Investors are beginning to war-game how the Federal Reserve can manage a US economy that just won’t land, with some even debating whether interest-rate hikes will be needed only weeks after a steady run of reductions appeared all but certain.

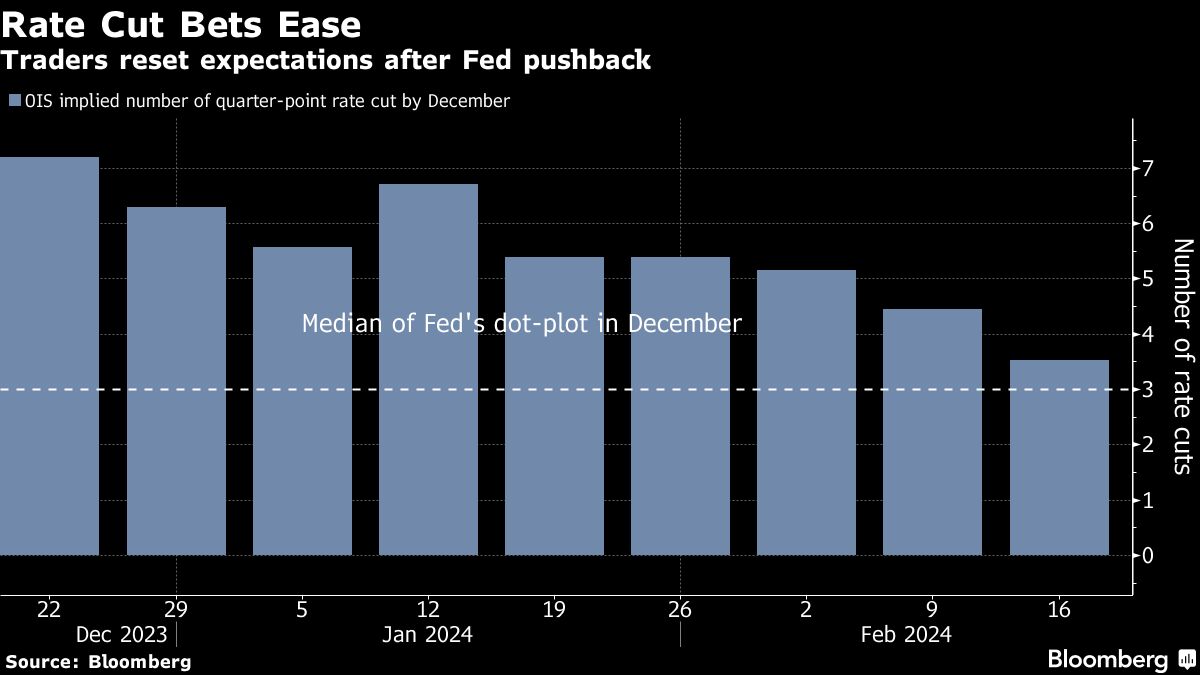

Bets on lower rates coming soon were so prevalent a few weeks ago that Fed Chair Jerome Powell publicly cautioned that policymakers were unlikely to be in position to cut as of March. Less than three weeks later, traders have not only removed March as a possibility but May also looks improbable, and even conviction about the June Fed meeting is wavering, swaps trading shows.

The latest hot debate: perhaps the next shift isn’t a cut at all. Former US Treasury Secretary Lawrence Summers on Friday voiced what a number of market participants had already been thinking: “there’s a meaningful chance” the next move is up.

Even if another hike is too hard to countenance, some Fed watchers are floating a repeat of the late-1990s: only a brief course of rate reductions that sets the stage for increases later.

“There are so many possible, plausible outcomes,” said Earl Davis, head of fixed income and money markets at BMO Global Asset Management. While he’s sticking with 75 basis points of cuts for 2024, he said “It’s very hard for me to say that with a high degree of confidence.”

For their part, no Fed policymaker in recent weeks has publicly suggested that further rate increases are on the table. Powell on Jan. 31 said, “We believe that our policy rate is likely at its peak for this tightening cycle.” On Friday, San Francisco Fed President Mary Daly, viewed as a centrist, said 75 basis points of cuts in 2024 was a “reasonable baseline expectation.”

At the same time, the central bank hasn’t offered the kind of “forward guidance” with regard to a medium-term policy framework that it’s sometimes presented in the past — leaving investors with less of steer. Volatile economic data this month has driven swings in Treasuries, futures and swaps contracts.

Yields jumped last week after hotter-than-expected consumer and producer price index data. A key subset of CPI services prices advanced by the most in nearly two years. Job gains for January also exceeded forecasts, though a slump in retail sales for the month offered a counterpoint to evidence that the economy continues to expand faster than its longer-term potential.

Two-, three- and five-year yields all reached their highest levels since early December last week.

“The last yards of this inflation fight is going to be bumpy,” said Lindsay Rosner, head of multi-sector fixed income investing at Goldman Sachs Asset Management. “It does feel a little bit like a ping-pong match with every single data point.”

Rosner said she agreed with Summers’s assessment of some risk of a rate hike, though concluded “it would make more sense to hold at these levels of interest rates for longer” for the Fed to be assured of quelling inflation.

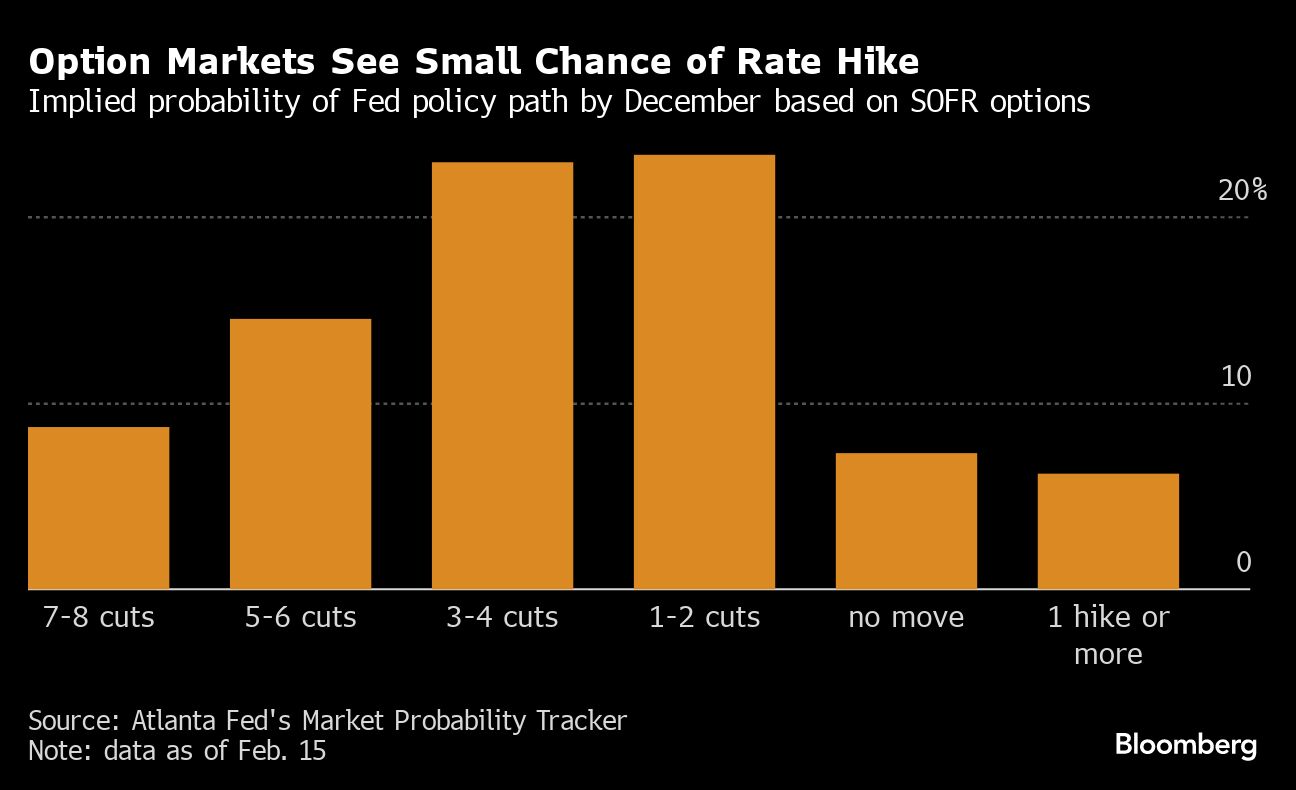

Summers, a Harvard University professor and paid contributor to Bloomberg Television, suggested a perhaps 15% chance that the next Fed move is an increase. Mark Nash, who manages absolute return macro funds at Jupiter Asset Management, puts the odds at 20%.

Even some who do expect rate cuts have advocated taking out insurance on that bet. BMO’s Davis has been shorting two-year Treasuries since December, though covered half of that position amid the climb in rates since the start of the year.

At Societe Generale SA, Chief FX Strategist Kit Juckes told clients in a report last week that if “the US economy re-accelerates, the Fed will eventually have to tighten again and the dollar will rally,” possibly back to 2022’s all-time high.

Analysis of short-term interest rate options by Bloomberg Intelligence showed that traders began to price in some chance of a Fed hike over the next year in the wake of the CPI release last Tuesday.

The outlier-options demand is also driven by the fact that it’s a cheap way to bullet-proof portfolios built around the base case, said David Robin, a strategist at TJM Institutional who’s been working in debt derivatives markets for decades.

“People are trying to figure out where their portfolios will implode, and hedge for that,” said Robin, who expects the Fed to cut two or three times this year.

Strategists at Citigroup Inc. say there should be even more hedging for the risk of the Fed engaging in only a very brief easing cycle, followed by rate increases shortly thereafter. The bank, whose economists expect the Fed’s first rate cut in June, sees some potential for the next few years to mirror what happened in the late 1990s.

What Bloomberg Intelligence Says...

“It was just a month ago when there was no hedging at all for the possibility of higher rates, and now you have at least some investors who seem to be doing so.”

“There’s less of a one-way distribution now of possible Fed outcomes that are being priced into the market. The long tail toward lower rates remains, but this shift is important.”

-Ira Jersey, chief US interest-rate strategist

In 1998, officials cut rates three times in rapid-fire succession to short-circuit a financial crisis brought on by the Russian debt default and the near-collapse of hedge fund Long Term Capital Management. The Fed then began a cycle of rate increases in June 1999 to contain inflationary pressures.

Besides volatile domestic economic data, there are international considerations, Pacific Investment Management Co. economist Tiffany Wilding said. Among them: the conflict in the Red Sea and drought-driven slowdowns in the Panama Canal, with disruptions to shipping sending freight costs higher.

It all could contribute to a “stop-start easing policy,” Wilding said. “There is a risk and it’s very difficult to forecast.”

The bottom line for the rates market in 2024, BMO’s Davis says: “There’s going to be extreme volatility both ways.”

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our YouTube channel.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

More Volatility/Downside Protection Topics >