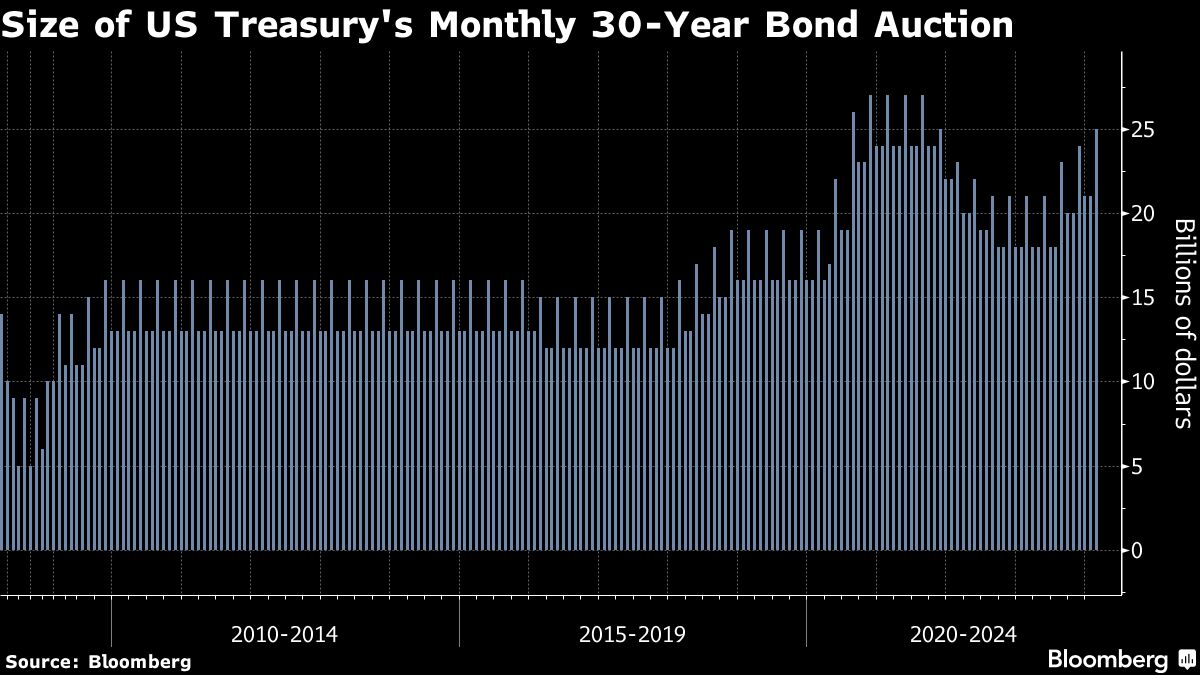

The US government sold $25 billion of 30-year bonds at a lower-than-anticipated yield, soothing investor nerves about demand for longer-dated debt.

Yields on US Treasuries briefly retreated from the day’s highs after the solid auction result, though resumed climbing later in the trading day. The 30-year sale — the largest in more than two years — was the last of three Treasury note and bond auctions this week.

The new bonds found receptive buyers, even as investors remain uncertain on when exactly the Federal Reserve will start cutting interest rates this year.

“The Treasury went three for three on its February refunding with good auctions,” said Kim Rupert, an economist at Action Economics. “There’s almost a FOMO bid for yield now.”

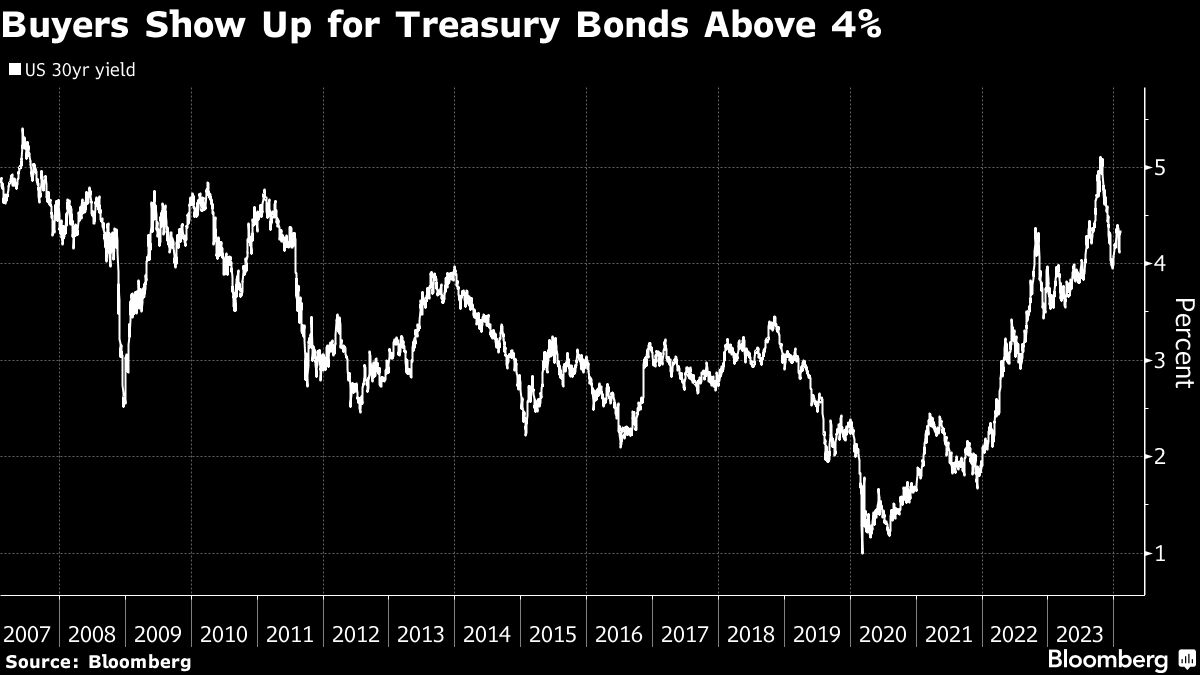

The 30-year bonds were awarded at 4.36% on Thursday, compared with a yield of about 4.38% moments before 1 p.m. New York time, the bidding deadline. The lower yield indicates stronger demand than traders anticipated.

Before the auction, 30-year bond yields had climbed to the highest in more than a week as the market sought a concession to smooth the supply of new bonds. The selling also picked up after the Labor Department’s weekly tally of new jobless claims was lower than anticipated.

The current 30-year bond’s yield rose as much as 5.6 basis points to 4.38%, the highest since Jan. 26.

“Given the amount of bonds Treasury has to auction this year, it’s a good sign that a reasonable concession attracted interest,” said Chris Ahrens, a strategist at Stifel Nicolaus & Co. “It looks like today’s yield concession on an outright basis” also proved to be “enough to draw decent indirect bidder interest of 70.7%.”

A steep rise in yields over the past week helped stoke demand for sales, but bond investors face an uncertain outlook for monetary policy that may impede rallies. While Wednesday’s $42 billion 10-year drew a lower-than-expected yield despite its record size, it has lost value since the auction, offering a cautionary tale for investors.

Still the Fed is looking to cut interest rates this year and into 2025. “On the back of that, the outlook for duration is pretty solid,” Vishwanath Tirupattur, chief fixed-income strategist at Morgan Stanley, said on Bloomberg Television, referring to a bond risk metric.

The high price-sensitivity of the longest-maturity Treasury security and its investor base dominated by pension funds and insurance companies make 30-year auction results less predictable than others.

What Bloomberg Strategists Say

“Overall, it’s a good result that caps a very good week of auctions, suggesting that investors are happy to scoop up ‘cheap’ bonds after the payroll and Powell rise in yields.”

— Cameron Crise, MLIV macro strategist

Three quarters of 30-year auctions since the beginning of 2016 have drawn higher-than-anticipated yields, according to Ian Lyngen, head of US rates strategy at BMO Capital Markets.

A vivid example of a messy auction was the $24 billion 30-year bond sale in November. Just before the 1 p.m. deadline on Nov. 9, the when-issued rate indicated a level of 4.716%, and then the new bond produced a rate more than 5 basis points higher at 4.769%. The poor demand left dealers holding nearly a quarter of the paper, double their usual allotment, and sparked hefty post-auction selling.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our YouTube channel.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

More Fixed Income Topics >