Beginning this year, the SECURE Act 2.0 allows owners of 529 plans to convert unused 529 funds to the beneficiary’s Roth IRA. But there are some stringent conditions, major ambiguities in the law, and potential income taxes and even penalties. I’ll cover the law and tax implications, my experience converting some of my son’s 529 money to his Roth, and some strategies this new law offers for college and beyond.

Beginning this year, the SECURE Act 2.0 allows owners of 529 plans to convert unused 529 funds to the beneficiary’s Roth IRA. But there are some stringent conditions, major ambiguities in the law, and potential income taxes and even penalties. I’ll cover the law and tax implications, my experience converting some of my son’s 529 money to his Roth, and some strategies this new law offers for college and beyond.

The law

This new law has huge benefits for those with large 529 account balances whose children have completed college and have unused funds. Before this year, the owner would have to pay taxes and a penalty to get money out of the account. Now, under certain conditions, the beneficiary can receive this money in a Roth tax-wrapper that, under current law, can grow for decades income tax-free.

Here are the details:

- The lifetime distribution limit is $35,000 per beneficiary.

- The maximum annual conversion amount is the IRS maximum for IRAs, currently $7,000 for those under age 50, less any other IRA contributions made that year by the beneficiary.

- The 529 plan must be open for at least 15 years.

- The Roth IRA must be in the name of the beneficiary of the 529. That beneficiary must have earned income at least as much as the rollover amount. Unlike a direct Roth contribution, the income limit does not apply to these Roth conversions.

- The rollover must be a direct rollover from the 529 plan to the Roth IRA custodian (trustee to trustee). The owner or beneficiary cannot take a check – no 60-day rule.

- Contributions and earnings on those contributions made in the last five years cannot be converted to a Roth.

While somewhat stringent, at first the law seems clear, yet this is far from reality. I spoke to Richard Ellis, executive director of the Morningstar gold rated My529 plan (Utah) where I have an account. He pointed out some of the ambiguities that need to be clarified by the IRS.

- Does the 15-year rule mean it has to be the same beneficiary?

- Does the 15-year rule include the time an account was open at another plan if it is rolled over from another state?

- How can one track the income by contributions for the past five years if the plan does not calculate it?

- Can one change the beneficiary after the $35,000 has been distributed to someone else (or even themselves) and start another $35,000 distribution to a Roth?

- Can a beneficiary over age 50 make a catch-up contribution of $1,000 in addition to the $7,000?

When will the IRS clarify these issues? Ann Garcia, a principal at Independent Progressive Advisors and author of How To Pay For College, told me she thinks the IRS will be in no hurry since the 529s were designed to help people pay for college and this new conversion law mostly benefits the wealthy. For this reason, she is recommending waiting at least a couple of months before initiating a conversion. Paul Curley, director of 529 & ABLE Solutions at ISS Market Intelligence, also recommended waiting. He said that publication 970 (Tax Benefits for Education) may soon be issued and that industry letters to the IRS seeking clarification may soon be answered. (Subsequently, publication 970 was issued but provided no clarification.)

Another complication is that federal law may not comply with state law. While the federal government considers these Roth rollovers a qualified distribution, the state may not. They could recapture any state income tax deduction or credit received when the 529 contribution was made, levy income tax on the gain and, in at least one case, even charge a penalty.

Curley developed the following listing of where states stand on these Roth rollovers.

More detail can be found here. Curley noted that California will be subject to state income tax and the additional 2.5% California tax on the gains. California has no deduction for the 529 contribution so there is no recapture.

But even if a state levies taxes on a conversion, the federal tax savings of moving funds into a Roth are huge.

The conversion process – A tale of two state 529 plans

Before recommending this to clients, I decided to first try a conversion with my 529 funds. As background, I have one child (Kevin) who finished college nearly four years ago with no plans for graduate school. I over-funded the 529 plans thinking he would go to private college but, instead, he stayed in state with a partial scholarship. My home state’s 529 (Colorado) was too expensive when he was young, so I gave up the state tax deduction and chose Utah (now My529). Later, the Colorado plan became less expensive, and I made some contributions to that direct plan as well.

I now have more than $35,000 of unused 529 money and don’t have any ambiguities previously mentioned at the federal level as both plans are over 20 years old and my son has been the beneficiary since opening the account.

I called the Colorado plan’s 800 number and the representative explained to me that this hadn’t yet been approved by the IRS. I escalated to a supervisor who had a different response; I’d have to initiate the conversation with the Roth custodian. That made no sense to me since the Roth and 529 accounts have different owners. Having a beneficiary convert and transfer assets from a different owner has obvious internal control issues. Later, in an email, Jon Pagnozzi, the sales director of the plan, confirmed the process, stating, “Start the rollover out by having the institution that holds your Roth account submit one of their transfer forms to Vanguard.”

A few minutes after the Colorado failure, I called the Utah My529 plan. The experience couldn’t be any more different than with Colorado. The representative showed me how to get to their online form “Roth IRA Rollover Request.” It was quick and easy to complete and execute via email. The next day, I received an email stating my request had been processed and a paper check would be mailed to Vanguard FBO Kevin’s Roth IRA.

Afterwords, I interviewed the heads of each plan. I spoke to Colorado’s CollegeInvest CEO, Angela Baier, and Pagnozzi. I asked them to confirm the process of initiating with the beneficiary’s Roth IRA custodian and Baier stated “that’s what Vanguard told us.” A Vanguard spokesperson confirmed that this was not initiated with Vanguard.

After I mentioned other states have Roth IRA Rollover request forms, Baier responded that it didn’t have one on the direct portfolio because of tax ambiguities. She later noted the Colorado advisor-sold platform did have such a form. “This is an easy fix,” she said, as they can get the form up in a few days and stated the law was only 18 days old and noted “we’re ahead of the game.” Later she wrote me it was delayed for consumers as they have “varied financial literacy.” They apparently quickly became comfortable with consumers’ financial literacy, as a few days later, the transfer form appeared on their website.

The Utah plan is a better example of being “ahead of the game.” Ellis told me the My529 plan had been preparing for this for some time and had the form ready by early December 2023. His staff had gone through training preparing for this new law. He credits the College Savings Foundation and College Savings Plan Network for holding virtual meetings with the 529 plans to help all participating states be ready before the new law took effect.

Ellis said he had expected about 10 conversions for the month of January but had about 100 during the first two weeks of the year. He stated the average conversion amount requested was close to the $7,000 annual maximum. He also expected most of the conversions would be in accounts linked to an advisor but none of the 100 was.

Conclusions and strategies

With clients who have any of the IRS ambiguities noted earlier, hold off a few months in hopes of receiving additional clarity from the IRS. Most state 529 plans are ahead of the game; a random internet search I did of 10 plans all came up with forms to initiate a Roth IRA rollover request. I suspect Colorado is in the small minority of those lagging behind.

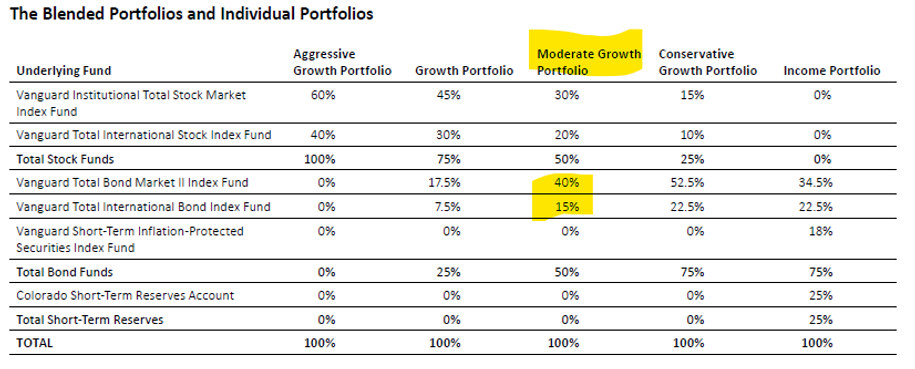

This wasn’t the first error I’ve noted from the Colorado 529 Plan. As an example, I pointed out another glaring error on its January 2023 disclosure statement that indicated its moderate growth portfolio asset allocation totaled 105%.

When I first pointed it out, Pagnozzi stated he would launch an investigation on how Vanguard let this happen. More than three months later, it remained on their web site. He told me, “We do all the fiduciary stuff.” Later, Baier stated, “The error is Vanguard’s.” A Vanguard spokesperson said, “When Vanguard became aware of the discrepancy in the plan disclosure document, we took steps to publish updates in coordination with other pending changes to the plan disclosure document in a timely manner.” I calculated the actual return was 0.28% lower than what was on their disclosure, or $280 on a $100,000 account. That’s material and likely millions of dollars across all investors.

It’s critical to pick the right plan and Morningstar’s 529 Ratings are a good place to start, though I wouldn’t even give CollegeInvest a bronze. Of course, one should consider any state deduction or credit along with fees.

The SECURE Act 2.0 opens new 529 strategies. The fear of over-funding is far less. I argued it was never such a problem because the worst-case scenario was a 10% penalty is only on the gain and that may even be worth the decades of tax-deferral. Now, this strategy makes sense to intentionally over-fund.

One could employ what I call an “off label” use. Similar to using an HSA like a Roth (keeping receipts and reimbursing decades later tax-free), someone could open the 529 with themselves as beneficiaries to begin converting to a Roth 15 years later. Doing so may provide a state tax deduction now and, unlike an HSA, not require one to keep receipts for future reimbursement on the tax-free growth. Other strategies may be attractive such as setting up 529s and naming adult children who have completed college as beneficiaries since the funds could later be converted to a Roth. For these more advanced strategies, I would recommend waiting a few months in hopes of some clarity from the IRS.

While I’ve always said investing is simple; I’ve never said taxes were. While very complex, the SECURE act 2.0 opens significant tax advantages in the 529 space, both for funding college and for retirement planning.

Allan Roth is the founder of Wealth Logic, LLC, a Colorado-based fee-only registered investment advisory firm. He has been working in the investment world of corporate finance for over 25 years. Allan has served as corporate finance officer of two multi-billion-dollar companies and has consulted with many others while at McKinsey & Company.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

More Small Cap Topics >

Beginning this year, the SECURE Act 2.0 allows owners of 529 plans to convert unused 529 funds to the beneficiary’s Roth IRA. But there are some stringent conditions, major ambiguities in the law, and potential income taxes and even penalties. I’ll cover the law and tax implications, my experience converting some of my son’s 529 money to his Roth, and some strategies this new law offers for college and beyond.

Beginning this year, the SECURE Act 2.0 allows owners of 529 plans to convert unused 529 funds to the beneficiary’s Roth IRA. But there are some stringent conditions, major ambiguities in the law, and potential income taxes and even penalties. I’ll cover the law and tax implications, my experience converting some of my son’s 529 money to his Roth, and some strategies this new law offers for college and beyond.