Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

When an income strategy is done right, it creates valuable and long-lasting peace of mind. After all, most investors start thinking about investment income for their retirement when they no longer have a steady paycheck.

That’s a huge transition for most people. As someone who has spent a good part of my career developing sound income strategies for investors, I’ve heard sighs of relief from recent retirees when they realize that their dividends and bond coupons can bridge their income gap and keep their lifestyle intact.

Investing for income is not foolproof. In fact, there’s a lot of ways to get it wrong! There are three pitfalls that I most commonly see income investors fall victim to. I hope illustrating them will help you avoid their damaging effects on your investment portfolio.

1. Limiting your investment choices

Most income investors fail to properly diversify. They think income investing consists of stodgy dividend-paying stocks and some bonds thrown in for stability. If that’s you, get familiar with the full menu of income investment options. They include real estate investment trusts (REITs), master limited partnerships (MLPs), preferred stocks, option strategies, closed-end funds, and merger arbitrage, to name a few. Opening yourself up to a wider range of income investment opportunities will present you with attractive options to diversify. If you stick to just one or two categories, you may be either taking on more risk than you want – or missing out on returns you could otherwise be achieving.

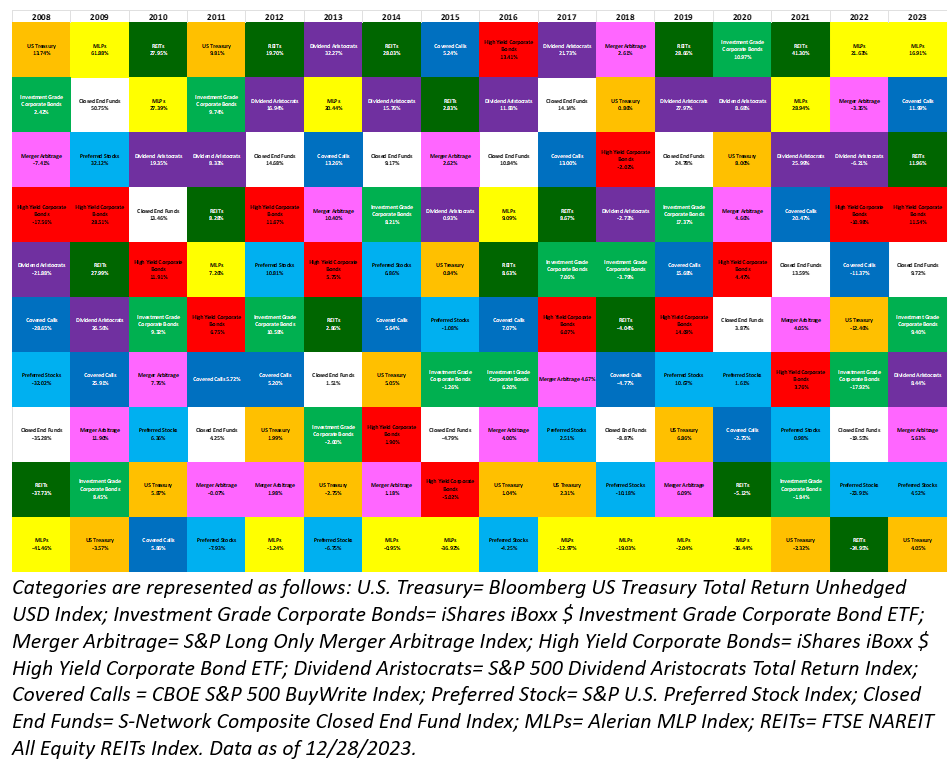

Look at the chart below. Zoom in to analyze the data, but to get the point, you need to pick a color. You see, each color represents a different type of income-generating asset class. Orange are U.S. Treasury bonds, yellow are MLPs, and so on. The color at the top performed the best in that year, the color at the bottom did the worst. Pick your color and see how it has done over time. My guess is that you’ll find times when it was towards the top, and other times it was among the worst performers.

Annual Performance of Select Income-Producing Investments

If you are an active investor, you may wish to navigate in and out of these categories in a more proactive way. Knowing what to avoid can make a tremendous difference in your results. Some advisory firms, Stansberry Asset Management included, thought it prudent to avoid bonds entirely in 2021 and most of 2022. If that’s not your style and you don’t have a competent advisor to do it for you, look to own the best investments you can across at least a handful of these categories. When your favorite category is in a slump, you’ll be glad you didn’t have all your eggs in that basket.

2. Sticking with what’s “safe”

There’s a feeling among many income investors that they must be conservative with their investments to achieve consistent results. After all, as most are in retirement; they’ve reached a point in life where it’s time to play it safe. That may be true to an extent, but many people underestimate just how long their retirement might last. If your portfolio is generating paltry returns because you selected the safest investments you could find, you risk having your wealth ravaged by inflation.

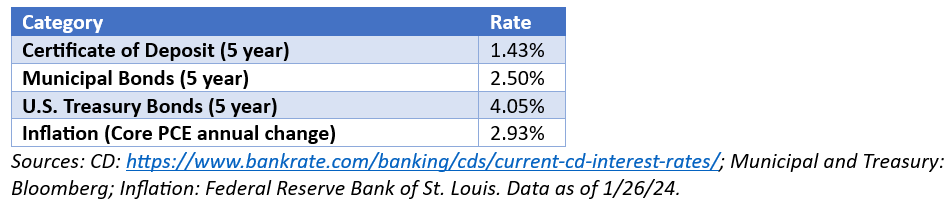

Some of the most conservative income investments include certificates of deposit (CDs), municipal bonds, and U.S. Treasury bonds. Look at their respective yields versus the rate of inflation.

It’s counterintuitive, but investing too conservatively can be quite risky! You risk losing your purchasing power over time to inflation – especially if inflation returns to levels we saw just a few months ago. There certainly may be a place for conservative investments in your portfolio – but in most cases, they should be a part of your plan, not the entirety of it.

3. Chasing yield

On the other side of the spectrum, there are investors who love buying the highest yielding investments they can find. All things being equal, who wouldn’t? Only, they aren’t equal. Yield is often a good proxy for risk. The higher the yield, the riskier the investment is likely to be. It’s okay to have some higher-yielding investments, but you should make sure you know what you own and understand why it yields what it does. In other words, understand the risk you are taking.

Investing in nothing but the highest yielding securities you find is a recipe for disaster. If you aren’t going to do the research, avoid this category completely and continue sleeping well at night. If you do want to perform the necessary diligence, check the dividend-payout ratio of any stock you are looking at as a first step. It’s simple: Check the financial statements to see: (1) How much income the company is earning; and, (2) How much it is paying in dividends. If 2 is greater than 1, you might have discovered a problem (and a dividend cut around the corner). Yes, there is a lot more to security analysis. But you might be surprised how many investors simply look at the dividend yield and never take this step, let alone a deeper dive.

A high yield can also signify that there’s little chance of a dividend increase. I have found that companies with a more modest yield but that have plenty of profits and a long history of raising dividends can be attractive investments. Their immediate yield may be lower, but these stocks can not only provide sturdy income but often a much higher total return over time.

Income investing doesn’t have to be boring. Or risky. By utilizing the entire income investment universe that’s available to you, generating a yield materially above inflation, and not getting too greedy, you will be well on your way to building a successful income-generating portfolio.

Michael Joseph, CFA is a portfolio manager and deputy chief investment officer at Stansberry Asset Management (SAM). He is a member of the CFA Institute’s Practice Analysis Working Body and sits on the board of Copper State Credit Union and the advisory board of the Arizona Council on Economic Education.

Stansberry Asset Management ("SAM") is a Registered Investment Advisor with the United States Securities and Exchange Commission. File number: 801-107061. Such registration does not imply any level of skill or training. This presentation has been prepared by SAM and is for informational purposes only. Under no circumstances should this report or any information herein be construed as investment advice, or as an offer to sell or the solicitation of an offer to buy any securities or other financial instruments.

For more information on SAM and Michael, please visit our homepage: www.stansberryam.com

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our videos.

Read more articles by Michael Joseph

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.