Bond traders are finally heeding one of the market’s oldest lessons: Don’t fight the Fed.

As the Federal Reserve pushed through its steepest interest-rate hikes in decades, investors consistently misjudged how far it would go, handing them steep losses in 2022 as Treasuries tumbled.

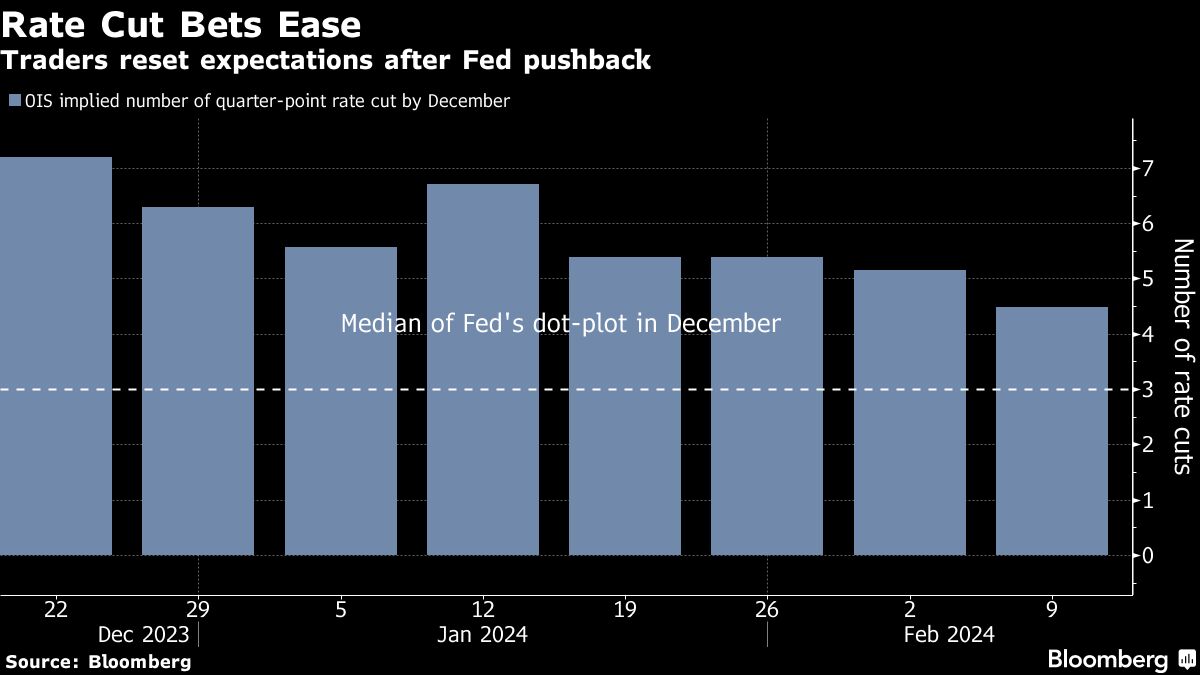

Then early last year, they wrongly wagered a banking panic would force the Fed to stop. And in December, after Chair Jerome Powell signaled he was done for good, they wagered he would pivot to easing policy aggressively, with the first rate cut coming as soon as March, even though the Fed’s forecasts showed otherwise.

But investors are now taking the central bank at its word.

In the derivatives markets, they’ve started pricing in that the Fed will carry out just four — or five at the most — quarter-point rate cuts in 2024, only slightly more than the three penciled in by policymakers. That’s a sharp shift from the end of last year, when futures traders were wagering on seven such moves, anticipating the Fed would cut rates by a full percentage point more than it was telegraphing at the time.

Of course, Fed officials could be wrong themselves on where rates are going — as happened back in 2021 — but by syncing up with them on the path of monetary policy, investors are now less likely to be caught off-guard by rate decisions. This promises to provide some stability to financial markets and potentially limit investors’ risk after three straight bruising years in the bond market.

“Clearly we got the message from the Fed that they want to do some insurance cuts because they see inflation falling,” said Ari Bergmann, founder of New York-based Penso Advisors, referring to the central bank’s interest in ensuring that policy doesn’t remain so tight that it stalls the economy. “I think the market is properly priced now.”

The Fed’s direction will hinge on whether inflation continues to recede, so the outlook could change.

But Powell has been clear that he welcomes solid economic growth as long as it doesn’t put upward pressure on consumer prices. There have been few signs of that: Economists are forecasting that on Tuesday the Labor Department will report that the consumer-price index rose 2.9% in January from a year earlier, the smallest increase since March 2021.

The steady retreat gives the Fed leeway to dial back interest rates simply to make policy less restrictive and prevent it from exerting too large a drag on the pace of the economy.

That expectation has helped to set a floor under the bond market, given the widespread consensus among investors that yields are at little risk of pushing back to last year’s peaks.

What Bloomberg Strategists Say:

Expectations of higher yields this year look rare, according to positioning and bank surveys. But the view of the minority could well be proven right due to a cyclical upswing in US and global growth that is gathering momentum, as well as favorable seasonals.

—Simon White, Bloomberg Macro Strategist

That sentiment was evident in the strong demand at the Treasury’s record $42 billion 10-year note auction last week. At the same time, options traders have been betting that the Treasury market will hold in a steady range as it waits for the Fed’s first move, which isn’t expected until May at the earliest.

“The Fed has three cuts for this year and the market has almost five, so directionally the market agrees with the Fed,” said Michael Cudzil, portfolio manager at Pacific Investment Management Co.

The discrepancy is not large enough to create the risk that Fed officials will try to reset expectations, especially given the uncertainty among themselves about where the policy rate will likely end the year. While most Fed officials have projected between two and four cuts, with the median at three, they ranged from as many as six cuts to none at all.

Benson Durham of Piper Sandler & Co., a former economist at the central bank, says his model shows that the pricing in the options market is pretty well aligned with the Fed’s projections.

A separate one tracked by the Atlanta Fed showed last week that options tied to the Secured Overnight Financing Rate indicated traders were putting roughly even odds on policymakers enacting no more than four quarter-point cuts in 2024. At the start of the year, the probability of that was just one-third, with the market counting on a faster pace of easing.

What to Watch

- Economic data:

- Feb. 12: New York Fed 1-year inflation expectations; monthly budget statement

- Feb. 13: Consumer price index; real average earnings

- Feb. 14: MBA mortgage applications

- Feb. 15: Initial jobless claims; retail sales; Philadelphia Fed survey; import and export price index; industrial production; capacity utilization; business inventories; TIC flows; NAHB housing market index

- Feb. 16: Housing starts; building permits; Producer price index; New York Fed services business activity; U. of Mich sentiment and inflation expectations

- Fed calendar:

- Feb. 12: Richmond Fed President Tom Barkin; Minneapolis Fed President Neel Kashkari; Fed Governor Michelle Bowman

- Feb. 14: Chicago Fed President Austan Goolsbee; Federal Reserve Vice Chair for Supervision Michael Barr

- Feb. 15: Atlanta Fed President Raphael Bostic; Governor Christopher Waller

- Feb. 16: San Francisco Fed President Mary Daly

- Auction calendar:

- Feb. 12: 13-, 26-week bills

- Feb. 14: 17-week bills

- Feb. 15: 4-, 8-week bills

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our YouTube channel.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

More Fixed Income Topics >